The Conversation (0)

Many Peaks Minerals Limited (ASX:MPK) (Many Peaks or the Company) is pleased to announce entering a binding Share Sale Agreement (Agreement) with Turaco Gold Limited (Turaco) to acquire its 89% interest in CDI Holdings (Guernsey) Ltd (CDI Holdings). CDI Holdings is an 89% subsidiary of Turaco, held with Predictive Discovery Limited (Predictive), holding an 11% free carry ownership in a joint venture with Turaco. The Agreement will trigger Turaco’s drag-along right in its joint venture with Predictive, whereby Many Peaks will also acquire Predictive’s remaining 11% interest and consolidate 100% ownership of the joint venture entity CDI Holdings.

HIGHLIGHTS

Ferke Gold Project, 300km2

Odienne Project, 758km2

The consideration for the purchase of 100% of CDI Holdings will be an aggregate 5,617,978 fully paid ordinary shares in Many Peaks subject to a 12 month escrow, to be issued under the Company’s capacity under ASX listing rule 7.1. Upon completion, Many Peaks will also assume a royalty deed for a 1% net smelter return royalty payable to Resolute (Treasury) Pty Ltd (Resolute)—further information on terms and conditions precedent outlined below.

Many Peaks’ Executive Chairman, Travis Schwertfeger, commented: “The Ferke and Odienne Projects in Cote d’Ivoire deliver Many Peaks a strong foundation of exploration success in Cote d’Ivoire with the potential to build significant high- grade ounces in the near term. Both projects are already covered with systematic geochemical coverage and high-resolution geophysics, which have led to demonstrated gold mineralisation confirmed in drilling. Leveraging over US$4m of previous expenditure in recent years has generated multiple targets ready for follow-up, including extension targets, providing Many Peaks with a transformational acquisition with near-term resource potential viable.

Our team has a depth of West African operating experience tied to multiple discovery and development projects over the past 15 years, and our technical team looks forward to operating in Cote d'Ivoire again. Over recent years, it has emerged as a premier jurisdiction within West Africa to operate in, with several recent exploration and development successes.

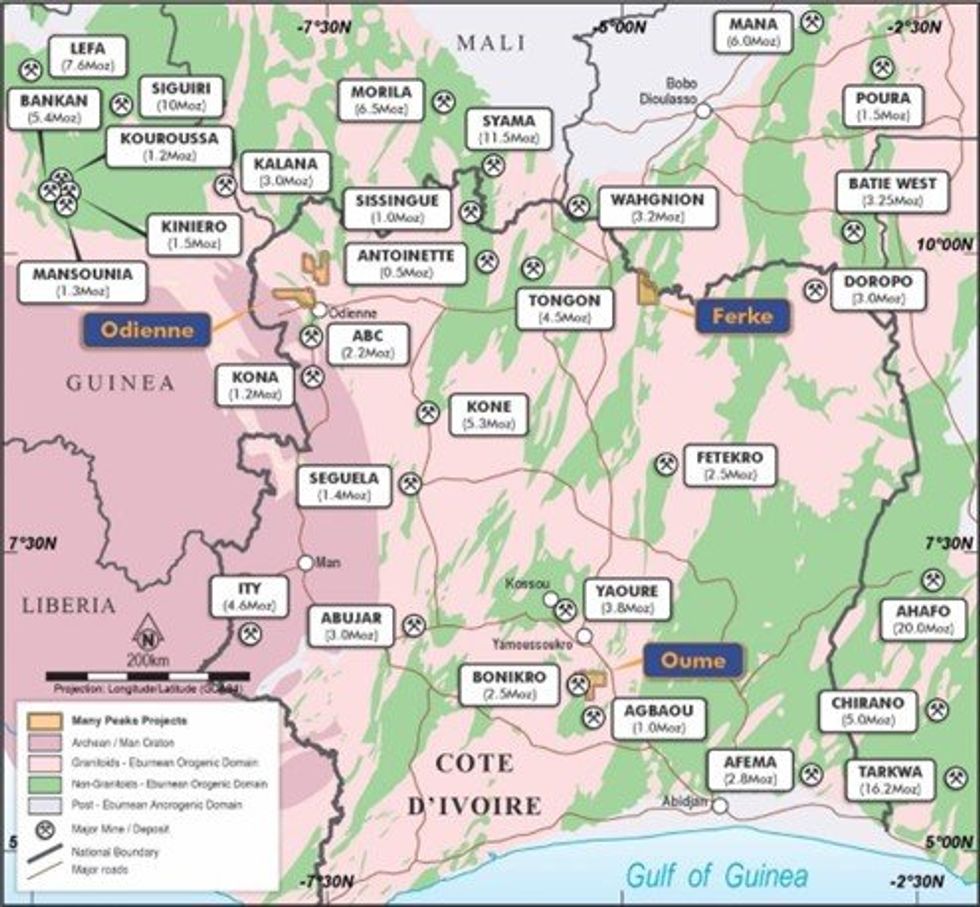

Figure 1: Project Locations

Figure 1: Project Locations

Ferke Gold Project

The Ferké Gold Project (Ferke) is located in northern Cote d’Ivoire, covering 300km2 in a granted exploration permit licence. Ferke is situated on the eastern margin of the Daloa greenstone belt at the intersection of major regional scale shear zones (refer to Figure 1). Initial exploration undertaken at the Ferke Gold Project by Predictive Discovery Ltd in 2016 and 2017 (previously referred to as Ferkessedougou North) comprised several phases of geochemical stream and soil sampling across the permit area, which has defined a more than 16km long gold-in-soils anomaly on the ‘Leraba Gold Trend’ (refer to Figure 2 and Predictive’s ASX announcement dated 2 February 2017).

Click here for the full ASX Release

This article includes content from Many Peaks Minerals, licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.