The Conversation (0)

On 30 January 2024, Jindalee Lithium Limited (Jindalee, the Company) lodged its December 2023 Quarterly Activities Report, which summarised activities undertaken at the Company’s 100% owned McDermitt Lithium Project located in Oregon, USA (Project)1. McDermitt is currently the largest lithium deposit in the USA by contained lithium in Mineral Resource and is a globally significant resource with the potential to supply lithium carbonate equivalent (LCE) to US supply chains for decades2 (Table 1).

Jindalee is pleased to provide an update on US government funding opportunities for McDermitt.

Grant applications lodged with two US Government agencies (Defense and Energy)

Jindalee advises that the Company has lodged applications for non-dilutive grant funding with both the Department of Defense (DoD) and the Department of Energy (DoE) (Battery Manufacturing and Recycling Grant).

If successful, the DoD grant application is expected to co-fund an accelerated Feasibility Study and associated drilling and testwork, whilst the DoE grant application is designed to potentially co-fund the engineering, procurement, construction and development of a lithium processing facility at McDermitt.

Both grant applications have passed initial reviews by the agencies. The DoE grant application was accompanied by letters of support from Oregon and Nevada politicians and agencies, as well as potential Project partners.

The Company expects to provide updates regarding the status of applications and any potential award decision in the second half of 2024.

Substantial Government funding for US critical mineral projects continues

The US Government is committed to securing a domestic supply for critical minerals to reduce reliance on foreign sourced materials, including lithium, and is providing significant support and funding via the Inflation Reduction Act, the Defense Production Act and other initiatives as recent developments indicate.

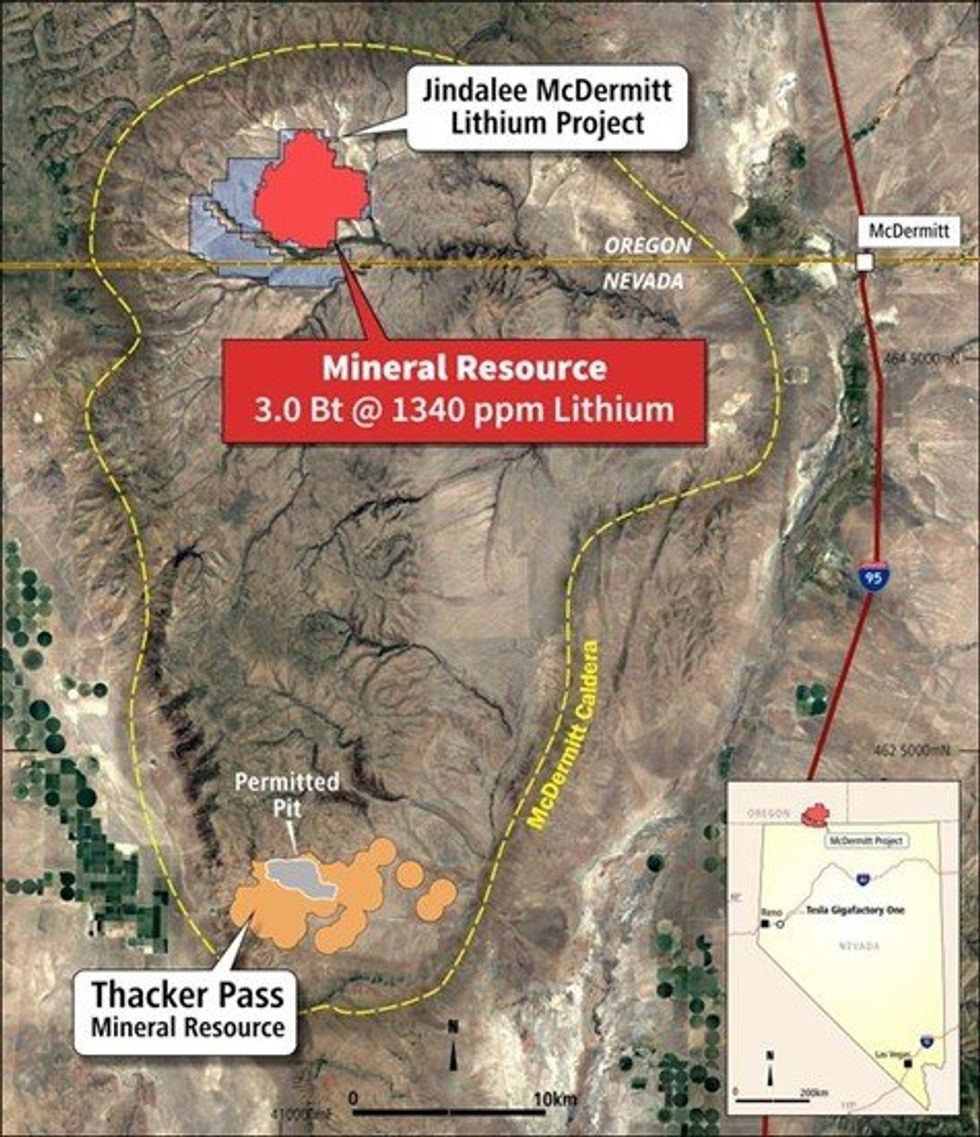

On 14 March 2024 Lithium Americas Corp (TSX: LAC, Market Cap: C$1.5bn6) announced that it had received a conditional commitment from the DoE for a US$2.26 billion loan for financing the Phase 1 construction of processing facilities at the Thacker Pass Lithium Project3, located approximately 30km south of McDermitt (Figure 1). The loan, anticipated to cover approximately 75% of Thacker Pass’s initial capital cost, offers favourable terms with an interest rate equivalent to the US Treasury rates (0% spread) and a tenor of 24 years.

On 8 April 2024 Perpetua Resources Corp (TSX: PPTA, Market Cap: C$538m6) announced that it had received a Letter of Interest from the US Export-Import Bank for potential debt of up to US$1.8 billion for capital funding of the Stibnite Gold and Antimony Project in Idaho, USA4. This follows earlier grants of up to US$59.4 million received by Perpetua Resources from the DoD to assist with construction readiness and permitting of the Stibnite Project5.

Jindalee’s CEO Ian Rodger commented “We are very pleased with the progress of our grant applications for the McDermitt Lithium Project, particularly with the strong backing we’ve received from key stakeholders, including US politicians and potential Project Partners. The support for our applications highlights the strategic importance of our Project and its alignment with US national interests. These non-dilutive grants, if successful, promise to significantly enhance equity returns, reinforcing our strategy and amplifying the value we deliver to our shareholders.

Table 1 – Summary of 2023 McDermitt Mineral Resource Estimate at the reporting cut-off of 1,000ppmNote: totals may vary due to rounding. (Lithium carbonate equivalent (LCE) is calculated by taking the lithium value and multiplying by 5.323 to determine the molar equivalent in standard industry fashion).

Table 1 – Summary of 2023 McDermitt Mineral Resource Estimate at the reporting cut-off of 1,000ppmNote: totals may vary due to rounding. (Lithium carbonate equivalent (LCE) is calculated by taking the lithium value and multiplying by 5.323 to determine the molar equivalent in standard industry fashion).

Figure 1 – McDermitt Caldera: Location of McDermitt and Thacker Pass projects

Figure 1 – McDermitt Caldera: Location of McDermitt and Thacker Pass projects

Click here for the full ASX Release

This article includes content from Jindalee Lithium Limited, licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.