The Conversation (0)

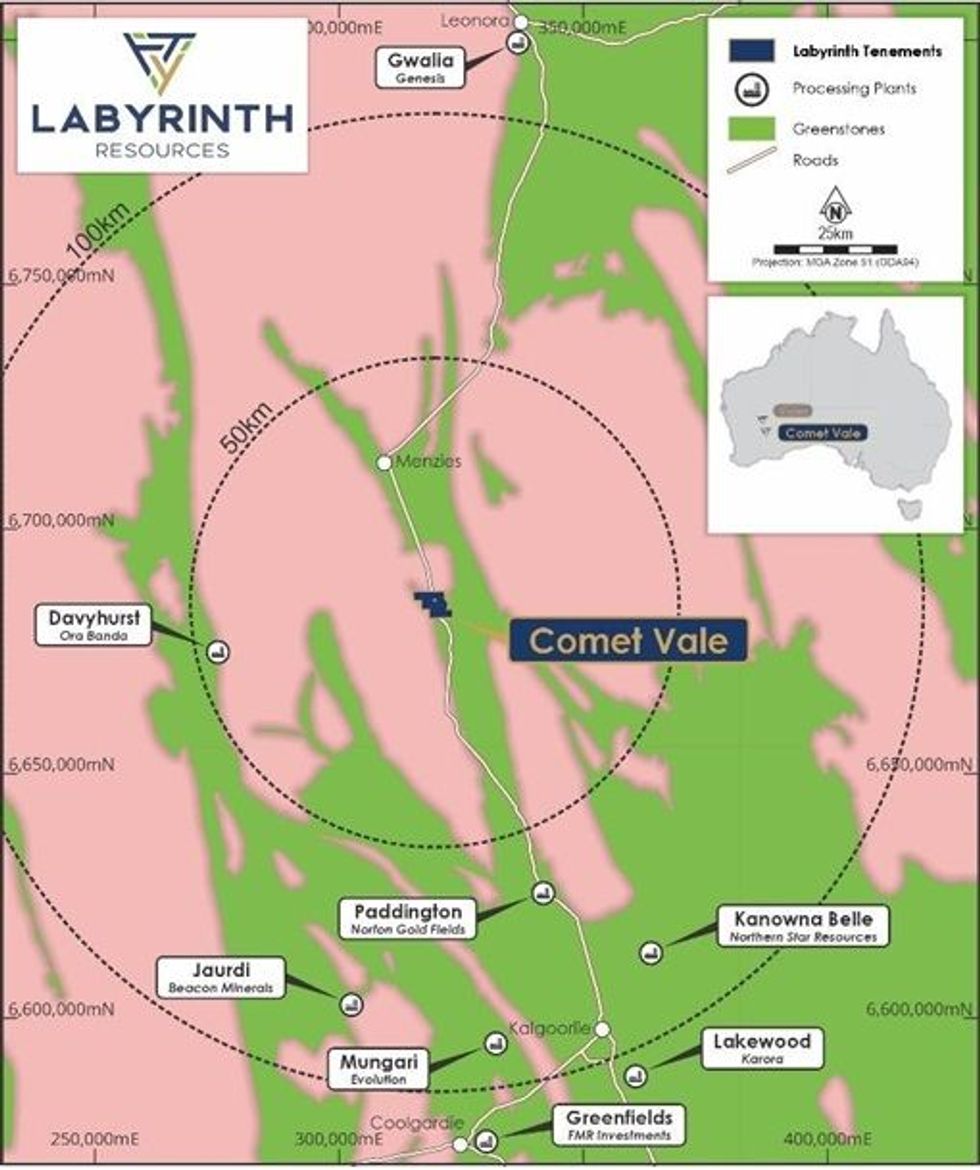

Labyrinth Resources Limited (ASX: LRL) (‘Labyrinth’ or ‘the Company’) is pleased to report highly promising gold and copper assays from soil sampling and rock chips at its Comet Vale Project in WA (see Figure 1).

More than 500 soil samples and 11 rock chip samples were collected. These results, combined with historic data, have defined several compelling drilling targets outside the mine area at Comet Vale.

In July 2024, Labyrinth entered into an option to acquire 100% of the property from Sand Queen Gold Mines Pty Ltd (‘SQGM’). The additional 49% interest has been the key to commencing dedicated exploration activity. Labyrinth intends to use some of the proceeds of its recent successful capital raising to undertake further exploration work with the aim of refining the targets ahead of a drilling campaign.

Figure 1. Regional location of Comet Vale Project.

Figure 1. Regional location of Comet Vale Project.

Labyrinth Chief Executive Jennifer Neild said: “We have strategically positioned ourselves in the prolific Goldfields region of Western Australia, with proven gold assets that have the potential for further high-grade mineralisation.”

“These assays are indicative of this potential. We are seeing cohesive trends in both primary and associated indicator elements. The overlap of these anomalies have added weight to positions of interpreted faults and have established several high priority target areas.”

“We now have extensive data that Comet Vale may host a large mineralised system with areas of high-grade gold and potentially copper.”

Details of sampling results:

The two campaigns of soil sampling were the first full geochemical analysis completed at Comet Vale. On the eastern side of the highway, a small number of rock chips were taken to support mapping observations. Many of the higher grades exist around Long Tunnel Prospect, where shallow tungsten and gold workings exist. It is unknown the extent of activites, refer to Table 2 for a summary.

Click here for the full ASX Release

This article includes content from Labyrinth Resources, licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.