The Conversation (1)

Thomas Kohi12 Dec, 2017

The copper market has been on a wild ride for much of the past year.

2025 was punctuated by tariff threats, supply-side disruptions and increasing demand, events that bled into 2026 and helped push copper prices to record highs at the beginning of the year.

A US Supreme Court decision that overturned 2025’s “Liberation Day” tariffs added further uncertainty to the market, with prices moderating in February and March as Middle East tensions broke into all-out war between the US and Iran.

The war caused a spike in oil prices, unsettling investors and heightening volatility in equity and bond markets.

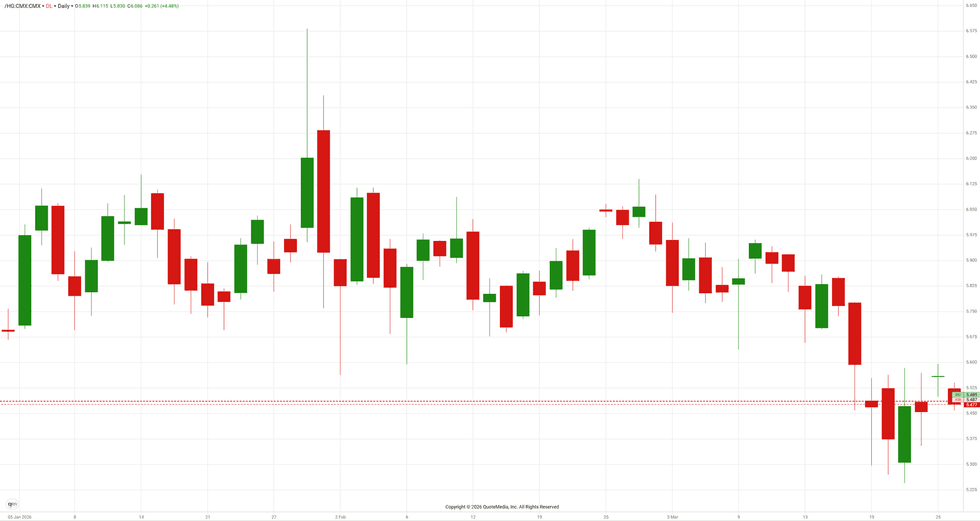

The standard three month copper contract on the London Metal Exchange (LME) opened the year at US$12,469.50 per metric ton (MT); meanwhile, continuous contracts on the Comex started at $5.69 per pound.

While prices on both exchanges were volatile, they remained above those levels for the rest of the month and on January 29 reached new record highs of US$13,952 on the LME and US$6.20 on the Comex.

Copper price, January 1 to March 26, 2026.

Chart via the Investing News Network.

Through February and much of March, LME copper prices traded between US$12,674 and US$13,500, while Comex prices moved within a range of US$5.64 to US$6.09. During the last half of March, prices saw downward pressure, falling to quarterly lows. LME prices sank to US$11,925 per MT, and Comex prices fell to US$5.38 on March 20.

As mentioned, the copper market began 2026 riding a wave of momentum that started in 2025.

The red metal has been widely expected to move into deficit for a number of years due to a lack of new mines coming online, as well as significant increases in demand as a result of urbanization in the Global South, the acceleration of the energy transition and the emergence of artificial intelligence.

Against that backdrop, copper supply experienced significant disruptions in 2025, as incidents at Ivanhoe Mines' (TSX:IVN,OTCQX:IVPAF) Kamoa-Kakula mine and Freeport-McMoRan's (NYSE:FCX) Grasberg mine forced temporary closures. While operations have resumed, both operations will take some time to fully recover.

Supply shocks helped drive copper to record highs in January, marking the peak of a price surge of more than 40 percent since the start of 2025. Downstream, this lack of supply has kept treatment and refining charges at smelting operations in negative territory as they compete for a limited amount of concentrate.

Some operations have turned to processing scrap or other metals to keep their smelters active.

According to a report from Goldman Sachs (NYSE:GS), tightness will ease to an extent later in the year as stockpiled inventories in the US begin to make their way back into the market.

Metal traders in the country have been buying metal in anticipation of incoming tariffs.

While a 50 percent tariff was applied to raw materials in August of last year, refined products were largely spared for the time being, with levies gradually being applied in 2027 and 2028.

However, a February 20 US Supreme Court ruling that overturned last year's “Liberation Day” tariffs from the Trump administration has created concerns that the timeline for copper tariffs could be accelerated. Goldman Sachs’ report suggests some analysts even believe the tariffs could begin rolling out later this year.

Market watchers are split over the supply situation for 2026, with Goldman Sachs predicting a surplus of 160,000 MT, while the International Copper Study Group is eyeing a deficit of 150,000 MT.

Overall, a supply gap is expected to widen in the coming years, with S&P Global predicting that mine output will peak in 2030 at 27 million MT per year, before falling to 22 million MT by 2040. These declines are attributed to a combination of lower grades at existing mines and a dearth of new projects set to come online.

What new projects there are will take years to fully realize, with the average time for a copper mine to go from the exploration stage to production taking around 15 years. Even new development projects and expansions that start this year will take years to have any material effect on the market.

In mid-March, Freeport announced it is planning a US$7.5 billion expansion of its El Abra mine in Chile, which, when completed, will increase output there to around 300,000 MT per year. KoBold Metals' Mingomba project, which started development in March, will also add 300,000 MT of copper supply, but won’t be completed until the early 2030s.

While copper supply issues have largely carried over from 2025, the demand side has been a little more eventful, particularly since the start of March and the beginning of hostilities between the US and Iran.

The situation has sent oil prices surging, with Brent climbing as high as US$120 per barrel and West Texas Intermediate crossing above US$100. As a result, metals prices saw significant declines toward the end of the quarter.

In an email to the Investing News Network, IndependentSpeculator.com CEO Lobo Tiggre explained that the war could potentially put downward pressure on demand for copper.

“Oil spikes like we’re seeing now are highly correlated with recession — and that’s bad for Dr. Copper,” he said.

Chinese demand is also still weak as the country continues to feel the effects of a real estate downturn that began in 2020. It has made several attempts to inject stimulus into the sector over the past few years, with little impact.

China’s new five year plan, which is set to run from 2026 to 2031, may cause the real estate market to rebound, but its focus has largely been shifted to social outcomes rather than material effects.

“China is still growing, so I don’t see things changing too much," said Tiggre.

"But it did impress me that they talked about 'investing in people,' which suggests more social spending than building stuff. That might be slightly near-term bearish for commodities."

China is still dedicated to the green transition, which could provide tailwinds for copper in the mid to longer term.

Looking long term, the case for copper remains strong. The market is still expected to start seeing significant shortfalls over the coming years, with the amount increasing significantly after 2030.

Base-level demand is set to outgrow supply on its own, but additional factors like the energy transition, artificial intelligence data centers and electric vehicles are seen pushing the gap wider.

In the short term, the markets are closer to being balanced, but a protracted war with Iran, or a long-term closure of the Strait of Hormuz, could cause an oil price shock and a global recession.

Such an event would have a significant impact on demand and could provide opportunities for investors.

“There is potential for near-term oversupply, especially if the war puts a damper on demand. This would actually be ideal for anyone who missed the chance to load up cheaper a year ago,” Tiggre said.

While Tiggre didn’t offer an exact price forecast, he expects some declines in the copper prices over the next few weeks before a strong surge toward the end of the year.

Don’t forget to follow us @INN_Resource for real-time news updates!

Securities Disclosure: I, Dean Belder, hold no direct investment interest in any company mentioned in this article.

Editorial Disclosure: The Investing News Network does not guarantee the accuracy or thoroughness of the information reported in the interviews it conducts. The opinions expressed in these interviews do not reflect the opinions of the Investing News Network and do not constitute investment advice. All readers are encouraged to perform their own due diligence.

Affiliate Disclosure: The Investing News Network may earn commission from qualifying purchases or actions made through the links or advertisements on this page.

Learn about our editorial policies.