The Conversation (0)

Jun. 18, 2026 06:18AM PST

Johan Swanepoel / Shutterstock

A widening two-dollar spread between the world’s cheapest and most expensive copper producers is exposing a growing vulnerability in the global supply chain.

According to data by Mining Visuals, mining companies are failing to contain their core operational expenses, relying instead on high precious metals prices and one-off production expansions to maintain their margins.

By-product credits drive cost reductions

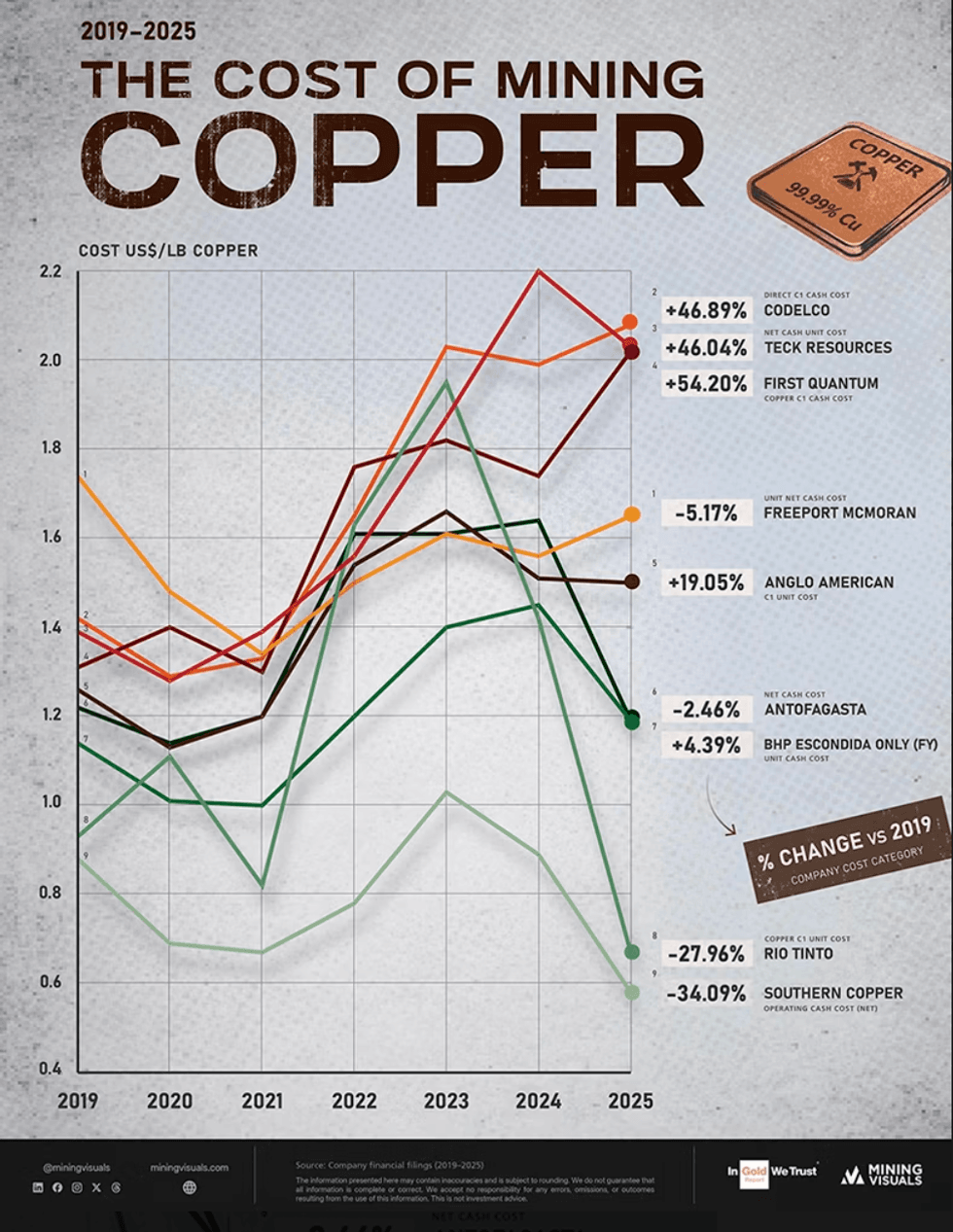

Infographic via MiningVisuals.

This financial divergence is also occurring as copper continues to set historic market highs. Copper futures on the COMEX broke records at US$6.71 per pound on May 13, 2026, while the London Metal Exchange saw prices peak at US$14,527.50 per metric ton earlier this year.

Driving this rally is a massive mismatch between supply and demand recently exacerbated by the closing of the Strait of Hormuz, which triggered a global shortage of sulfuric acid—a critical chemical reagent needed for refining.

With the International Energy Agency (IEA) projecting a 30 percent supply shortfall by 2035, the metal has become a focal point for investors tracking grid expansions, artificial intelligence data centers, and the electric vehicle transition.

Yet, a newly compiled cost-curve analysis reveals that the industry's apparent profitability is deceptive.

Consider Southern Copper (NYSE:SCCO), which reported the industry’s lowest net cash cost in 2025 at just US$0.58 per pound. While this represents a 34 percent drop from its 2019 baseline, the company’s underlying operating expenses actually rose to US$2.17 per pound.

The low net figure was entirely sustained by massive by-product credits, which expanded by US$0.34 per pound year-over-year on the back of higher zinc and silver output at its Buenavista concentrator.

Antofagasta (LSE:ANTO,OTCPL:ANFGF) deployed the same accounting cushion. Its net cash costs fell 27 percent to US$1.19 per pound purely because gold prices surged and its molybdenum output jumped 48 percent.

Other producers also relied on sheer volume to temporarily dilute their fixed overheads. Year-over-year, Rio Tinto (ASX:RIO,NYSE:RIO,LSE:RIO) slashed its 2025 net unit costs by 53 percent to US$0.67 per pound (a 27.96 percent drop against 2019), leaning heavily on a 61 percent production spike at its massive Oyu Tolgoi underground development in Mongolia.

Meanwhile, BHP (ASX:BHP,NYSE:BHP,LSE:BHP) followed suit at Escondida, lowering unit cash costs by 18 percent year-over-year to US$1.19 per pound by mining its highest-grade ore bodies in 17 years.

Base extraction costs and inflation

Where these windfalls were absent, cost lines bloated immediately against historical baselines.

Chilean state giant Codelco watched its C1 cash costs climb to US$2.08 per pound, representing a 46.89 percent increase since 2019, due to high equipment rental fees, unexpected maintenance, a seismic event at El Teniente, and a stronger Chilean peso.

First Quantum Minerals' (TSX:FM,OTCPL:FQVLF) C1 cost hit US$2.02 per pound driven by lower grades at Sentinel as well as higher employee, maintenance, and contractor costs.

At the top of the cost curve, Teck Resources (TSX:TECK.A,TECK.B,NYSE:TECK) averaged US$2.03 per pound across its portfolio, while its newly opened Quebrada Blanca mine operated at a steep US$2.67 per pound.

These premiums matter because by-product credits are highly cyclical. If gold, zinc, or molybdenum prices pull back, the net cash costs for insulated miners will instantly snap back to their true, higher baselines.

The industry cannot easily mine its way out of this dilemma. Over the last decade or more, new copper discoveries have become few and far between, and major existing mines face steadily depleting high-grade resources.

S&P Global reports that global copper supply is expected to peak by 2030 without massive structural expansions. Because moving a project from initial greenfield discovery to commercial production routinely takes 10 to 20 years, the market is structurally locked into current infrastructure.

Moving into late 2026, preliminary corporate guidance indicates that local currency appreciation will continue to drive extraction costs higher, meaning the current floor under copper prices is likely here to stay.

MiningVisuals is your go-to source for mining insights and visuals — transforming complex data into clear graphics that highlight the essential minerals building our future.

Don’t forget to follow us @INN_Resource for real-time news updates!

Securities Disclosure: I, Giann Liguid, hold no direct investment interest in any company mentioned in this article.

https://x.com/giannliguid

https://www.linkedin.com/in/giannliguid/

Featured Copper Investing Stocks

Learn about our editorial policies.