The Conversation (0)

PUKPIK / Adobe Stock

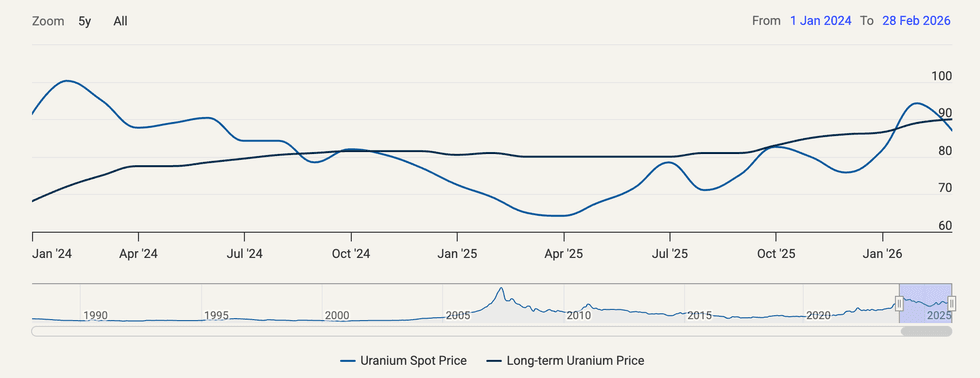

Propelled by surging nuclear demand projections, the spot U3O8 price started 2026 at just over US$80 per pound. Positive fundamentals pushed the energy fuel to US$101.41 on January 29, marking a year-to-date high.

Geopolitical instability in February and March weighed on the spot price as investor sentiment turned to safe-haven assets, and U3O8 tumbled to US$85.50 on February 5, a 15.91 percent decline over seven days.

The pressure continued through March as the war in Iran prevented shipments through the Strait of Hormuz, creating a global energy crisis. By the end of the quarter, the spot price was sitting at US$83.90, representing a 2.52 percent increase from its January start position.

Market challenges were underscored during a Bloor Street Capital virtual uranium conference on March 28.

“We've definitely had a cooling off as people have kind of stepped away and de-risked and taken money off the table in terms of not really knowing how this is all going to play out,” said John Ciampaglia, CEO of Sprott Asset Management.

“But I think the longer-term fundamentals, the story, remain very intact. And we would argue that this recent energy crisis, no matter how long it lasts, is another positive development, longer term, for uranium and nuclear energy.”

SPUT returns to market

A key feature of the quarter was the re-emergence of the Sprott Physical Uranium Trust (TSX:U.U,OTCQX:SRUUF) as an active buyer. After a six month lull tied to capital-raising constraints and macroeconomic uncertainty, the trust moved aggressively in early 2026, purchasing more than 5 million pounds year-to-date.

"When it is on, it really can go,” Ciampaglia noted.

He highlighted a rapid return of investor demand following a January prospectus renewal. Large back-to-back institutional inflows helped drive a surge in buying activity, and briefly pushed U3O8 back to US$100.

While the trust operates under a 9 million pound annual spot purchase cap, Ciampaglia underscored flexibility within its mandate, suggesting additional off-market procurement could extend its buying capacity if needed.

Long-term price sees steady growth

Although the first quarter saw volatility in the spot market, the uranium term market is sending a strong bullish signal, with the long-term contract price climbing to US$90, its highest level since 2008.

According to Ciampaglia, this benchmark, which serves as a reference for future delivery, “has been going up for the last six months,” reinforcing the upward trajectory for uranium pricing.

He noted that the increasing importance of the term price is helping to anchor the spot market. When the spot price drifts too far below long-term levels, market participants step in to arbitrage the gap.

“You’ll have participants come in, buy uranium and basically sell that uranium forward ... and keep that relationship quite tightly tethered,” he explained. This dynamic — commonly referred to as a carry trade — allows traders to capitalize on short-term weakness by locking in spreads between spot and future prices.

Uranium spot and long-term prices, January 2024 to February 2026.

Chart via Cameco.

As a result, the mechanism has acted as a stabilizing force during recent volatility, cushioning downside moves and preventing a sharper disconnect between spot and term markets.

Long-term uranium demand growing rapidly

According to industry experts who spoke at this year's Prospectors & Developers Association of Canada (PDAC) convention, held in Toronto in early March, the most telling indicator of uranium demand is not the spot market, but the amount of fuel utilities still need to contract for future years.

Grant Isaac, Cameco's (TSX:CCO,NYSE:CCJ) president and chief operating officer, noted that the volume of “uncovered requirements” — future uranium demand not yet secured by utilities — has reached record levels.

“The forward demand that has yet to come to the market has never been bigger,” he said. “Between now and 2045, that is a wall of demand that ultimately cannot be avoided.”

At the same time, utilities have not been contracting uranium at replacement rates since 2012. That means the industry has been consuming fuel faster than it has been replenishing long-term contracts.

The result is a steadily widening supply gap.

Q1 developments in the uranium market underscore a structural shift in demand that remains underappreciated, particularly as sovereign-driven agreements quietly reshape long-term supply dynamics.

According to Isaac, recent contracting activity, including major deals with India and the US, highlights “one of the most unrecognized pieces of uranium demand,” namely the strategic, off-market procurement of fuel tied to national energy security. These bilateral agreements are already translating into substantial, and often overlooked, demand.

Isaac pointed to the US government’s plan to support 10 new reactors, noting that “10 reactors with 10 years' worth of fuel is 65 million pounds of uranium ... (that) nobody had in their mind ahead of time.”

Similarly, Cameco’s agreement with India, announced in March, adds another 20 million pounds, reinforcing the scale of demand emerging outside traditional market channels.

Crucially, uranium demand is not confined to new builds. Reactor life extensions, capacity upgrades and restarts are collectively driving a “more durable demand profile ... than we have ever seen.”

At the same time, the industry faces a growing backlog of uncovered requirements, with utilities yet to secure future supply. Isaac emphasized that this forward demand “has never been bigger in the history of the uranium fuel cycle,” a trend compounded by the fact that utilities have not been contracting at replacement rates since 2012.

Q1's top uranium news stories

Q1 saw a wave of significant uranium deals and corporate developments that reinforced a shift toward long-term, strategic contracting, particularly among sovereign buyers seeking to secure future fuel supply.

The standout transaction came from Cameco, which signed a landmark agreement with India valued at approximately C$2.6 billion. The deal will see the company supply nearly 22 million pounds of uranium over a nine year period beginning in 2027, marking one of the largest bilateral supply agreements in recent years.

Beyond Cameco, the quarter also pointed to intensifying competition among global suppliers.

Kazakhstan’s state producer Kazatomprom signaled it is pursuing its own long-term supply arrangements with India, further illustrating how key buyers are diversifying supply sources through parallel negotiations.

In Canada, Denison Mines' (TSX:DML,NYSEAMERICAN:DNN) Phoenix mine in Saskatchewan’s Athabasca Basin became the first fully permitted uranium mine to enter construction in over a decade.

“We are truly ready to start construction,” Dension CEO David Cates told the Investing News Network at PDAC.

“Because our mine is an in-situ recovery mine, we have a much shorter construction timeline. We're not sinking a shaft or opening a pit. We're not building a big mill,” he said. “We're drilling a series of vertical, or near vertical, wells that are like a water well that'll go from surface into the orebody, and we're building a process plant.”

Cates went on to explain that the style of project also avoids the need for a tailings facility or a large workforce camp, which shortens the construction timeline to about two years, two to three years less than a typical underground mine.

The company is aiming for first production in 2028.

Demand dynamics and tightening supply outlook

Beyond the price volatility seen in Q1, a deeper examination of the uranium market reveals a demand landscape poised for significant expansion, shadowed by a supply side fraught with structural challenges.

Industry analysts project a substantial increase in global nuclear capacity that will inevitably strain available resources.

Speaking at PDAC, Nick Carter, executive vice president at UxC, outlined a trajectory of robust growth.

“In today's market, we have about 441 units producing about 400 gigawatts of electricity,” he noted. “By 2040 we expect that to increase by about 47 percent.” This growth, he explained, is largely concentrated in Asia, with China alone operating 60 reactors and a staggering 38 more under construction.

While Asian markets dominate the expansion, established nuclear powers are also contributing to demand.

Carter noted that Japan is seeing a steady return to service with 14 restarts, and operational improvements in France could add further pressure on fuel supplies. This rising demand is set to collide with a supply landscape that is struggling to keep pace. While 2025 saw world production reach approximately 173 million pounds, primary demand stood at roughly 204 million pounds, creating a deficit that is projected to widen significantly.

Carter’s analysis points to a looming supply gap beginning around 2030 and extending to the end of the next decade.

“Obviously, it's probably going to be a little higher, assuming some of the US reactor demand ... but overall, there's a pretty big supply gap out in the mid-2030s,” the expert stated.

The challenge, according to industry analysts, will be closing this gap.

Carter highlighted a litany of risks that plague new project development and production restarts, from underestimated capital costs and geopolitical instability to supply chain bottlenecks and regulatory delays. He gave specific examples, such as the sulfuric acid shortages that hampered production in Kazakhstan, and the political uncertainties surrounding projects in Mongolia and New Mexico, to underscore the difficulty of bringing new supply online.

“Filling that supply gap will be, in my opinion, quite challenging going forward,” Carter remarked.

Further complicating the supply picture for western markets is a fundamental shift in global trade flows.

Carter noted that a combination of Russian import bans in the US and Europe, coupled with Chinese strategic buying, has redirected vast quantities of uranium.

“China imported a massive amount of uranium, nearly 70 million pounds … that’s literally about 40 percent of the world's primary production that China has a share of in this market,” he explained.

This aggressive purchasing by Beijing and New Delhi is effectively shrinking the pool of material available to western utilities, adding a new geopolitical imperative to secure non-Russian, western-aligned supply chains.

Looking ahead to the remainder of 2026, the market is expected to remain influenced by financial players rather than utilities demand. While funds like the Sprott trust have been active buyers, their purchasing capacity is finite.

However, the UxC analyst pointed to potential new sources of demand, including small-scale producers that may be forced to buy on the spot market to meet commitments, and the continued emergence of new investment vehicles drawn by the artificial intelligence narrative around nuclear power.

The outlook suggests a market defined by competing forces: bullish long-term demand underpinned by structural supply constraints, set against a near-term environment of financial speculation and shifting geopolitical realities.

Don’t forget to follow us @INN_Resource for real-time updates!

Securities Disclosure: I, Georgia Williams, hold no direct investment interest in any company mentioned in this article.

Editorial Disclosure: The Investing News Network does not guarantee the accuracy or thoroughness of the information reported in the interviews it conducts. The opinions expressed in these interviews do not reflect the opinions of the Investing News Network and do not constitute investment advice. All readers are encouraged to perform their own due diligence.

From Your Site Articles

- Uranium Stocks: 5 Biggest Companies ›

- Top 10 Uranium-producing Countries ›

- Uranium Reserves: Top 5 Countries ›

- When Will Uranium Prices Go Up? ›

Related Articles Around the Web

TSXV:AEC

https://twitter.com/INN_Resource

https://www.linkedin.com/in/georgia-williams-15845447/

gwilliams@investingnews.com

Featured Uranium Investing Stocks

Learn about our editorial policies.