The Conversation (0)

Mujhid_Muneer / Adobe Stock

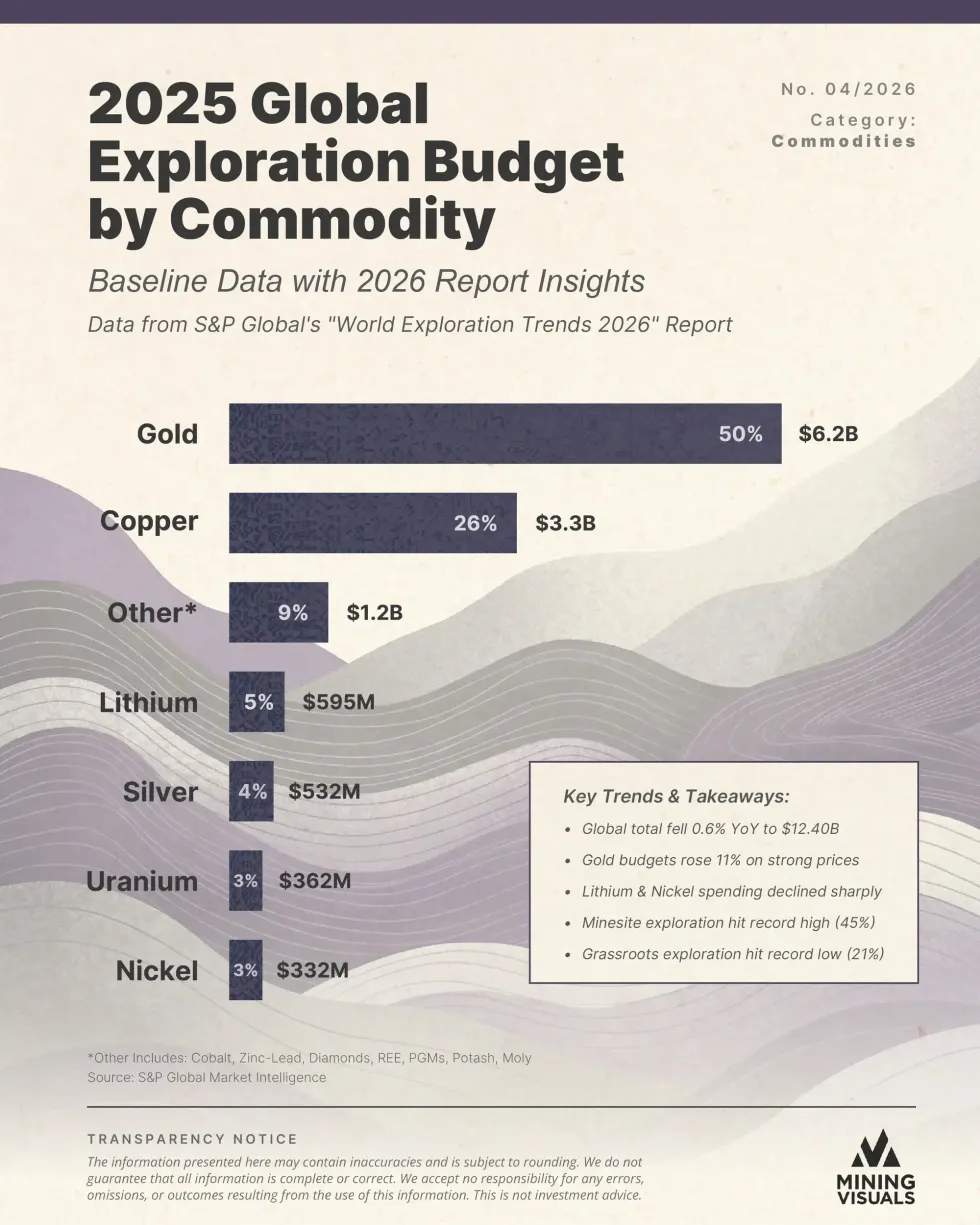

The global mining industry has decisively pivoted toward safe havens, funneling half of its entire exploration budget into gold while abandoning early-stage grassroots discoveries at a record pace.

According to the newly released "World Exploration Trends 2026" report from S&P Global Market Intelligence, total nonferrous exploration budgets dipped 0.6 percent year-over-year to US$12.40 billion in 2025.

A graph shows 2025 global exploration budgets for various commodities.

Infographic via MiningVisuals.

Yet the relatively flat top-line figure masks a severe capital rotation taking place.

Miners are overwhelmingly prioritizing sure bets. Minesite exploration, which includes drilling at or immediately adjacent to existing, proven deposits, surged to a record high, accounting for 45 percent of all exploration dollars spent globally.

Conversely, generative grassroots exploration, the inherently risky search for entirely new deposits in untested geographical areas, collapsed to an all-time low of just 21 percent.

The industry’s flight to safety is heavily anchored by precious metals. Driven by bullion prices that smashed through US$4,600 an ounce in early 2026 amid escalating geopolitical tensions and relentless central bank accumulation, gold exploration budgets surged 11 percent.

The metal captured a massive 50 percent of the total global budget, representing US$6.2 billion in deployed capital. This singular surge in gold spending single-handedly offset steep funding cuts across the broader commodities complex.

The most dramatic casualties of this capital rotation were battery metals. Following a period of intense hype and elevated spending, lithium and nickel experienced sharp declines in exploration allocations. Lithium captured just US$595 million, or 5 percent of the global budget, while nickel accounted for a mere 3 percent at US$332 million.

The pullback primarily stems from weak short-term market conditions and a brutal financing environment for the junior mining companies that traditionally spearhead critical mineral discoveries.

Copper, meanwhile, held its ground as a structural necessity. The industrial metal commanded a strong second place, capturing 26 percent of the global exploration budget at US$3.3 billion.

Capital allocation for copper continues to edge higher, supported by long-term demand expectations tied to global electrification, grid expansion, and renewable energy infrastructure.

Despite the cautious deployment of capital in the field, liquidity is still entering the sector. Funds raised by junior and intermediate companies actually more than doubled year-over-year to US$21.43 billion.

However, this capital remained highly selective, directed heavily toward advancing existing project development rather than funding greenfield exploration.

This evaporation of risk appetite presents a structural dilemma for the global economy. Because bringing a new mineral discovery into commercial production routinely takes more than a decade, the lack of investment in grassroots exploration suggest an incoming pipeline crunch.

MiningVisuals is your go-to source for mining insights and visuals — transforming complex data into clear graphics that highlight the essential minerals building our future.

Don’t forget to follow us @INN_Resource for real-time news updates!

Securities Disclosure: I, Giann Liguid, hold no direct investment interest in any company mentioned in this article.

https://x.com/giannliguid

https://www.linkedin.com/in/giannliguid/