AddStylerz / Adobe Stock

The first quarter of 2026 has been a rollercoaster ride of volatility for the gold price.

The precious metal's strong fundamentals helped it break above the US$5,000 per ounce level for the first time, and during the period it traded in a range of US$4,100 to nearly US$5,600.

As global financial and geopolitical uncertainty shake up the broader markets and the historical world order, gold is gaining support from safe-haven demand while feeling the pressure of a stronger US dollar.

What happened to the gold price in Q1?

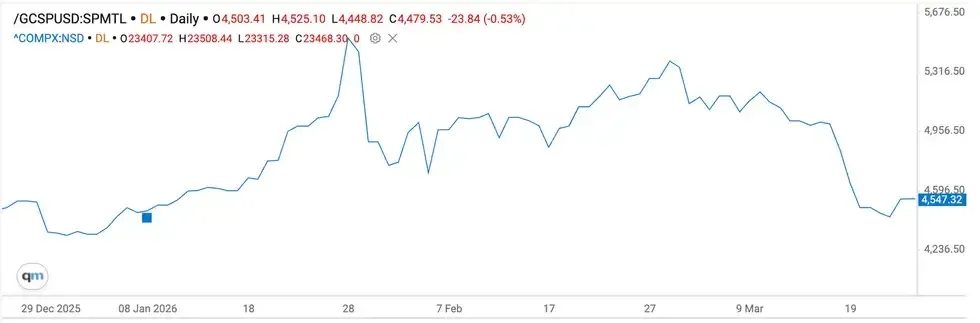

Gold began the year at US$4,384.46 on January 2, and continued to rise throughout the first month of the year, breaking to a new record high of US$5,589.38 on January 28.

Gold price, Q1 2026.

Chart via the Investing News Network.

Its upward trajectory didn’t last long, however, and February was a much more volatile month for gold.

“A big part of what you saw with the run up in January and the selloff at the end of January was the role of the Comex active February gold contract,” Jeffrey Christian, managing partner at CPM Group, told the Investing News Network (INN) in a March interview, adding that upwards of 200 million ounces of gold futures contracts were bought in February.

Gold slipped to the US$4,750 mark on February 1, and the yellow metal spent much of the first half of the month trying to break back above the psychologically important US$5,000 level. The second half of February saw gold on a more steady upward trend, closing at a monthly high of US$5,278.10 on February 28.

“In addition to that, you saw tremendous amounts of gold bought by investors in exchange-traded funds (ETFs). So these are not necessarily traditional physical gold investors. These are people who are watching the gold price rise since August, saying, ‘I’ve got to get a piece of that,’” explained Christian. “So you saw a tremendous amount of gold being bought by investors in January, interestingly enough, while investors were selling their silver ETFs.”

The World Gold Council (WGC) reports that physically backed gold ETFs saw US$5.3 billion in inflows during February, the strongest two month start to a year and the ninth consecutive monthly increase.

The metal closed even higher at the start of March, rising to a high of US$5,418.71 before closing the day at US$5,383.22. However, investors lost their appetite for gold soon after that, and March quickly became another volatile month for the precious metal. Gold closed down below the US$5,100 mark by March 5.

Gold continued to decline further during the month, and by March 16 it had fallen below the key psychological US$5,000 mark to as low as US$4,977.09 before settling the trading day at US$5,006.44. The biggest slide came later in the week as the price of gold fell off a cliff to below the US$4,500 level on March 20.

The price sank to US$4,100 on the morning of March 23, the lowest level of the quarter. The drop also represented the steepest weekly decline in 40 years. Iran’s ongoing attacks in the Strait of Hormuz effectively blocked global oil trade in the region and caused investors to move out of equities and liquify gold to cover losses.

March 25 saw gold back up above the US$4,500 level as the Trump administration proposed a 15 point peace plan and a potential one month ceasefire to Iran; however, Iranian leaders rejected the deal.

What were the biggest drivers of the gold price in Q1? Two of the greatest factors determining the value of the yellow metal during quarter were which direction the US Federal Reserve would take interest rates for 2026, and the breakout of the Iran war in the Middle East. Interestingly, these two drivers are inextricably linked together.

Gold and US monetary policy

At the start of 2026, the prevailing sentiment among Fed watchers was that the risk of higher inflation still needed to be balanced with the need to support the American job market. For that reason, the consensus among experts was that rate cuts were still on the horizon, just not until early in the second half of the year.

Adding to projections for lower rates was US President Donald Trump’s feud with the Fed.

On January 9, the Department of Justice targeted Fed Chair Jerome Powell with grand jury subpoenas concerning a criminal indictment. The move further strengthened the assumption that Trump would install a dovish new Fed chair once Powell’s term came to an end in May, although he denied any involvement or knowledge of the investigation.

“I don’t know anything about it, but he’s certainly not very good at the Fed, and he’s not very good at building buildings," the president said when asked about the probe and Powell by NBC News.

The potential for less restrictive US monetary policy and the uncertainty over Fed independence prompted investors to seek safe-haven assets and weakened the US dollar, providing significant support for gold early in the quarter.

However, Trump’s nomination of the more hawkish Kevin Warsh, a former Fed governor, to replace Powell triggered a massive selloff in gold as investors became less convinced that the White House would soon be dictating US monetary decisions. On the flip side, weak US labor and economic data helped fuel sentiment that even with Warsh at the wheel, the Fed may need to cut interest rates later in 2026 to revive the US economy.

Trump’s ongoing tariff tensions also complicated matters for the Fed as higher costs for goods translate into higher inflation. In addition, the threat of unresolved trade wars and Trump’s fixation on taking over Greenland gave further justification to central banks' gold-buying schemes.

Gold and the Iran war

The geopolitical uncertainty and volatility created by the Trump administration’s actions in Venezuela and the Middle East has also been a major drive of the gold price this quarter.

Soon after the US military operation that removed Nicolás Maduro from his seat of power in Venezuela, Trump began warning that the US would intervene in Iran if its leaders did not halt the execution of anti-government protesters. Iran responded with threats of strikes on US bases. In early February, the tensions escalated when the US shot down an Iranian Shahed-139 drone approaching a US aircraft carrier in the Arabian Sea.

Then, on February 28, the US and Israel launched Operation Epic Fury, targeting multiple locations in Iran.

At first, the conflict was a major boost for gold on the basis of safe-haven demand, pushing the gold price up to nearly US$5,400 as a full-scale war broke out in the first week of March.

However, the war rally in gold was short-lived as the conflict bled into the wider region of the Middle East and resulted in Iran effectively blocking oil transport through the Strait of Hormuz.

With oil prices surging past US$100 per barrel for the first time since 2022, the consensus is that the cost of goods is bound to rise across a broad swath of sectors. This would dramatically change the calculus for the Fed at its upcoming meetings. On top of that, US economic data released near the end of the first quarter points to stickier inflation for longer, especially if the Iran war does not find a speedy conclusion.

"Gold is not responding to war. Gold is simply responding to the fact that the Federal Reserve might not lower interest rates as anticipated,” Alex Ebkarian, co-founder of Allegiance Gold, told INN in a March interview.

He sees a trifecta of factors influencing inflation and rates on the back of the Iran war and the effective blockade of the Strait of Hormuz, namely: higher oil prices, higher fertilizer prices and the potential for a drawn-out conflict that would add to the US debt load — which is already at unmanageable highs.

“I think that the Strait of Hormuz is the battlefield, not only from an oil perspective, but the dominance of currency,” said Ebkarian. "And I think that battleground is important for people to pay attention and understand how everything is connected, from the dollar, oil, gold and the market in general.”

This dilemma is very much on the minds of Fed officials, as reflected in the central bank's March 18 rate announcement, which saw the central bank’s board members vote to hold rates steady for a second time this year.

The broader implications for energy markets and inflation have begun to set in for not only economists and policymakers, but also investors. The potential for rates to remain on hold or even increase is now placing downward pressure on gold, with the price sinking back down to the US$4,500 mark near the end of the quarter.

The impact of the Iran war on the gold market also has the potential to impact gold miners.

“War is very inflationary. I mean, look at the oil price. Look at what it's doing. This is the reason why the gold price is correcting, and especially the miners ... half of a lot of these miners' costs, especially if they're an open-pit project, is oil,” David Erfle, editor and founder of Junior Miner Junky, told INN in a March interview. “So when you have a strong oil price, that cuts into their margins, even though they've been fantastic lately.”

However, Erfle remains bullish moving forward, commenting later in the conversation, “I've said in the past that 2025 was the perfect storm for gold. Now it's a Category 5 hurricane in 2026.”

Gold's fundamentals remain strong

In the near term, the gold price may face serious headwinds from geopolitical unrest in the Middle East.

However, the long-term view among most analysts is that the yellow metal’s fundamentals remain strong, with significant price appreciation still on the horizon. “Longer term, all of those economic and political conditions that are the increased risk and the increased uncertainty and the increased volatility — they're all in place still; that's probably going to mean higher gold and silver prices for the foreseeable future,” Christian told INN.

Ebkarian agrees. “I think we're in the fourth or fifth inning in terms of the bull market, because the fundamentals are the same," he said. “We have an unprecedented amount of deficit spending, and the debt is growing,” he continued, adding that the US deficit is sitting at close to US$2 trillion. At the same time, the country's national debt was close to US$39 trillion as of March, adding about US$1 trillion in the past five months.

Central banks have been a major gold price driver over the past few years, and data published by the WGC on March 3 indicates that they remained active during the first month of the year.

In January, they added a net 5 metric tons of gold to their reserves. That represents a slow start to the year compared to the average of 27 metric tons added each month in 2025. However, the WGC points out that while the momentum may have eased in the face of a higher gold price, the base of demand is broadening as central banks such as the Bank Negara Malaysia and the Bank of Korea begin to make their first gold purchases in years.

“We have pressure on lowering the interest rates, but yet, quietly in the background, central banks continue to basically buy more and more gold,” said Ebkarian.

Gold price forecast for 2026

It’s hard to pin analysts down on making near-term gold price predictions in the Trump era, but most projections see elevated prices for the precious metal by the end of the year.

In late January, as the price was soaring, Goldman Sachs (NYSE:GS) raised its year-end 2026 gold target to US$5,400. In late February, right before the Iran war broke out, JPMorgan Chase (NYSE:JPM) forecast that gold would reach US$6,300 by the end of this year, citing strong central bank demand and diversification of the investor base.

Meanwhile, ING sees gold averaging US$5,190 for 2026, and Scotiabank is even more conservative, calling for the precious metal to average US$4,100 for the year.

Gold’s decline down to the US$4,300 level as Q1 comes to a close may change these outlooks. Ed Yardeni, president of Yardeni Research, told CNBC in late March that even though he’s lowered his year-end 2026 forecast from US$6,000 to US$5,000 per ounce, his firm is “sticking with $10,000 by the end of the decade."

Don't forget to follow us @INN_Resource for real-time updates!

Securities Disclosure: I, Melissa Pistilli, hold no direct investment interest in any company mentioned in this article.

Editorial Disclosure: The Investing News Network does not guarantee the accuracy or thoroughness of the information reported in the interviews it conducts. The opinions expressed in these interviews do not reflect the opinions of the Investing News Network and do not constitute investment advice. All readers are encouraged to perform their own due diligence.

NYSE:BAC

https://twitter.com/INN_Resource

https://www.linkedin.com/in/melissa-pistilli-865271a9/

mpistilli@investingnews.com

The Conversation (0)

Featured Gold Investing Stocks

Learn about our editorial policies.