Dec. 02, 2025 01:55PM PST

Max Zolotukhin / Adobe Stock

The gold price saw incredible gains in 2025, rising from US$2,600 per ounce to a record high of over US$4,300.

Gold has moved up in nearly every month of the year, and is on track for its biggest annual gain in 46 years.

Various factors have lent support, including ongoing geopolitical instability in Eastern Europe and the Middle East, US President Donald Trump’s volatile trade policies and the resulting uncertainty in global financial markets. A reversal in the US Federal Reserve’s monetary policy is another major factor that has influenced the gold price this year.

Read on for more on what moved the gold price in each of the year’s four quarters.

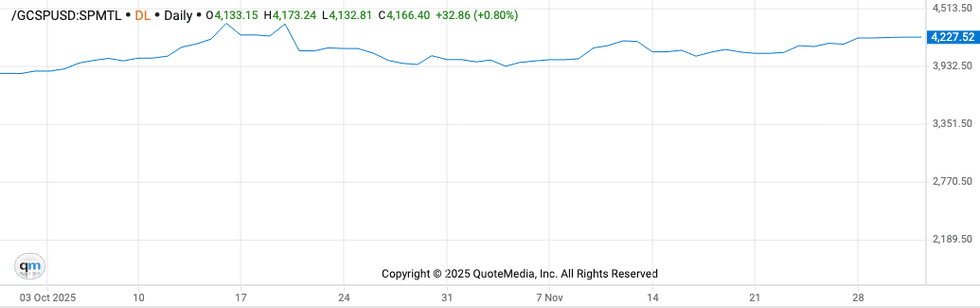

Gold price in Q4

The gold price began Q4 at US$3,865.10, but quickly shot to an all-time high of US$4,379.13 on October 17. The surge was fueled by a number of circumstances supportive of safe-haven demand and store of value.

First up was the deepening trade war between the US and China.

In response to US lawmakers demanding broader bans on equipment sales to Chinese chipmakers, President Xi Jinping’s government announced further rare earth element export restrictions. The action spurred Trump to respond by threatening 100 percent tariffs on Chinese goods and export controls on critical software.

Other forces behind gold’s impressive rally in the fourth quarter included the US government shutdown and expectations that the Fed would begin reducing interest rates. At the same time, central banks continued to be net buyers of gold amid increased gold exchange-traded funds (ETF) inflows.

Gold price, Q4 2025.

Chart via the Investing News Network.

By October 27, the price of gold had fallen to its quarterly low of US$3,897.30. However, the yellow metal managed to rise once again, closing out the month above the US$4,000 level.

Gold took another run at its record high in the second week of November as the longest US government shutdown in history came to an end and labor market weakness in the US primed expectations of further Fed rate cuts in December. The precious metal reached US$4,242.50 on November 13 before falling back below US$4,100 the next day.

The long-delayed release of September US jobs data on November 20 also placed downward pressure on gold as the numbers were stronger than expected. Nonfarm payrolls increased by 119,000, more than double the 50,000 gain analysts had projected. The report reduced expectations of a Fed rate cut in December.

The price of gold fell as low as US$4,022 the next day. However, the last week of November saw gold on another upward trend as the likelihood of a December Fed rate cut increased, hurting the US dollar.

New York Fed President John Williams said continued weakness in the labor market makes the case for a December rate cut feasible, and Fed Governor Christopher Waller also mentioned a December cut would be appropriate.

While the US Department of Labor will not be releasing an October jobs report due to the government shutdown, a report from job placement firm Challenger, Gray & Christmas shows that US employers shed 153,074 jobs in October. That’s up 183 percent from September 2025 and 175 percent from October 2024.

The latest consumer confidence survey also hasn't helped, especially since numbers have been down for 10 consecutive months, signaling the potential for a recession. “Consumer confidence tumbled in November to its lowest level since April after moving sideways for several months,” said Dana M. Peterson, chief economist at the Conference Board. “All five components of the overall index flagged or remained weak.”

On November 28, gold broke above the US$4,200 level again. By December 1, it had reached its highest level in six weeks, hitting US$4,263 before settling down to US$4,237 at the end of the trading day.

How did gold perform for the rest of the year?

Gold price in Q1

Gold gained 20 percent in Q1 and closed above US$3,000 for the first time ever on March 18. The precious metal’s strong performance during the period is linked to global uncertainty surrounding Trump's second term.

Trade policy was at the center of those concerns. Soon after Trump's inauguration, his administration applied tariffs to imports from Canada and Mexico, only to press pause two days later and delay implementation until March.

The seesaw between on-again, off-again tariff announcements continued throughout the quarter alongside rising tensions in the Middle East and Eastern Europe, adding to market instability and bolstering gold’s safe-haven appeal.

This was highly evident in what the Word Gold Council (WGC) called “strong global inflows” into gold ETFs.

Gold price, Q1 2025.

Chart via the Investing News Network.

“There has been a huge spike in the movement of physical gold from around the world into US depositories," said David Barrett, CEO of EBC Financial Group UK, in comments to the Investing News Network (INN) at the time.

"This seems to have been driven by the global political stress and potential tariff impacts. The amounts involved have caused disruption in the real demand and promoted new buyers as well,"

Gold price in Q2

The gold price continued to set new record highs in the second quarter of 2025, breaking through the US$3,500 level briefly on April 21 before closing the quarter slightly lower at US$3,434.40.

Trump’s tariffs were once again the main theme influencing the metal's gains through the quarter. On April 2, Trump declared “Liberation Day,” an executive order applying tariffs on a broad range of imports coming from most US trade partners. The subsequent global market meltdown caused US debt holders, such as Japan and Canada, to sell US treasuries, which led to higher yields on 10 year bonds. Investors in turn sought the safety of gold.

On the back of those factors, the WGC’s June ETF report shows that ETF flows in the first half of 2025 were the highest semiannual inflows since the first half of 2020.

Gold price, Q2 2025.

Chart via the Investing News Network.

“The bond market understands that Washington is so broken and the debt situation is so bad," explained Chris Temple, founder, editor and publisher of the National Investor, in a June 19 interview with INN. "It varies in degrees compared to other countries, but everybody’s in the same boat. That’s why gold all of a sudden … gold is the safe haven now, even more than treasuries. And I don't think a lot of people every thought they'd see that again."

Gold price in Q3

Gold set another record during Q3, rising over 15 percent to a quarterly high of US$3,858.41 on September 30.

The substantial rally was attributed to declining yield curves, US monetary policy and the weakening dollar. Gold traditionally has had an inverse relationship to the dollar, a trend that has benefited the metal immensely this year.

In this vein, the 25 basis point rate cut from the Fed on September 17 was a major catalyst. Some analysts believe it’s a signal to investors that the economy may be on the verge of a stagflationary environment.

This is reflected in WGC’s reporting of record ETF inflows to the tune of US$26 billion for the third quarter, with North American markets accounting for US$16.1 billion.

Gold price, Q3 2025.

Chart via the Investing News Network.

“At the heart of all of this is a question around the role of the dollar, the role of dollar-based assets and diversification in portfolios. And that’s where people are looking at alternatives. Alternatives that can give you safe-haven characteristics like gold,” Joe Cavatoni, the WGC's senior market strategist, Americas, said in a mid-September INN interview.

Investor takeaway

Safe-haven investment demand has been the key driver for gold in 2025.

Investors have sought refuge in precious metal throughout the year as geopolitical tensions, Trump-related trade turmoil and a worsening economic outlook have sparked volatility in the stock market.

In the first three quarters of the year, the WGC reported 1,556 metric tons of gold investment demand, representing US$161 billion in gold assets. That’s only 6 percent below the record reached in the first three quarters of 2020.

Central banks have continued to increase their physical holdings as a potential buffer against a global economic downturn. The most recent data on central bank gold buying from the WGC shows that they added 634 metric tons of gold to their coffers during the first three quarters, with more than one-third of those purchases occurring in Q3.

As the conditions for gold’s current year-long rally become further entrenched, investors can reasonably expect this year’s story to be next year’s story, but with even higher gold prices.

Don't forget to follow us @INN_Resource for real-time updates!

Securities Disclosure: I, Melissa Pistilli, hold no direct investment interest in any company mentioned in this article.

Editorial Disclosure: The Investing News Network does not guarantee the accuracy or thoroughness of the information reported in the interviews it conducts. The opinions expressed in these interviews do not reflect the opinions of the Investing News Network and do not constitute investment advice. All readers are encouraged to perform their own due diligence.

From Your Site Articles

- When Will Gold Stocks Go Up? Experts Talk Outlook for Equities and Price ›

- Sprott Commodities Outlook: Trends for Uranium, Copper, Gold and More in 2025 ›

- Gold Price Today | Live Gold Price Chart & Historical Data ›

Related Articles Around the Web

https://x.com/INN_Resource

https://www.linkedin.com/in/melissa-pistilli-865271a9/

mpistilli@investingnews.com

The Conversation (0)

Featured Gold Investing Stocks

Learn about our editorial policies.