The Conversation (0)

tonstock / Adobe Stock

The global lithium market is undergoing a massive structural reversal.

Following a multi-year period of severe oversupply that crushed spot prices, the critical battery metal is now aggressively tightening, with major financial institutions projecting a steep supply deficit by 2026.

"The question is no longer if the lithium market will face a supply shortage, but rather how aggressively the supply chain will struggle to meet compounding demand," Mining Visuals noted in a recent report.

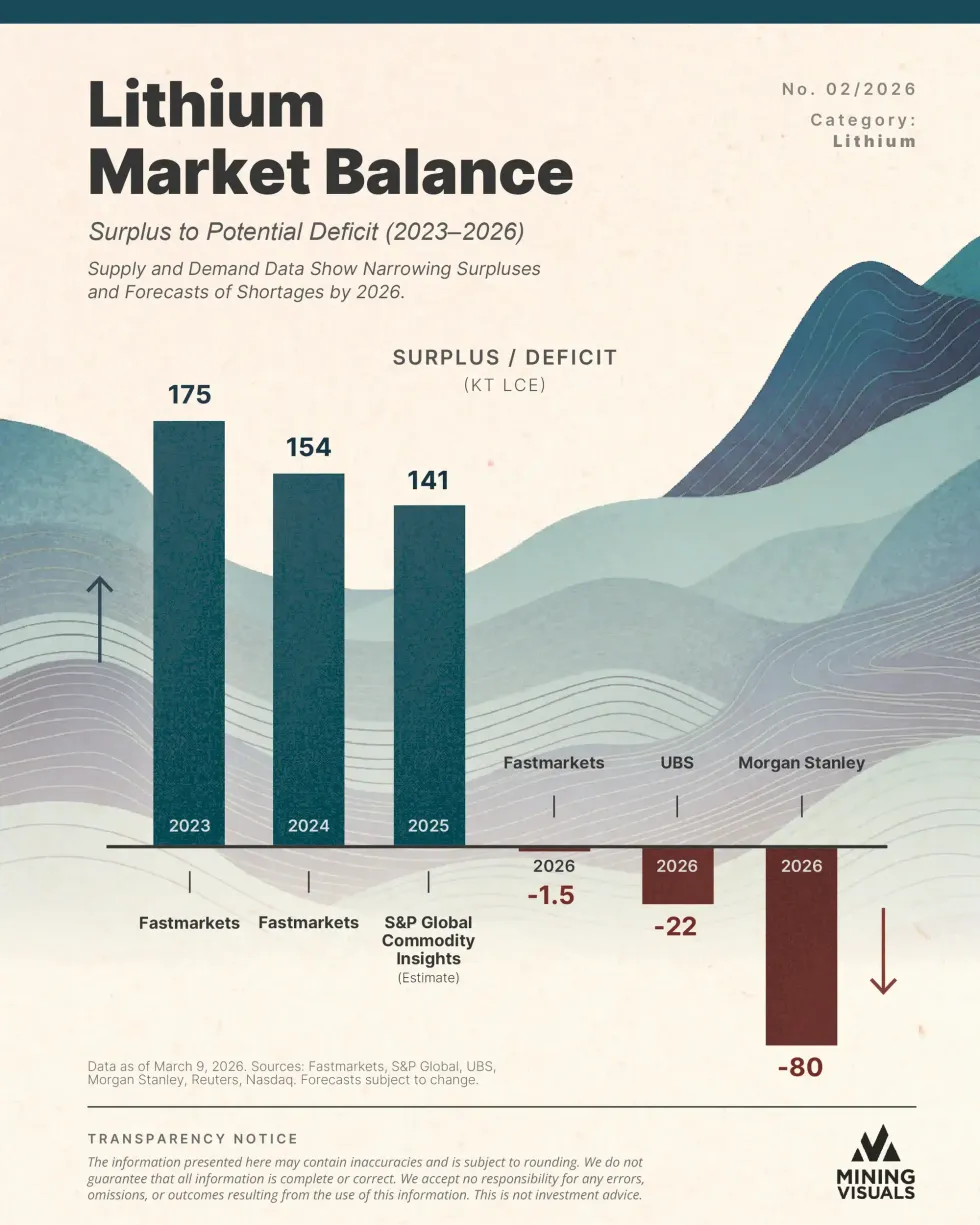

A surplus contraction

Bar graph showing lithium market surplus data from 2023-2026.

Infographic via MiningVisuals.

Between 2022 and 2024, the lithium market was defined by a massive wave of excess supply. A surge of new production, primarily from operations in Australia and China, flooded the market just as short-term demand growth temporarily cooled.

The resulting imbalance was severe. According to Fastmarkets, the market surplus peaked at approximately 175,000 tons of Lithium Carbonate Equivalent (LCE) in 2023. This excess inventory crushed spot prices, which plummeted by more than 80 percent from their late-2022 highs, bottoming out at just $8,259 per ton in China by June 2025.

However, the same price collapse triggered a fierce market correction. As prices fell below the cost of production, major Chinese operations curtailed capacity, Australian spodumene miners halted output, and global exploration budgets were heavily slashed.

Consequently, the surplus is shrinking rapidly. S&P Global Commodity Insights forecasts the surplus will narrow to 141,000 tons LCE in 2025, driven by a 13.5 percent year-over-year increase in consumption.

The definitive pivot arrives in 2026, where consensus firmly points to a structural deficit.

EV resiliency and policy risks

While supply was aggressively reigned in throughout 2025, the underlying demand drivers accelerated.

Global EV sales rose 22 percent in 2025, maintaining their position as the primary demand driver, consuming roughly 70 percent of total lithium output.

However, energy storage systems (ESS) are rapidly emerging as the swing factor capable of tightening global balances independently. Battery energy storage demand grew an explosive 51 percent in 2025, lifting storage to about a fifth of total global battery demand.

This growth is driven by grid reliability upgrades and the massive power requirements of expanding AI infrastructure.

In the US, the energy storage industry installed a record 57.6 GWh of new capacity in 2025—four times what the industry installed just three years ago. China dwarfed that figure, with 65 GWh of grid-scale battery energy storage entering operation in December 2025 alone.

On the policymaking side, meanwhile, governments in recent years have increasingly treated critical minerals less as inputs and more as strategic assets.

In the US, a Section 232 action focused on critical minerals concluded that reliance on imports poses a threat to national security, opening the door to price floors, tariffs, and negotiated import frameworks.

Furthermore, the US launched "Project Vault" in February 2026, a US$12 billion public-private initiative designed to procure and store critical minerals, including a strategic lithium reserve.

Simultaneously, supply unreliability is injecting a heavy risk premium into the market.

Zimbabwe, which produces roughly 10 percent of global mined lithium, abruptly suspended exports of raw lithium earlier this year to force domestic processing.

In China, regulatory issues have delayed the restart of CATL's (SZSE:300750,HKEX:3750) massive Jianxiawo lepidolite mine, removing a key source of supply from the market.

Pricing in the pivot

Markets are forward-looking, and the shift from glut to deficit is already being aggressively priced in.

Between early December 2025 and late January 2026, spot battery-grade lithium carbonate prices rose from approximately US$13,433 per metric ton to US$26,278, a 95 percent increase.

Spodumene prices have followed suit, climbing above US$2,000 per metric ton for the first time since late 2023.

While the rebound in prices has improved project economics, a meaningful supply response is expected to lag significantly. During the prolonged market downturn, feasibility studies for new projects dropped from dozens annually to fewer than 10 in 2025.

With demand compounding across multiple sectors and new supply constrained by lengthy development timelines and geopolitical maneuvering, the era of cheap, abundant lithium appears to be decisively over.

MiningVisuals is your go-to source for mining insights and visuals — transforming complex data into clear graphics that highlight the essential minerals building our future.

Don’t forget to follow us @INN_Resource for real-time news updates!

Securities Disclosure: I, Giann Liguid, hold no direct investment interest in any company mentioned in this article.

https://x.com/giannliguid

https://www.linkedin.com/in/giannliguid/