The Conversation (0)

Jul. 13, 2026 02:00PM PST

Fact CheckedThis article has been reviewed and updated according to INN's rigorous fact-checking process. Our staff editors verify all articles against information and data from primary sources, reputable publishers and experts.

mizar_21984 / Adobe Stock

Zinc has performed better than market watchers expected so far in 2026. While the base metal's price has seen some volatility, it ultimately posted a modest increase in the first half of the year.

Demand for zinc is primarily tied to the housing and manufacturing sectors due to its use in the making of galvanized steel. Both sectors are influenced by interest rates and inflation.

While rates have been relatively steady over the past year, inflation surged during the first six months of 2026 as the US-led invasion of Iran put pressure on energy prices.

Global supply chains have also been disrupted, with hundreds of ships unable to leave the Persian Gulf.

What happened to the zinc price in H1?

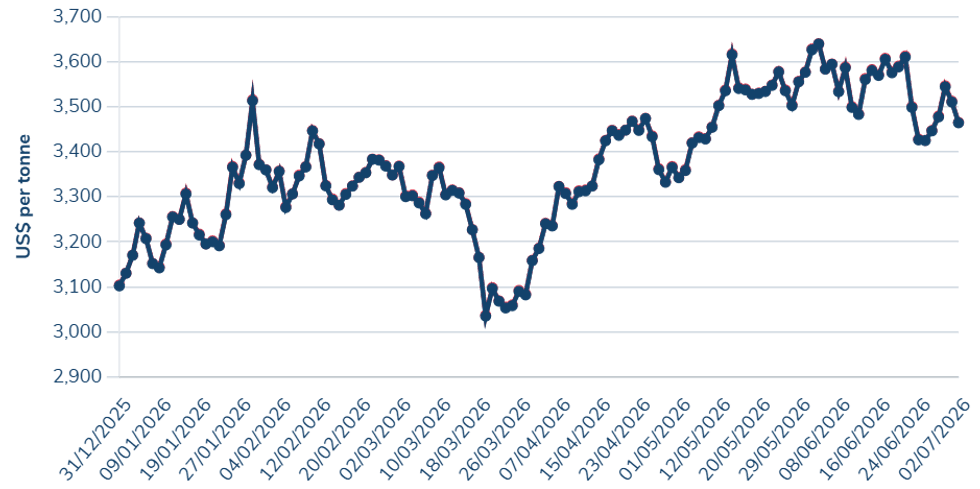

The standard three month zinc contract on the London Metal Exchange (LME) started the year at US$3,127 per metric ton (MT) on January 2. From there, it had several price swings before reaching a high of US$3,412 on January 29.

Throughout February and the start of March, zinc remained rangebound between US$3,200 and US$3,400. After March 10, the price fell sharply, plummeting to a year-to-date low of US$3,040 on March 24.

Zinc price, December 31, 2025 to July 2, 2026.

Chart via the London Metal Exchange.

After that, the zinc price regained momentum and climbed to US$3,472 on April 24; it then pulled back below US$3,400 before continuing to climb to a year-to-date high of US$3,641 on June 2.

As of June 25, the price of zinc was sitting at US$3,435.

Zinc's H1 supply/demand dynamics

Zinc has largely been dominated by a supply-side narrative in 2026. At the start of the year, the expectation was that the sector would shift into a surplus; however, that excess material has not yet materialized.

In an email to the Investing News Network, Ruilin Wang, associate director, copper-zinc, at S&P Global Energy, said that concentrate availability remains tight and that zinc has shifted into a deficit: “The view began to shift as early as February to March, as spot treatment charges declined further, imported concentrate availability into China weakened and geopolitical risks increased concerns over raw material supply."

By April, the refined market deficit was projected at 67,000 MT, rising to 87,000 MT by the end of May.

The shift in zinc market dynamics has largely occurred on the supply side, with Wang noting that it reflects both structural issues within the market and disruption-related factors.

On the mining side, Glencore's (LSE:GLEN,OTCPL:GLCNF) first quarter report shows a 17 percent decline in zinc production. It came to 176,900 MT, down from 213,600 MT in the first quarter of 2025.

The company attributes this decrease to the Lady Loretta mine in Australia entering the end of its life in late 2025, as well as lower contributions from the Kazzinc mine in Kazakhstan due to feedstock sequencing.

Similarly, Teck Resources (TSX:TECK.A,TECK.B,NYSE:TECK) saw its zinc production fall to 106,000 MT in Q1, down from 117,000 MT in the same period in 2025 due to lower grades at its Red Dog mine in Alaska.

In its Q1 results, the zinc producer also notes that disruptions to global mine supply have caused production growth estimates to trend toward the negative. Teck said it expects the concentrate market to remain constrained due to lower production from mining operations. The scarcity of concentrate has also caused downstream problems for smelting operations, with treatment charges dropping to low and even negative levels.

Wang explained that the overall impact of lower treatment charges varies by region.

“Chinese smelters have been the main beneficiaries, supported by strong by-product revenues (high sulfuric acid prices), which help offset feedstock cost pressures,” she said. Because of this, Chinese operations have been able to maintain high utilization rates, with refined output growing by 5.7 percent during the January to April period.

Outside of China, the story is different.

Smelters are challenged by high energy prices and don’t have the same by-product support to offset lower charges. This issue has led to further curtailments, including Nyrstar’s (EBR:NYR) decision to carry out maintenance at its Budel smelter in the Netherlands. Operations at the site were placed on care and maintenance twice previously, in 2022 and again in 2024, as the zinc market struggled with high costs and low margins.

The plant produces more than 300,000 MT of refined zinc annually.

When it comes to zinc demand, not much has changed. In China, demand remains weak as the property sector has yet to rebound, creating significant headwinds to increasing galvanized steel uptake.

Outside China, demand has exceeded supply, contributing to the market deficit. The US market has managed to stay in balance, but Wang noted that restocking efforts have been offset by inflationary concerns.

Zinc price forecast for 2026

The zinc narrative paints a picture of two separate markets emerging.

In China, supply has continued to be strong, with upgraders being able to stay profitable through by-product sales. The west has seen stronger demand and lower inventories.

“Physical availability remains constrained outside China, with LME inventories at critically low levels and increasingly concentrated in Asia, while western warehouse stocks have been largely depleted. This has been reinforced by sharp increases in canceled warrants, signaling tightening prompt availability in western markets,” Wang said.

According to Wang, arbitrage from Shanghai to LME warehouses has also been unfavorable for exports, as LME prices have consistently remained stronger than those in China.

“Although this creates an incentive for Chinese exports, the arbitrage window has not yet opened, meaning western markets are not being relieved by Chinese supply flows," she explained.

"A projected move toward global surplus beyond 2027 would gradually ease regional tightness."

Additionally, western market tightness, along with supply curtailments, is creating the possibility for supply shocks and short-term vulnerability. Likewise, Wang suggested that policies designed to help create critical minerals stockpiles, like Project Vault, may cause further constraints as long-term offtakes remove physical metal from the market.

Where does that leave the zinc market as the second half of the year begins?

Zinc surplus expectations haven't come to fruition in 2026; in fact, the market has headed in the other direction. The supply side hasn’t kept up, and it could be some time before that begins to take place.

New zinc supply is coming, including Ivanhoe Mines' (TSX:IVN,OTCQX:IVPAF) Kipushi mine in the Democratic Republic of Congo, which is expected to deliver 240,000 to 290,000 MT in 2026. However, for the rest of the year, Wang suggested that the price will remain elevated, with the annual average coming in around US$3,300 per MT.

“We expect zinc prices to remain supported in the second half of 2026, but with a shift from the strong rally observed in Q2 to a more balanced trajectory … we expect H2 prices to stay elevated but more rangebound, with volatility driven by incremental changes in smelter operations, inventory flows and macro signals,” she said.

Don’t forget to follow us @INN_Resource for real-time news updates.

Securities Disclosure: I, Dean Belder, hold no direct investment interest in any company mentioned in this article.

Editorial Disclosure: The Investing News Network does not guarantee the accuracy or thoroughness of the information reported in the interviews it conducts. The opinions expressed in these interviews do not reflect the opinions of the Investing News Network and do not constitute investment advice. All readers are encouraged to perform their own due diligence.

From Your Site Articles

- Why Invest in Zinc? ›

- Top 10 Countries for Zinc Production ›

- Zinc Stocks: 5 Biggest Canadian Companies in 2025 ›

- Top Zinc Producing Companies ›

- Understanding the Zinc Spot Price and Zinc Futures ›

Related Articles Around the Web

https://x.com/INN_Resource

https://www.linkedin.com/in/deanbelder

dbelder@investingnews.com

Featured Zinc Investing Stocks

Learn about our editorial policies.