The Conversation (0)

Aug. 24, 2022 01:55PM PST

GAS-photo / Shutterstock

The war in Ukraine was a major catalyst for oil and gas prices during the first half of the year.

Hampered supply out Russia drove the cost of natural gas in Europe significantly higher, while a resurgence in oil demand following COVID-19 shutdowns and shipment disruptions pushed the cost of West Texas Intermediate (WTI) and Brent crude to 11 year highs. Supply challenges kept values elevated through Q1.

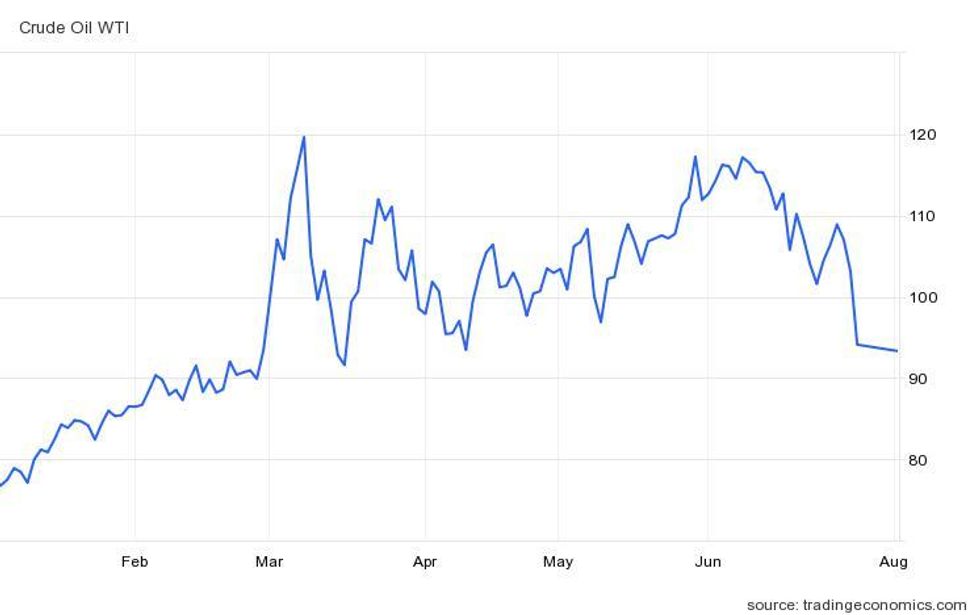

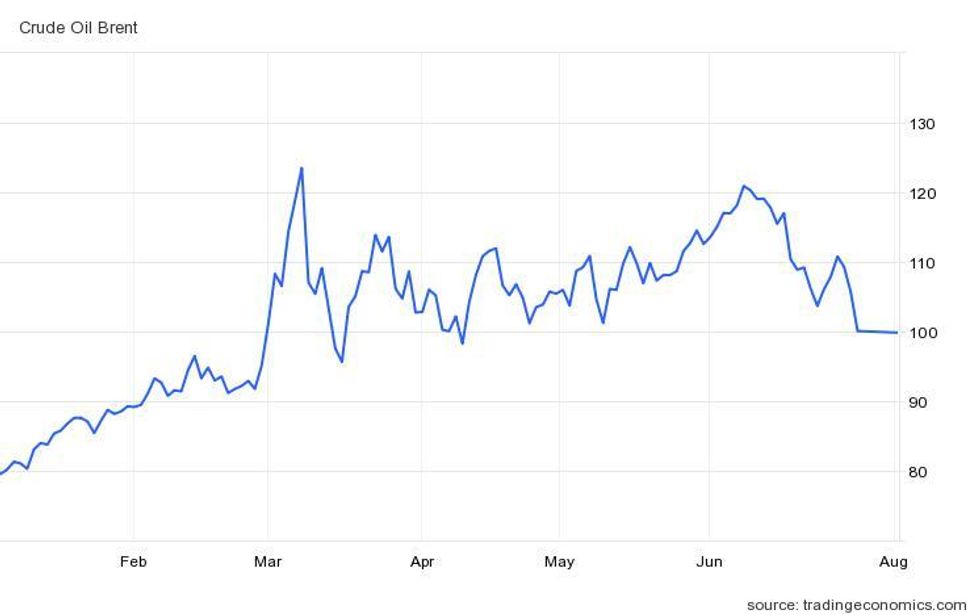

WTI crude started the year at US$75.88 a barrel, while Brent crude was selling for US$79.40. By the end of January, Brent crude had grown by US$10 to US$89.59; WTI crude followed suit, concluding the 31 day period at US$86.36.

“Easing concerns surrounding the impact of the Omicron variant on the global economic recovery supported prices for oil over the past month,” a January report from FocusEconomics reads.

“Against this backdrop of improved demand prospects, OPEC+ recently decided to stick to its current schedule for increasing output in February, further boosting prices in turn.”

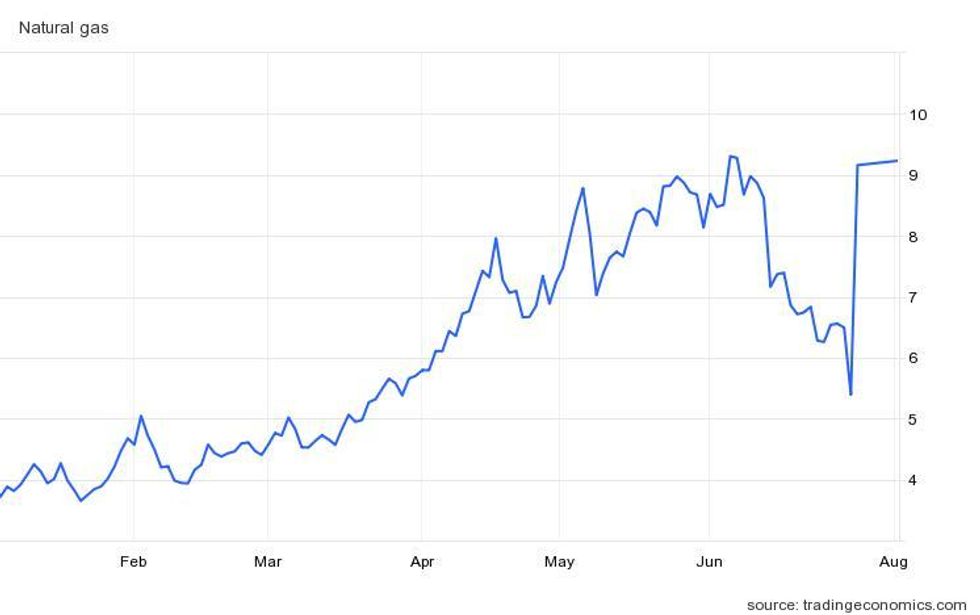

US natural gas prices also spent the first month of 2022 moving higher, starting the session at US$3.68 per million British thermal units (MMBtu) and ending it at US$4.60.

According to FocusEconomics panelists, after gas prices plummeted in November 2021 due to the rise in Omicron variant cases, values spent the first calendar month recovering.

“On January 14, the Henry Hub natural gas price was US$4.26 MMBtu, which was 12.4 percent higher than on the same day in the previous month,” the firm's January overview states. “Moreover, the price was up 14.2 percent on a year-to-date basis and was 60.2 percent higher than on the same day in 2021.”

Ahead of Russia’s invasion of the Ukraine, FocusEconomics outlined several factors that would impact the crude oil and natural gas sectors, including OPEC’s production rate, increased demand stemming from economic growth, extreme weather conditions, currency fluctuations, transportation costs and geopolitics.

The lattermost proved to be especially impactful in February and March.

Oil price update: War in Ukraine a major Q1 price catalyst

A steady ramp up in oil demand throughout early February supported both WTI and Brent crude before prices spiked above US$100 per barrel at the end of the month.

WTI crude's H1 price performance.

Chart via TradingEconomics.

The February 24 invasion of Ukraine immediately raised supply worries across the sector. Russia ranks third in annual oil production, outputting more than 10 million barrels per day — roughly 10 percent of global supply.

Brent crude's H1 price performance.

Chart via TradingEconomics.

Western sanctions against Russia drove commodities higher across the board, and both Brent (US$123.59) and WTI (US$120.10) crude soared to their highest values since 2008 on March 8.

“Markets were unnerved by potential supply disruptions, which could arise either through direct damage to pipelines or via the recent spate of tough Western sanctions and possible Russian retaliation, such as reducing oil and gas exports,” a March report published by FocusEconomics explains.

The US$120 range was unsustainable for the energy fuels, with both slipping back below US$100 by mid-March.

According FocusEconomics panelists, the realization that the “sanctions have been designed to avoid disruption to fuel supplies” somewhat relaxed global markets, but created a price discrepancy between WTI and Brent.

“Prices for WTI have risen less sharply than Brent amid recent forecasts of robust US crude production plus the US’s weaker dependence on Russian oil and gas,” the firm said. However, it pointed out that US inventories were still depleted, with export demand strong and global inventories on the low end.

By the end of the first quarter, WTI was up 37.86 percent from the start of the year, sitting at US$105.60, while Brent crude had increased 29.13 percent to hit US$103.16 over the same period.

Gas price update: Q1 brings questions over Russian supply

Over the first three months of the year, natural gas prices also made large gains, adding 55.41 percent by the end of March. They started 2022 at US$3.70 and had climbed to US$5.75 by the end of the quarter.

Tight US supply due to low inventories was further heightened by concerns over the future of Russian exports.

Almost half of Europe’s natural gas comes from Russia, with the majority flowing through the Nord Stream 1 and 2 pipelines. Potential pipeline shutdowns quickly became a prominent topic following the invasion of Ukraine.

Natural gas' H1 price performance.

Chart via TradingEconomics.

According to the International Monetary Fund (IMF), disruptions to Russian gas supply would weigh heavily on energy security and on the GDP of several European countries.

“In the most-affected countries in Central and Eastern Europe — Hungary, the Slovak Republic and the Czech Republic — there is a risk of shortages of as much as 40 percent of gas consumption and of gross domestic product (GDP) shrinking by up to 6 percent,” the IMF's mid-2022 report explains.

Oil price update: Energy security comes into focus in Q2

Crude oil prices remained locked between US$95 and US$110 from March through May before another rally set in. Continued sanctions and fears around Russian supply sustained 10 year highs, while mounting anxiety about geopolitics in other oil-producing countries further eroded global energy security.

“The oil market has twisted and turned in response to some seemingly jaw-dropping news in recent weeks,” FocusEconomic states in a May market report. “At the end of May, the European Union slapped a ban on most Russian oil and agreed, along with the UK, to bar the insurance of ships carrying Russian oil. Only a few days later, OPEC+ agreed to accelerate oil production.”

Despite these developments working to “cancel each other out,” the growing worldwide energy crisis propelled prices to a Q2 high as WTI touched US$117.51 and Brent reached US$120.74 on June 8.

Fueled by uncertainty around supply from Russia and OPEC’s inability to reach previously set targets, many market analysts acknowledged both the precarious energy situation and the problems with forecasting.

“Rarely has the outlook for oil markets been more uncertain. A worsening macroeconomic outlook and fears of recession are weighing on market sentiment, while there are ongoing risks on the supply side,” reads an oil market report released by the International Energy Agency in July.

The six months of high energy prices seen in H1, paired with inflation and pandemic recovery, are all expected to weigh heavily on global GDP this year, according to the World Bank and IMF. The organizations are anticipating that GDP will contract from its 2021 level of 5.9 percent to roughly 2.9 percent.

Gas price update: Prices peak in Q2

As the effects of sanctions began to take hold in April, natural gas prices began a more pronounced upward trend. By May 5, values had reached a 14 year high of US$8.93, a more than 140 percent increase from January.

By June, contention over supply from both Nord Stream 1 and 2 hit a fever pitch, and prices hit a fresh 14 year intraday high US$9.35. The threshold was unsustainable, however, and values fell through the end of the month.

At the end of the quarter, prices had contracted to US$5.29, down 43 percent from H1's high point. However, natural gas values spiked higher in early July as supply over the winter began to take center stage in Europe.

Looking forward, the first energy crisis since the 1970s has invigorated the move towards cleaner, renewable energy. Still, natural gas demand is projected to increase over the next 10 years.

“Gas demand is projected to grow by 10 percent in the next decade in all scenarios,” McKinsey & Company notes in a report on global energy perspectives.

Currently, gas accounts for 23 percent of all energy demand, but that is expected to decline to 15 percent by 2050.

“After 2030, gas projections diverge across scenarios driven by increasing decarbonization pressure in buildings and industry. The demand for gas is projected to be more resilient than for other fossil fuels,” the overview states.

Oil price update: Increased production to tame values in H2

Since the end of June, WTI values have continued to consolidate below US$100, while Brent has hovered around that level, breaking through to US$106 before contracting again.

The price retraction for both classes falls in line with FocusEconomics' outlook from earlier in the year.

"A rebound in U.S. shale oil and global oil production will likely push the market into surplus this year, despite robust US and global demand,” it reads. “Much depends on the evolution of the Russia-Ukraine conflict, Western sanctions, possible Russian retaliation and the pandemic, while U.S. monetary policy and the prospect of a new Iranian nuclear deal poses key downside risks.”

As such, panelists polled by the group are calling for WTI to average US$79.06 during the fourth quarter.

For Brent, the outlook is a little more opaque, although panelists are also expecting prices to remain off their previously set highs this year.

“That said, they will remain elevated amid persistent geopolitical tensions, including between Russia and the West,” the Brent crude update notes. “Much rests on the supply side of the price equation.”

More production out of OPEC, a decline in inflation and rebounding economic activity are all factors that the group believes could serve as price movers in the months ahead.

“Our panelists continue to have diverging views on the price outlook,” FocusEconomics explains. “For Q4 2022, the maximum price forecast is US$100 per barrel, while the minimum is US$65 per barrel.”

Don't forget to follow us @INN_Resource for real-time updates!

Securities Disclosure: I, Georgia Williams, hold no direct investment interest in any company mentioned in this article.

Editorial Disclosure: The Investing News Network does not guarantee the accuracy or thoroughness of the information reported in the interviews it conducts. The opinions expressed in these interviews do not reflect the opinions of the Investing News Network and do not constitute investment advice. All readers are encouraged to perform their own due diligence.

From Your Site Articles

- Top 5 Oil and Gas Stocks on the TSX and TSXV in 2022 ›

- Oil Price and Inflation: What’s the Correlation? ›

- Oil and Gas Price Forecast: Top Trends That Will Affect Oil and Gas in 2023 ›

- Top 10 Oil-producing Countries (Updated 2022) ›

- How to Invest in Oil and Gas ›

Related Articles Around the Web

https://x.com/INN_Resource

https://www.linkedin.com/in/georgia-williams-15845447/

gwilliams@investingnews.com

Featured Oil and Gas Investing Stocks

Learn about our editorial policies.