The Conversation (0)

Yakov / Adobe Stock

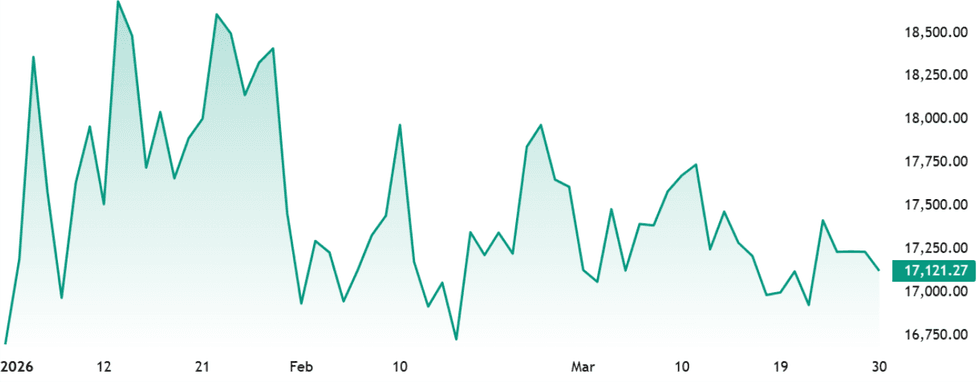

Nickel prices spiked at the end of 2025 and faced volatility in the first quarter of 2026.

The wave of strong upward momentum that began this past December has settled, leaving prices for the base metal trading within a wide range of US$17,000 to US$18,800 per metric ton (MT) in Q1.

Soft demand and elevated supply are threatening to send prices lower as the year continues.

However, there is some hope that the market could turn around as the world’s number one miner, Indonesia, rebalances its quota system, and as China embarks on a new five year plan.

What happened to the nickel price in Q1?

Nickel prices started the year with strength, riding a wave of momentum that started to build in mid-December, when they climbed from US$14,255 on December 16 to US$18,785 on January 14.

The first month of 2026 saw wide price swings, but the biggest came at the end of the month, when prices moved from US$18,520 on January 29 to bottom out at US$17,045 on February 2.

Nickel price, January 1 to March 31, 2026.

Chart via TradingView.

Since that time, nickel has breached the US$18,000 mark on two occasions — February 11 and 25. In between those dates, the metal reached a year-to-date low of US$16,830 on February 17.

Prices didn't fare much better in March. Nickel started the month closer to its low point than to January’s high, and while it’s slipped below US$17,000, it’s failed to break above US$18,000.

The metal was trading at US$17,390 as of March 25.

Will Indonesian supply cuts boost nickel prices?

When it comes to supply, simply put, there's too much nickel.

The market has been hit by a flood of Indonesian nickel over the past few years, and while there have been calls to rebalance the sector, shifts in the country's quota system have only stabilized prices, not increased them.

The biggest change in those circumstances came toward the end of 2025, when Indonesia announced that it would reduce mining quota validity from three years to one year.

In an email to the Investing News Network at the end of the year, ING commodities strategist Ewa Manthy suggested that wasn’t likely to be enough to improve the market in a meaningful way.

“The global market is still forecast to remain in surplus — around 261,000 MT in 2026 — so further cuts would need to be significant to alter fundamentals,” she explained.

So far, her prediction appears to be playing out. While the Indonesian government made another round of cuts to output quotas, this time a more significant drop to between 260 million and 270 million MT, down from 364 million MT last year, the move hasn’t translated to a sustained price increase for nickel.

At this point it's unclear whether the supply quotas will remain as tight throughout the year.

In 2024, the quota was slashed in February to 240 million MT, but later raised to 270 million MT as a lack of domestic supply began to affect smelters, forcing them to increase imports.

The same thing could happen again. Eramet (EPA:ERA,OTCPL:ERMAF) has already stated that it will apply for a revised quota at its Weda Bay operation after it was cut to 12 million MT from 32 million MT in 2025.

Elsewhere, metal inventories in Shanghai Futures Exchange warehouses have declined this year, falling from 106,473 MT at the end of December 2025 to around 87,538 MT on March 20.

Meanwhile, London Metal Exchange inventories have moved in the opposite direction, rising from 255,282 MT at the end of December to 282,792 MT as of March 20.

Nickel demand remains soft

On the demand side, one of nickel's main uses is in the production of stainless steel.

Much of this is destined for the construction industry, which is facing headwinds from a number of sources.

Notably, the Chinese construction sector, which traditionally has been a significant driver of stainless steel, is facing ongoing uncertainty. While demand from manufacturing is expected to increase, experts see that usage being offset by a real estate sector that has been under pressure since 2020. Although the Chinese government has tried to stimulate the market, new home sales are expected to decline again in 2026. Overall, S&P Global is predicting that Chinese steel demand will shrink in 2026 to 837 million MT, a drop from 860 million MT last year.

Likewise, demand for nickel destined for batteries is slowing down.

Chinese electric vehicle (EV) makers have been moving away from nickel-based batteries to lead-based batteries, which accounted for two-thirds of Chinese EV sales in 2025. Advancing technology has made these batteries more viable in recent years, overcoming energy density and range issues.

Additionally, because the inputs are cheaper, they’re more attractive to battery and EV producers and consumers alike.

Although Chinese EV sales reached a record 12.9 million units in 2025, North American sales were dampened, shrinking 4 percent to 1.8 million. Of the roughly 20 million pure EVs sold in 2025, Chinese auto maker BYD (OTCPL:BYDDF), which primarily uses a lithium-iron-phosphate blade battery in its cars, accounted for just over 10 percent of total sales.

These results allowed BYD to snag the top producer spot from US-based Tesla (NASDAQ:TSLA), which uses a nickel-manganese-cobalt chemistry in its batteries.

US-Iran war creating bottlenecks

Another potential headwind for nickel is the war between the US and Iran.

Since aggressions have ratcheted up, so too have oil prices. Although they came down somewhat during the week of March 23, they’re still significantly higher than they were at the same time last year.

The concern is that a protracted war could lead to long-term supply disruptions. Already, several Asian nations have seen energy shortages since the outbreak of hostilities.

The conflict also causing ripples in commodities markets. There have been significant outflows from metals exchange-traded funds into oil, and some producers have temporarily shut down operations.

Many mines depend on energy that comes from the Middle East, and any long-term impact on that supply could have significant consequences for their work.

When it comes to nickel specifically, operators depend on sulfur products used in high-pressure acid leach operations, which largely dominate battery-grade nickel production in Indonesia.

Much sulfur supply flows through the Strait of Hormuz from Saudi Arabia, Qatar and the United Arab Emirates. The strait's closure is not only affecting shipments from the region, but is more broadly impacting the shipping industry in general, which has had floating inventories taken off the board.

Nickel price forecast for 2026

Apart from the outbreak of war, not much has materially changed for nickel investors since the start of the year. Prices have come down a little, but are trading higher than last year at this time.

The oversupply situation has persisted through the start of the year, and it may not be until later in 2026 or into 2027 that the market begins to see a shift. BMI, a Fitch Solutions company, has a 2026 nickel price call of US$15,800, while Goldman Sachs (NYSE:GS) is more bullish, anticipating an average of US$17,200 this year.

Of course, there are events that could throw those predictions to the wind — most notably, the war in the Middle East. Its overall effect will depend on how long the conflict lasts.

Don’t forget to follow us @INN_Resource for real-time news updates!

Securities Disclosure: I, Dean Belder, hold no direct investment interest in any company mentioned in this article.

Editorial Disclosure: The Investing News Network does not guarantee the accuracy or thoroughness of the information reported in the interviews it conducts. The opinions expressed in these interviews do not reflect the opinions of the Investing News Network and do not constitute investment advice. All readers are encouraged to perform their own due diligence.

NASDAQ:F

https://twitter.com/INN_Resource

https://www.linkedin.com/in/deanbelder

dbelder@investingnews.com