The Conversation (0)

Click here to read the latest copper trends article.

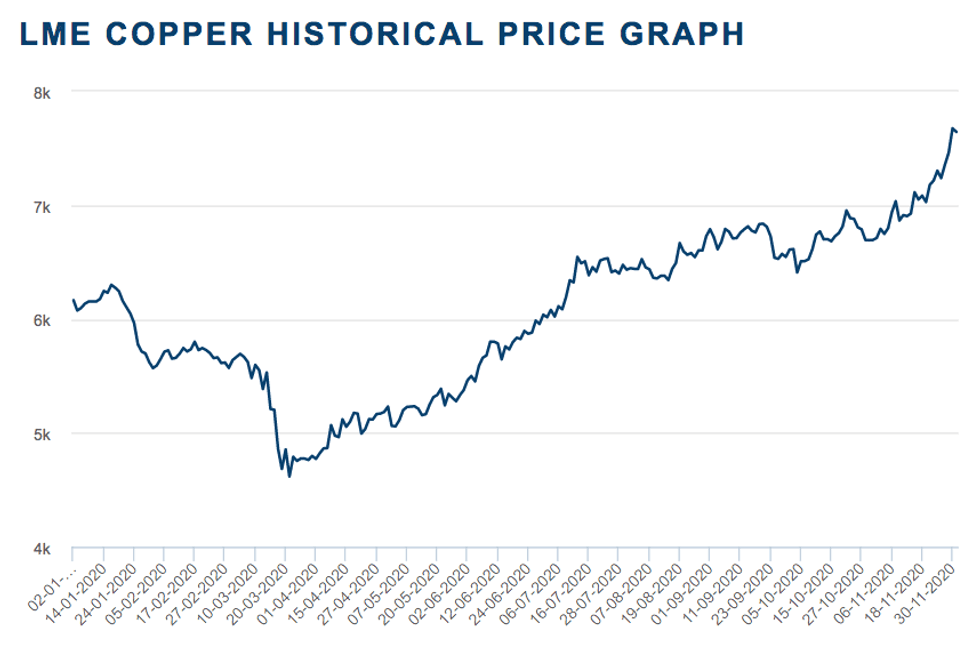

In 2020, the COVID-19 pandemic hit markets across the board, with copper being no exception.

Lockdown and containment measures hurt supply and demand for the red metal in Q1, but a sharp recovery began in Q2, with copper testing the US$7,000 per tonne level by the end of the year.

With 2020 rapidly drawing to a close, here the Investing News Network (INN) takes a look at what the trends for copper were in each quarter, how prices performed throughout the year and what analysts said about developments quarter by quarter. Read on to learn more.

Copper trends Q1: COVID-19 hits the world

Uncertainty reigned during the first quarter of the year, with base metals prices hitting multi-year lows on the back of the potential impact of the coronavirus outbreak on the global economy.

The trend in copper prices was downward for most of Q1, with the red metal breaking several marks to the downside. Copper prices plummeted to their lowest point of 2020 on March 23 at US$4,617.50.

2020 copper price performance. Chart via the London Metal Exchange.

As China shut down its production lines and implemented virus containment measures, demand for infrastructure metals was hurt — but how much and to what extent remained to be seen.

Karen Norton of Refinitiv told INN at the time that Chinese copper demand was estimated to have fallen by a quarter in Q1, but the impact elsewhere was expected to be felt more keenly in Q2.

And of course, the coronavirus outbreak was not only a demand-side story — a supply response once the virus spread around the globe came fast as well.

Major copper powerhouses Peru and Chile imposed restrictions to contain COVID-19, and miners in those countries and elsewhere stepped up preventative measures, including halting production, suspending expansions and reviewing future plans.

Another major catalyst in Q1 was that the low copper price environment put further strain on mining companies, which were already experiencing pressure before the coronavirus pandemic.

“Production was already set to be constrained this year, so producers’ ability to (ramp up output as soon as the outbreak is controlled) is limited,” Norton said. “Significantly, some major miners are also delaying work on new projects, which will have the knock-on effect of restricting growth over a medium-term view where growth was already quite limited.”

Over the longer term, CRU Group is forecasting that production from existing copper mines will decline by 2024, and mine projects will be key to sustaining supply growth.

Copper prices started the quarter trading at US$6,165 to end the three month period at US$4,797.

Copper trends Q2: Supply and demand start recovery

After taking a hit in Q1, the second quarter of the year told a different story for the red metal, as fundamentals started to improve.

An improvement in copper demand in China, paired with stimulus packages and supply disruptions in top-producing countries, pushed prices higher.

For Kieran Clancy of Capital Economics, copper demand recovered quicker than many expected in Q2.

“This is almost entirely due to a remarkable bounce-back in Chinese demand, as policymakers there moved to stimulate activity — particularly in the copper-intensive infrastructure sector,” Clancy told INN at the time. “And with that support set to be stepped up in the months ahead, a further pick-up in Chinese demand will probably remain the key driver in the second half of the year.”

He added that a pick-up in demand ex-China would probably be an additional positive at the margin.

For Dan Smith of Commodity Market Analytics, the early phase of the recovery was clearly V-shaped. “But as we move into H2, growth will start to level off and many sectors will remain depressed compared to where we were in 2019.”

At that point, copper supply had been relatively resilient so far in 2020, which was somewhat unexpected, according to Clancy.

“Compared to other base metals, mined copper supply has held up reasonably well, thanks to a surge in Chinese output of copper ore,” Clancy said back in Q2. “However, with virus numbers in Latin America now climbing rapidly, we think there is significant risk to supply in Q3.”

Copper prices started the quarter trading at US$4,772 to end the three month period at US$6,038.

Copper trends Q3: Sharp recovery continues

The sharp copper rebound that started in Q2 continued through the third quarter, with upbeat Chinese demand and supply-side concerns boosting the red metal’s price to a two year high. Copper rallied well in Q3, in line with a widespread rise across the commodities complex, Smith told INN at the time.

“The rally was faster than we expected, although prices have not yet broken above key resistance around US$7,050, so this continues to represent a significant obstacle in the months ahead,” he said.

Norton of Refinitiv told INN that she was expecting to see fresh highs reached in Q3, but not on a sustained basis. “Several factors have converged to support prices, including ongoing supply worries, partially due to labor disputes, better-than-expected demand in top consumer China and US stimulus hopes,” she said back in Q3.

After supply worries due to coronavirus restrictions and lockdowns characterized Q1, the third quarter of the year brought new supply concerns on the back of labor disputes.

In Chile, the top-producing country, workers at Zaldivar, Collahuasi, Centinela, Candelaria and Escondida, the world’s largest copper mine, were in contract negotiations throughout the quarter.

Refinitiv’s base-case assumption was that any strikes would prove relatively short-lived and ultimately not have a substantial impact on production.

Speaking about concerns over potential supply disruptions in South America, Smith said it is quite rare for strike activity to make any meaningful difference in prices for anything more than a few weeks.

“More important for now is COVID-19, which is taking a significant toll on mine production in Chile and Peru,” he explained to INN.

Copper prices started the quarter trading at US$6,016.50 to end the three-month period at US$6,610.

Copper trends Q4: Prices test US$7,000 level

As the fourth quarter kicked off, all eyes were on the US and Europe as they continued to work on launching stimulus packages that could impact demand for metals.

“The US government is likely to unleash a new stimulus package soon, which will fuel a further surge of global liquidity into financial markets and copper,” Smith said. “The EU is also looking at stimulus via increased infrastructure spending to boost renewable energy and power grids for electric vehicles.”

The US elections also took place during Q4, with Democrat Joe Biden winning the presidency.

“If it materializes, a Biden victory would not necessarily have an immediate impact on trade, but relations would likely improve over the longer term,” Norton said before the election results.

“Copper would also likely get a fillip from the adoption of green energy policies that would benefit demand for the metal over the longer term.”

Gains for the red metal were limited as a second wave of COVID-19 infections hit many countries around the world, fueling fears of new containment measures that could hit demand for metals.

Prices surged to their highest level since 2018 following strong data from China, which pointed to solid demand for copper ahead.

Another catalyst for prices during the last three month period of 2020 was the expectation of approval and distribution for a COVID-19 vaccine, which turned investors bullish on the economic outlook.

Copper hit its highest point of the year so far on December 1, reaching a seven year high of US$7,674.50. Copper started the quarter trading at US$6,614 and on December 1 finished at US$7,644.

Don’t forget to follow us @INN_Resource for real-time news updates.

Securities Disclosure: I, Priscila Barrera, hold no direct investment interest in any company mentioned in this article.

Editorial Disclosure: The Investing News Network does not guarantee the accuracy or thoroughness of the information reported in the interviews it conducts. The opinions expressed in these interviews do not reflect the opinions of the Investing News Network and do not constitute investment advice. All readers are encouraged to perform their own due diligence.

https://www.linkedin.com/in/priscilabarrera/

pbarrera@investingnews.com