The Conversation (0)

GTI Energy Ltd (GTI or Company) advises that planning is finalised, with permitting & bonding close to completion, for 100,000 ft of drilling at its Great Divide Basin (GDB) Project in Wyoming.

Highlights:

Exploration Program Overview – Great Divide Basin (GDB)

DRILLING AT THOR

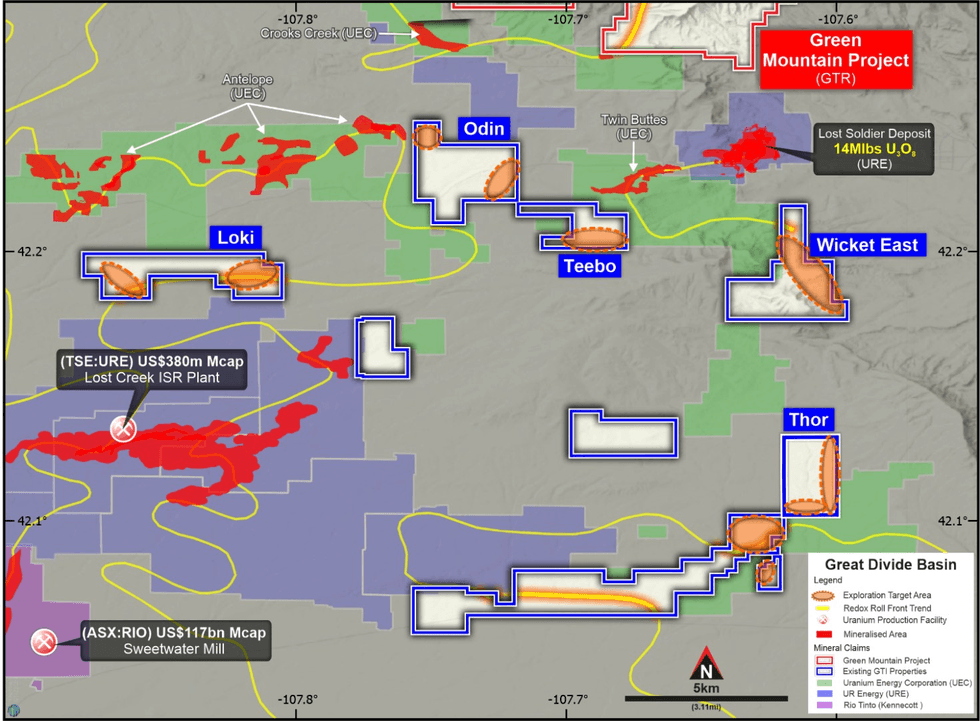

Thor is the most advanced of the GDB Project areas and is located adjacent to Ur-Energy Inc’s (URE) 18Mlb Lost Creek uranium deposit and operating ISR uranium processing plant2.

Exploration at Thor to date has successfully identified mineralisation with economic potential based on widths, grades & depth of mineralisation (ASX release 29 March 2022)1.

The upcoming program at Thor is now planned, permitted & bonded to include follow-up drilling of up to 70 new holes (~40,000 ft) to target extensions of the 2 miles of mineralised roll front identified from drilling completed earlier this year.

The new drilling will focus on the north-eastern section of the project including the two Wyoming state leases located northeast of the lode claim block which GTI previously successfully explored (Figure 1).

DRILLING AT WICKET EAST

The Wicket East claims abut the southern boundary of Ur-Energy’s Lost Soldier Deposit (Figure 1).

Drilling of up to 20 holes (~20,000ft) at Wicket East seeks to explore a projected mineralised trend extending from the southern boundary of URE’s Lost Soldier property for ~3 miles, as defined by historic drilling information similar in nature to that used to plan the successful maiden drilling program at Thor.

DRILLING AT ODIN, LOKI & TEEBO

Odin & Teebo are located adjacent to Uranium Energy Corp’s (UEC), former Uranium One, Antelope Project. The Loki claims sit south of UEC’s Antelope & north of URE’s Lost Creek.

Drilling of ~40 holes (~40,000 ft) collectively across Odin, Teebo & Loki also seeks to explore mineralised trends, over a combined length of ~5 miles, as defined by the historic drilling information previously used to plan successful maiden drilling at Thor.

FIGURE 1. GDB WYOMING ISR URANIUM PROJECTS. PLANNED EXPLORATION DRILLING AREAS

FIGURE 1. GDB WYOMING ISR URANIUM PROJECTS. PLANNED EXPLORATION DRILLING AREAS

Executive Director Bruce Lane said “preparation for our follow-up drilling campaign in the Great Divide Basin is now at an advanced stage. We have sequenced the drilling to deliver the full 100,000 ft program prior to Christmas as originally planned. We are confident that we can successfully execute the drilling this year which will set GTI up to produce a uranium resource report in 2023. We look forward to providing updates in the coming weeks as the program progresses”.

Click here for the full ASX Release

This article includes content from GTI Energy Ltd, licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.