The Conversation (0)

Click here to read the latest platinum outlook.

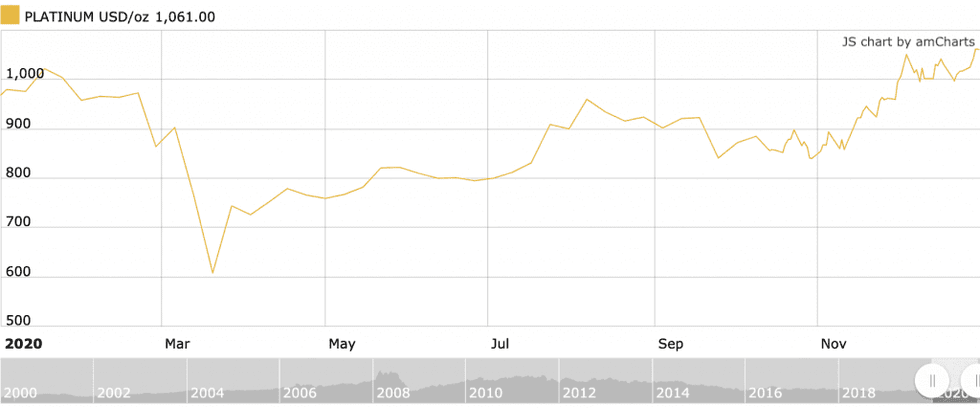

Platinum prices endured a rollercoaster ride in 2020, hitting a two year high in January before plummeting to a 17 year low in March.

Although the rest of the precious metals suite recovered quickly from the slump, platinum wasn’t able to regain its early year momentum until the second half of 2020. By the end of December, the metal had surpassed its previous 2020 high to add 8.3 percent to its value for the year.

That number jumps to 74 percent when calculating platinum’s recovery from its March low of US$608 per ounce. Much of the rebound was facilitated by a significant uptick in investment demand.

“Investment demand surged by 291 percent year-on-year in the third quarter,” notes a World Platinum Investment Council (WPIC) report from November 2020.

“(Exchange-traded fund) ETF demand in the quarter rose to 543,000 ounces (koz), while strong bar and coin demand continued, rising to 96 koz.”

2020 saw platinum ETF inflows reach record-setting levels, surpassing 3.8 million ounces. The growth in investor demand contributed to the metal’s overall deficit in 2020.

“Investor interest and positioning increased further based on the positive developments in 2020,” the overview from the WPIC states.

“These included the stronger than expected V-shaped recoveries in automotive markets, sustained pandemic-related risk driving precious metal investment demand and severely reduced supply, that all contributed to the record -1,202 koz deficit forecast for 2020.”

The platinum-group metals (PGMs) space was hit hard in March, as both platinum and palladium shed 40 percent almost overnight.

2020 platinum price performance. Chart via Kitco.

“The drop in prices in late February and early March was predominantly driven by a stark fall in demand from the automotive sector,” Steven Burke of FocusEconomics told the Investing News Network.

Burke went on to note that lockdown measures weighed on the global economic outlook, which in turn suppressed vehicle demand.

“That said, restrictions on South Africa’s mining sector to control the spread of the virus dragged heavily on supply, which, coupled with safe haven demand, helped prices to recover quickly in Q2,” said Burke. “In H2 2020, the ongoing rise in prices was mainly driven by recovering global economic activity — particularly out of China as car sales in the country were healthy.”

Platinum trends 2020: Supply challenges propel prices

Unsurprisingly, widespread COVID-19 lockdowns in South Africa greatly impacted platinum output in the top-producing country. That was further compounded by production challenges at Anglo American Platinum’s (Amplats) (LSE:AAL,OTC Pink:AGPPF) converter plant.

In early March, the mining major announced it would be unable to meet its previous guidance due to a force majeure at its South African operations. A fire and structural issues forced Amplats to take both the Phase A and B sections of its Anglo Conversion Plant offline.

The closure of both the A and B plant in March weighed heavily on Amplats’ production, as US Global Investors’ (NASDAQ:GROW) Ralph Aldis pointed out.

“(Amplats) curtailed guidance down to about 2.5 million ounces from (roughly) 3.1 million to 3.3 million,” he said. “That’s almost 600,000 ounces less production. It should tighten the market.”

The PGMs miner was able to resume operations in Q4, with a ramp up at the end of the year.

“The Anglo issue has had an impact and was one of the reasons for the run up in PGMs prices late last year, but with supply being restored, barring any renewed disruptions that impact will fade,” said Rohit Savant, vice president of research at CPM Group.

Although Amplats and South Africa have resumed mining activity, global refined platinum production is expected to slip 22 percent year-over-year, largely off the South Africa closures.

According to the WPIC, “The country’s output is expected to decline 30 percent (-1,302 koz) as a result of a processing infrastructure failure and COVID-19.”

Platinum trends 2020: Depressed automotive demand

The largest end-use segment for platinum is the automotive industry, a sector that was significantly impeded by COVID-19 restrictions, keeping buyers out of show rooms and production lines muted.

As noted in a S&P Global report, auto sector sales are anticipated to fall 20 percent globally for 2020. Depressed sales are set to continue into 2022, with an average decline of 6 percent from 2019 tallies.

“We continue to believe that the Chinese market has the potential to resume moderate long-term growth, and project it will be the only region to recover to 2019 volumes by the end of 2022,” reads the firm’s overview. “In Europe and North America, sales showed signs of stabilizing in July and August, but we don’t expect these markets to fully recover their steep declines within the next two years.”

Reduced demand from the car segment was countered by the fall in output, but an increase in pollution control measures, especially in China, will likely continue to add to an overall platinum deficit.

With the South African lockdown stretching two months, platinum prices began to spike at the end of June. The metal added 31 percent to its value, rising from US$608 on March 20 to US$800 on July 3.

Platinum prices climbed an additional 32 percent from July to the end of December to reach US$1,062.

“Platinum relies more heavily on South Africa for its primary supply,” said Savant, explaining why platinum outperformed palladium during H1 2020.

“Additionally, a sharp recovery in Chinese commercial vehicle demand during 2020 further helped support platinum prices,” he said. “The uptick in Chinese commercial vehicle demand had an impact on both metals’ prices, (but) the impact was greater on platinum than on palladium in large part due to the disruption to South African mine supply.”

Platinum outlook 2021: What to expect?

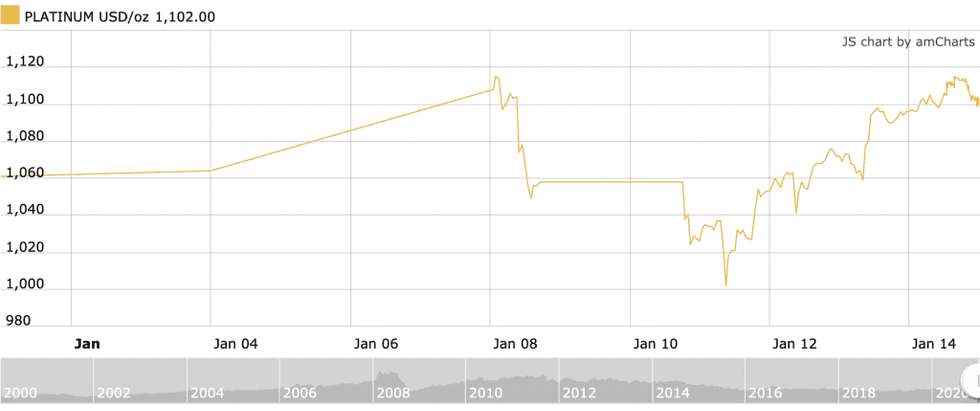

After trending higher from the end of October to early January 2021, reaching a four year high, platinum briefly pulled back, dipping to US$1,018 on January 11. Prices have since rebounded and are holding near the US$1,100 threshold.

2021 platinum price performance. Chart via Kitco.

“A key factor that is expected to help both platinum and palladium is the ample liquidity as a result of accommodative monetary and fiscal policy amid improving economic conditions,” said CPM Group’s Savant. “Being industrial precious metals they should benefit from this environment.”

The fundamentals for both metals are promising, but platinum does seem to be poised to perform slightly better. “While both metals are expected to rise during the year, platinum is expected to outperform palladium,” he added. “Platinum’s price performance is expected to lag only that of silver among the exchange-traded precious metals.”

The WPIC foresees a recovery in total supply, with an estimated 17 percent year-over-year uptick.

“Mine supply is expected to sharply rebound 20 percent (+976 koz) year-on-year to 5,772 koz following the extreme disruption of 2020,” the WPIC reported.

The platinum-focused firm sees growth in the automotive, jewelry and industrial segments slowly returning to pre-pandemic levels and benefiting the demand side.

“However, as investment demand is not expected to repeat the record in 2020 it will decline,” it explains. “Total platinum demand in 2021 is therefore expected to increase 2 percent (+150 koz) to 8,089 koz.”

For Aldis, a potential catalyst for the metal will be the emergence and growth of the hydrogen fuel cell space. He referenced a November Bank of America Merrill Lynch (NYSE:BAC) report.

“They were highlighting that platinum is going to have a future in the post-internal combustion engine’s demise, because the fuel cells use platinum as a catalyst to speed the hydrogen and oxygen reaction that releases the energy and produces the water,” said Aldis.

Another demand catalyst for prices could be the continued substitution of palladium with platinum in catalytic convertors, as well as increased sales in gasoline-powered vehicles over diesel.

“Platinum prices are at a discount to palladium, and even relative to its own price level, platinum prices are at multi-year lows despite the sharp gains in recent months,” said Savant.

“This relative undervalued status of platinum coupled with improving medium- to long-term fundamentals for the metal are expected to help platinum perform strongly during 2021.”

Don’t forget to follow us @INN_Resource for real-time updates!

Securities Disclosure: I, Georgia Williams, hold no direct investment interest in any company mentioned in this article.

Editorial Disclosure: The Investing News Network does not guarantee the accuracy or thoroughness of the information reported in the interviews it conducts. The opinions expressed in these interviews do not reflect the opinions of the Investing News Network and do not constitute investment advice. All readers are encouraged to perform their own due diligence.

https://x.com/INN_Resource

https://www.linkedin.com/in/georgia-williams-15845447/

gwilliams@investingnews.com

Featured Platinum Investing Stocks

Learn about our editorial policies.