The Conversation (0)

Telson Mining Corporation (“Telson” or the “Company”) (TSX Venture – TSN.V) is pleased to announce the positive result of an independent Preliminary Economic Assessment study (“PEA”) prepared in accordance with National Instrument 43-101 (“NI 43-101”) on the 100% owned Campo Morado Mine (“Campo Morado” or the “Project”) located in Guerrero State, Mexico.

Telson Mining Corporation (“Telson” or the “Company”) (TSXV:TSN) is pleased to announce the positive result of an independent Preliminary Economic Assessment study (“PEA”) prepared in accordance with National Instrument 43-101 (“NI 43-101”) on the 100% owned Campo Morado Mine (“Campo Morado” or the “Project”) located in Guerrero State, Mexico.

Campo Morado PEA Highlights1:

- Pre-tax Net Present Value (“NPV”) at a 8% discount rate of US$81Mn- After-tax NPV at a discount rate of 8% of US$65Mn

- Undiscounted cash flow before income and mining taxes of US$114Mn

- Undiscounted cash flow after income and mining taxes of US$91Mn

- Life of mine (“LOM”) of 12 years, with 9.7 million tonnes of potential mill feed at an average grade of 4.33% zinc grade, 1.00% Lead grade, 0.78% copper grade, 131.9 grams per tonne (“g/t”) of silver and 1.71 grams per tonne (“g/t”) of gold

- Mining rate of 2,500 tonnes per day (“tpd”)

Jose Antonio Berlanga, Director and CEO, stated: “The positive Preliminary Economic Assessment marks another significant milestone for Telson. It validates the positive economic value of last year’s acquisition of the Campo Morado mine. We expect to improve the Net Present Value of the mine in the short run by implementing several strategies summarized below and we will embark on a Pre-Feasibility Study designed to demonstrate the improvements in mining and milling that we are instituting. The PEA is based on historical operating costs incurred by the previous operator of the Campo Morado mine as Telson is still in the pre-production stage and it is too early to forecast any cost savings resulting from the changes we have implemented. Among the strategies we have identified as drivers of increasing the NPV are:

1. Cost reductions resulting from: i) a reduced local workforce. We are currently operating the mine and approaching similar output as the former operator with approximately 50% of the previous workforce. It should be noted that the former owner was focused only on zinc production and was mining three separate mineralized bodies at the same time which required additional personnel, services, equipment and infrastructure. We are focused on all metals and only mining one mineralized body at a time, such that we can operate with a smaller workforce; ii) a change from room and pillar mining to sub-level caving (see s. 16.3 of the PEA); and iii) a reduction in haulage distance as a result of new egress portal being developed;

2. conducting an aggressive exploration campaign designed to increase the mineral resources at Campo Morado;

3. analyzing leaching processes to increase recoveries of precious metals from concentrate and existing tailings.

While we look forward to optimizing the performance of the Campo Morado mine, we also wish to emphasize that our primary goal for 2018 is to build our new mine at our flagship Tahuehueto project in Durango, Mexico. We point out that we published a NI 43-101 Technical Report Preliminary Feasibility Study Telson Resources Project Durango, Mexico with an effective date of December 6, 2016 and a report date of January 20, 2017 (see Tahuehueto PFS). based on a 550tpd operation at Tahuehueto that assigned a pre-tax Net Present Value, using an 8% discount, of US$138Mn and a post-tax Net Present Value using an 8% discount, of US$77Mn to Tahuehueto, such that the base case scenario NPV of both projects of the Company, Tahuehueto and Campo Morado, adds to US$218Mn on a pre-tax basis and US$142Mn on a post-tax basis. We are building a mill capable of processing 1,000 tpd at Tahuehueto and are also working on an updated PFS to reflect the improved economics of such an operation. We believe this will validate the upside potential of the economics of the Company for our shareholders and look forward to a very exciting year ahead of us.”

Description of Campo Morado Mine and PEA

The Campo Morado Project hosts several polymetallic massive sulphide deposits containing zinc, copper, silver, gold and lead mineralization. Five deposits have been extensively drilled: G9, El Largo, Reforma, Naranjo and El Rey. The Project is comprised of a previously mined underground multi-metal mine with infrastructure, installations and equipment capable of processing 2,500 tonnes of material per day. Farallon Resources Ltd. (Farallon) began mining operations at the G9 Mine at Campo Morado in April 2009. Nyrstar NV (Nyrstar) purchased Farallon and the Campo Morado Mine in December 2010 and continued mining operations at G9 mine with some production from the El Largo deposit until production was suspended in January 2015 and the mine was placed on care and maintenance.

Telson Mining Corporation purchased the Campo Morado Mine from Nyrstar Mining Ltd. and Nyrstar Mexico Resources Corp. (together the “Nyrstar Group”) in June 2017 and restarted mining operations under a preproduction plan and initiated production of zinc concentrates in October 2017. Telson intends to advance preproduction towards full commercial production during 2018. The purchase price of the Nyrstar Group subsidiaries that own the Campo Morado Mine was US$20Mn of which US$3.5Mn has been paid and the balance of US$16.5Mn is due to be paid on or before June 13, 2018.

Mineral Resource Estimate

The current Campo Morado resources occur in five main mineralized zones, G9, El Largo, Naranjo, Reforma and El Rey. Within these main zones, 36 sub-zones of well defined, massive and semi-massive sulphide deposits modeled three dimensionally are used to constrain the resources. The boundaries of these sub-zones are delineated by geological and assay data from extensive drilling and underground excavation. The resource estimate is based on 1,541 surface and underground drill holes and the 33,523 assays obtained from them that intersect and occur within these mineralized zone models. The mined-out volumes of the underground excavations of previous mining operations in turn deplete the resources. Two contiguous 5-metre cube block models were used to cover this area. The overall combined resource of the five zones estimated by ordinary kriging is presented below. The tabulation is based on zinc equivalency (ZnEq) 2 that incorporates the contributions of zinc, copper, gold, silver and lead and metal recovery factors achieved at the processing facility on site. The base case at a 5.5% ZnEq cut-off is highlighted in bold typeface. The effective date for the mineral resource estimates3 for the five individual main mineralized zones is September 30, 2017.

Campo Morado Resource Estimate 2017

| Cut-off ZnEq (%) | ZnEq (%) | Tonnes | Au (g/t) | Ag (g/t) | Cu (%) | Pb % | Zn (%) |

| Measured | |||||||

| 3.0 | 6.94 | 17,004,000 | 1.34 | 91 | 0.73 | 0.67 | 3.17 |

| 4.0 | 7.87 | 13,412,000 | 1.49 | 104 | 0.76 | 0.78 | 3.71 |

| 5.5 | 9.27 | 9,292,000 | 1.70 | 124 | 0.82 | 0.94 | 4.56 |

| 7.0 | 10.71 | 6,318,000 | 1.88 | 143 | 0.87 | 1.11 | 5.44 |

| Indicated | |||||||

| 3.0 | 5.78 | 16,848,000 | 1.25 | 85 | 0.68 | 0.61 | 2.25 |

| 4.0 | 6.62 | 12,324,000 | 1.42 | 99 | 0.72 | 0.73 | 2.68 |

| 5.5 | 7.94 | 7,335,000 | 1.70 | 123 | 0.78 | 0.92 | 3.31 |

| 7.0 | 9.32 | 4,086,000 | 1.96 | 151 | 0.86 | 1.12 | 3.94 |

| Measured + Indicated | |||||||

| 3.0 | 6.36 | 33,852,000 | 1.29 | 88 | 0.70 | 0.64 | 2.71 |

| 4.0 | 7.27 | 25,736,000 | 1.46 | 102 | 0.74 | 0.76 | 3.22 |

| 5.5 | 8.68 | 16,627,000 | 1.70 | 123 | 0.80 | 0.93 | 4.01 |

| 7.0 | 10.16 | 10,404,000 | 1.91 | 146 | 0.87 | 1.11 | 4.85 |

| Inferred | |||||||

| 3.0 | 5.03 | 3,316,000 | 0.98 | 76 | 0.52 | 0.58 | 2.10 |

| 4.0 | 5.85 | 2,152,000 | 1.11 | 90 | 0.55 | 0.71 | 2.54 |

| 5.5 | 7.27 | 988,000 | 1.32 | 116 | 0.64 | 0.92 | 3.20 |

| 7.0 | 8.75 | 416,000 | 1.52 | 148 | 0.76 | 1.10 | 3.78 |

2 Zinc equivalent calculations used metal prices of USD 1.20/lb for zinc, USD 2.80/lb for copper, USD 17/oz for silver, USD 1150/oz for gold and USD 0.90/lb for lead and metallurgical recoveries of 70% for zinc, 68% for copper, 38% for silver, 25% for gold, and 60% for lead. The zinc equivalency calculation is as follows:

ZnEq General Equation = Zn% + ((Cu % *(Cu recovery / Zn recovery) * ((Cu $ per %) / Zn $ per %)) + ((Ag g/t * (Ag recovery / Zn recovery) * (Ag $ per gram / Zn $ per %)) + ((Au g/t * (Au recovery / Zn recovery) * (Au $ per gram / Zn $ per %)) + ((Pb % *(Pb recovery / Zn recovery) * ((Pb $ per %) / Zn $ per %))

ZnEq = Zn% + ((Cu % *(68/70) * (61.73/26.455)) + ((Ag g/t * (38/70) * (0.547/26.455)) + ((Au g/t * (25/70) * (36.97/26.455)) + ((Pb % *(60/70) * ((19.84/26.455))

Where:

| Au price = $1150/oz | Au metal recovery = 25% |

| Ag price = $17/oz | Ag metal recovery = 38% |

| Cu price = $2.80/lb | Cu metal recovery = 68% |

| Pb price = $0.90/lb | Pb metal recovery = 60% |

| Zn price = $1.20/lb | Zn metal recovery = 70% |

3 Capping to reduce statistically anomalous high values was applied to the updated mineral estimate. All mineral resource estimates, cut-offs and metallurgical recoveries are subject to change as a consequence of more detailed economic analyses that would be required in pre-feasibility and feasibility studies.

Capital and Operating Cost Estimates

The Project is a previously operating mine that is being brought back into production. Consequently, this PEA treats the initial capital investment as a sunk cost, and all subsequent investment is considered as sustaining capital expenditure.

Over the LOM period, sustaining capital is provided for as shown in table below.

Sustaining Capital estimate for the Campo Morado Mine

| Sustaining Capital | LOM TOTAL (USD’000) |

| Development | 25,500 |

| Mill/Concentrator | 12,000 |

| Tailings Storage | 10,000 |

| Infrastructure (Other) | 10,000 |

| Social Responsibilities | 12,000 |

| Rehabilitation & Closure Costs | 3,200 |

| Total | 72,700 |

Operating cost estimates for the Project are forecast on the basis of previous operators operating experience at the Project, modified where appropriate to reflect increased throughput and proposed changes in the underground mining method.

Over the LOM period, operating costs are forecast as shown in table below.

Operating cost estimate for the Campo Morado Mine

| Project Operating Costs | LOM Average USD/t milled | LOM TOTAL USD’000 |

| Selling Costs | 23.52 | 228,997 |

| Royalties | 2.97 | 28,896 |

| Mining | 32.78 | 319,190 |

| Processing | 24.72 | 240,745 |

| G&A | 14.76 | 143,744 |

| TOTAL Operating Costs | 98.74 | 961,571 |

The LOM capital and operating costs as discussed in the PEA will most likely be further refined as Telson continues to bring the Campo Morado Project back into production and continues to optimize the various costs at site.

Economic Analysis

Micon has prepared its assessment of the project based on a discounted cash flow model, from which Net Present Value (NPV) can be determined. A real discount rate of 8.0% is applied to the base case cash flow.

The prices used in the cash flow projection are rolling average prices for each metal for the 12 months ended January 2018, which Micon believes provide a reasonable estimate of project revenues for this PEA. The prices used are shown in table below.

Metal Price Forecast

| Metal | Unit | Price (USD/unit) | Unit | Price (USD/unit) |

| Zinc | tonne | 2,954.70 | pound | 1.340 |

| Lead | tonne | 2,346.40 | pound | 1.064 |

| Copper | tonne | 6,274.20 | pound | 2.846 |

| Silver | troy ounce | 17.08 | ||

| Gold | troy ounce | 1,269.00 |

Since the project has already been constructed, initial capital costs are treated as sunk. However, LOM sustaining capital is estimated at USD 72.7Mn, mainly for underground development and expansion of tailings storage capacity.

Total cash costs over the LOM period average USD 98.74/t milled. Costs incurred in Mexican pesos (MXN) have been converted at the rate of MXN 18.75/USD.

Pursuant to the share purchase agreement dated April 27, 2017 (the “Agreement”) between Telson and the Nyrstar Group, Nyrstar retains the right to receive a variable purchase price royalty (the “Zinc Royalty”) on future zinc production on the first 10 million tons of ore processed by Telson when the price of zinc is at or above US$2,100 per tonne (see Telson news release dated June 14, 2107 for further details). Telson maintains the right under the Agreement to purchase 100% of the Zinc Royalty at any time for US$4Mn. Buy-out of the Zinc Royalty to Nyrstar is assumed to take place prior to the cash flow period and is treated as a sunk cost. A 3% royalty payable to SGM on the NSR value of concentrate sales (before transport costs) has been provided for in the cash flow model.

This PEA is preliminary in nature; it includes inferred mineral resources that are considered too speculative geologically to have the economic considerations applied to them that would enable them to be categorized as mineral reserves, and there is no certainty that the PEA will be realized.

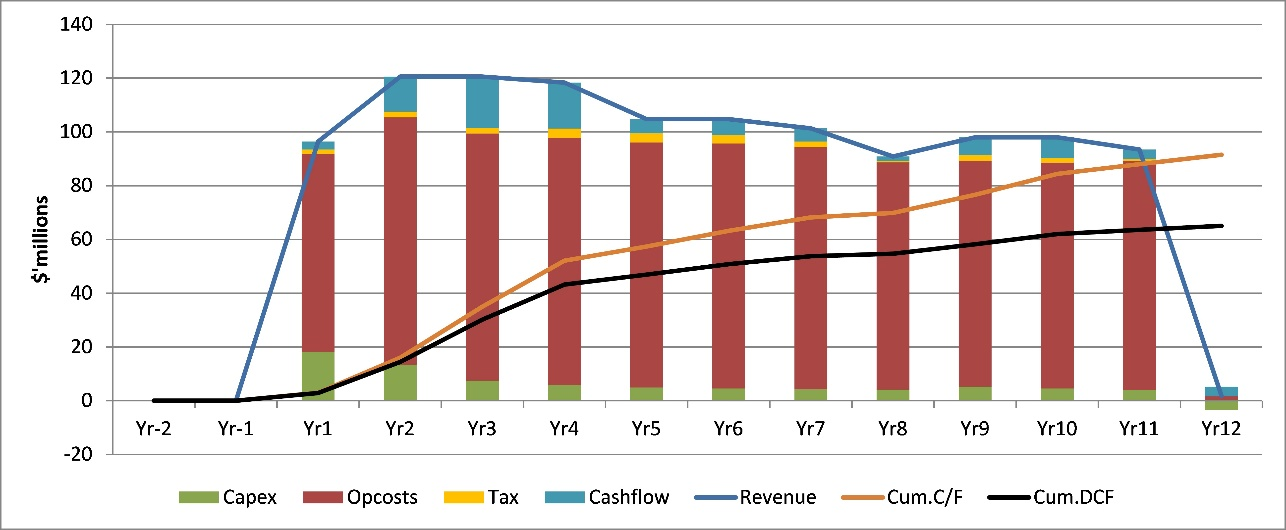

Annual base case cash flows and unit costs on a zinc equivalent basis are presented in the chart and table below.

Annual Cash Flow Forecast

Click Image To View Full Size

Unit cost estimate on Zinc Equivalent Basis

| LOM total (USD’000) | USD/t milled | Gross Rev. (%) | Margin (%) | USD/lb ZnEq | |

| Mining | 319,190 | 32.78 | 28% | 0.35 | |

| Mill/Concentrator | 240,745 | 24.72 | 21% | 0.27 | |

| G&A | 143,744 | 14.76 | 13% | 0.16 | |

| Direct site costs | 703,679 | 72.26 | 61% | 39% | 0.78 |

| Transport, TC/RC | 228,997 | 23.52 | 20% | 0.25 | |

| Cash Operating Costs | 932,676 | 95.78 | 81% | 19% | 1.03 |

| Royalties | 28,896 | 2.97 | 3% | 0.03 | |

| Production Taxes | – | – | 0% | – | |

| Total Cash Costs | 961,571 | 98.74 | 84% | 16% | 1.06 |

| Capital Expenditure | 72,700 | 7.47 | 6% | 0.08 | |

| Total Production Costs | 1,034,271 | 106.21 | 90% | 10% | 1.15 |

At an annual discount rate of 8.0%, the discounted cash flow evaluates to a net present value (NPV) of USD 65 million after tax. At an annual discount rate of 8.0%, the discounted cash flow evaluates to a net present value (NPV) of USD 81 million before tax.

Owing to the absence of pre-production capital expenditures in the forecast period, no internal rate of return (IRR) or payback period can be determined.

Risks and Opportunities

A summary of key risks and opportunities identified by the QPs is provided in the table below.

Risks and Opportunities

| Discipline | Opportunity | Risk |

| Geology and exploration | There are a number of exploration targets on the Campo Morado property that represent an excellent upside opportunity. They have the potential to add to the resource base with further work. | |

| Mineral resources | Several drill holes with missing assays have been assigned zero grade. If this information is found, it will likely have a positive impact on the grade in the local area of these drill holes. | A number of the Mineral Resource assumptions for reasonable prospects of eventual economic extraction at the Reforma, Naranjo, El Largo and El Rey deposits are based on analogues to G-9, including metallurgical recoveries and mining methods. Actual data collected from the deposits may vary from these assumptions.

There is a risk some of the Measured Mineral Resources at Reforma, Naranjo and El Rey will not have the appropriate drill support until grade control drilling is completed. The tonnages and grade for the potentially recoverable pillars at G9 are based on the assumption that a practical, economically feasible method can be developed to mine them. |

| Mine plan | The mining sequence has been prepared on an area-by-area basis and so there may be an opportunity to improve the production grade profile in a more detailed plan. | Evaluation is at a PEA level only. Mining engineering may reveal planning constraints not recognised in this study. |

| Tailings | Subject to further testwork, leach recovery of copper, gold and silver from reprocessing existing tailings may be possible. | Expansion of storage capacity require d to accommodate material in the PEA plan. |

| Process | Equipment for finer grinding is on site but not yet installed.

The Campo Morado tailings have a high precious metals content that may, in the future, be reprocessed if an economically viable method for precious metals recovery is developed | Achieving planned plant throughput and recovery into concentrate may increase operating costs. |

| Infrastructure | Telson has all of the infrastructure currently necessary to operate the Campo Morado Project. | |

| Environmental, closure, permitting and social | Telson has all the current environmental permits to operate. The communities and various groups in the area appear to support the resumption of mining activities.

Security is good at the present time, with a small military component on site, and Telson has the support of all social groups or factions in the area. Security should continue to improve as Telson continues to demonstrate a longer term commitment to the area | Environmental laws are tightened and become more stringent as a result of Mexico’s involvement in the Paris Agreement, NAFTA and various other Free Trade agreements.

Security becomes unstable within the state |

| Economics | Unit cost savings might be possible in some areas at the planned higher rates of plant throughput. | Project returns are sensitive to metal prices and any change in NSR terms.

Any significant changes to the fiscal regime would affect the cashflow forecast. |

About Telson Mining Corporation

Telson Mining Corporation is a Canadian based junior resource mining company currently in pre-production at two Mexican gold, silver and base metal mining projects and is advancing both towards commercial production, Campo Morado in the coming months of 2018 and Tahuehueto in early 2019. At the Campo Morado Mine in Guerrero, Mexico, Telson has re-commenced mining and processing operations with pre-production from mine development on a trial basis that commenced at an average 1,400 tonnes per day and is currently at approximately 1,900 tonnes per day during the recommissioning stage and intends to advance towards commercial production at full capacity of approximately 2,500 tonnes per day during 2018. Telson’s Tahuehueto Project, located in north-western Durango State, Mexico is currently in pre-production at approximately 150 tonnes per day utilizing a toll mill for processing and has entered a construction phase with a timeline to be producing on site in its own mineral processing plant capable of milling at least 1,000 tonnes per day in Q1, 2019. Regular metal concentrate delivery and sales are underway from both projects.

Visit: www.telsonmining.com

On behalf of the board of directors

(signed) “Ralph Shearing”

Ralph Shearing, P.Geol, President and Director

Qualified Persons

Mr. Eric Titley BSc, PGeo of Titley Consulting Ltd., independent Qualified Person (“QP”) under the guidelines of NI 43-101 prepared the mineral resource estimates and reviewed the geology and exploration disclosed in this news release. Mr. Christopher Jacobs CEng, MIMMM, of Micon International Limited (“Micon”), an independent QP, reviewed the capital and operating estimates, and economic analysis. Mr. William Lewis, B.Sc, P.Geo, of Micon, an independent QP, reviewed the environmental, closure, permitting and social aspects. Mr. James W.G. Turner BSc(Hons) ACSM, MSc MCSM, MIMMM CEng of Micon, and independent QP, reviewed tailings, metallurgy, process and infrastructure section. Mr. Bruce Pilcher CEng, FIMMM, FAusIMM (CP) of Micon, an independent QP, reviewed the mine plan. Each of Mr. Titley, Mr. Jacobs, Mr. Lewis, Mr. Turner and Mr. Pilcher have read and approved the contents of this news release. It should be noted that the above Qualified Persons are QPs for the Campo Morado Project but not the Tahuehueto PFS.

Cautionary Note Regarding Production Decisions and Forward-Looking Statements

It should be noted that Telson has commenced pre-production mining at both projects without the benefit of pre-feasibility or feasibility studies that outline mineral reserves. Furthermore, it is likely that Telson will declare commercial production at Campo Morado prior to completing a feasibility study of mineral reserves demonstrating economic and technical viability. Accordingly, readers should be cautioned that Telson’s production decision will likely be made without a comprehensive feasibility study of established reserves such that there is greater risk and uncertainty as to future economic results from the Campo Morado mine and a higher technical risk of failure than would be the case if a feasibility study was completed and relied upon to make a production decision. Telson has completed a preliminary economic assessment (“PEA”) mining study on the Campo Morado mine that provides a conceptual life of mine plan and a preliminary economic analysis based on the previously identified mineral resources (see News Release dated November 8, 2017 and April 2,2018 ). This will soon be replaced by a pre-feasibility study (“PFS”) that will allow the application of modifying factors to the mineral resources to allow a portion of them to be converted to mineral reserves; and will support the pre-production activities to bring the Campo Morado mine into commercial production.

Statements contained in this news release that are not historical facts are “forward-looking information” or “forward-looking statements” (collectively, “Forward-Looking Information”) within the meaning of applicable Canadian securities laws. Forward Looking Information includes, but is not limited to, disclosure regarding possible events, conditions or financial performance that is based on assumptions about future economic conditions and courses of action; the timing and costs of future activities on the Company’s properties, such as production rates and increases; success of exploration, development and bulk sample processing activities; timing for the restart of continuous mining operations at the Campo Morado Mine, and timing for processing at its own mineral processing facility on the Tahuehueto project site. In certain cases, Forward-Looking Information can be identified by the use of words and phrases such as “plans”, “expects”, “scheduled”, “estimates”, “forecasts”, “intends”, “anticipates” or variations of such words and phrases. In preparing the Forward-Looking Information in this news release, the Company has applied several material assumptions, including, but not limited to, that the current exploration, development, environmental and other objectives concerning the Campo Morado Mine and the Tahuehueto Project can be achieved, the continuity of the price of gold and other metals, economic and political conditions and operations. Forward-Looking Information involves known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of the Company to be materially different from any future results, performance or achievements expressed or implied by the Forward-Looking Information. There can be no assurance that Forward-Looking Information will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on Forward-Looking Information. Except as required by law, the Company does not assume any obligation to release publicly any revisions to Forward-Looking Information contained in this news release to reflect events or circumstances after the date hereof or to reflect the occurrence of unanticipated events.

Neither TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

For further information about Telson Mining Corporation, please contact:

Glen Sandwell

Corporate Communications Manager

ir@telsonmining.com

Tel: +1 (604) 684-8071

1 Cautionary statement NI 43-101: The PEA was prepared in accordance with National Instrument 43-101 Standards of Disclosure for Mineral Projects (“NI 43-101”). Note: The PEA is preliminary in nature and includes Inferred Mineral Resources that are considered too speculative geologically to have the economic considerations applied to them that would enable them to be categorized as Mineral Reserves, and there is no certainty that the PEA based will be realized. Mineral Resources are not Mineral Reserves and do not have demonstrated economic viability. Calendar years used are for illustrative purposes. Some figures may not sum exactly due to rounding. Unless otherwise indicated the currency used is United States dollars.

Click here to connect with Telson Mining Corporation and receive an Investor’s Presentation.

Source: www.thenewswire.com