The Conversation (0)

With all of this favorable press regarding gold and its intrinsic value, many investors have missed the news that prices for investment diamonds have actually performed slightly better than gold during the first half of this year.

By Vincenzo Desroches–Exclusive to Diamond Investing News

The year of 2010 will go down as one of uncertainty, risk adversity, and ineffective monetary and fiscal policies as developed countries of the world have tried all manner of schemes to get their respective economies back on track and out of the recession ditch. Gold and precious metals have reached historical highs, while the predictable flights of risk-averse capital have found safe havens in them, as well as in U.S. Treasury Bills. With all of this favorable press regarding gold and its intrinsic value, many investors have missed the news that prices for investment diamonds have actually performed slightly better than gold during the first half of this year.

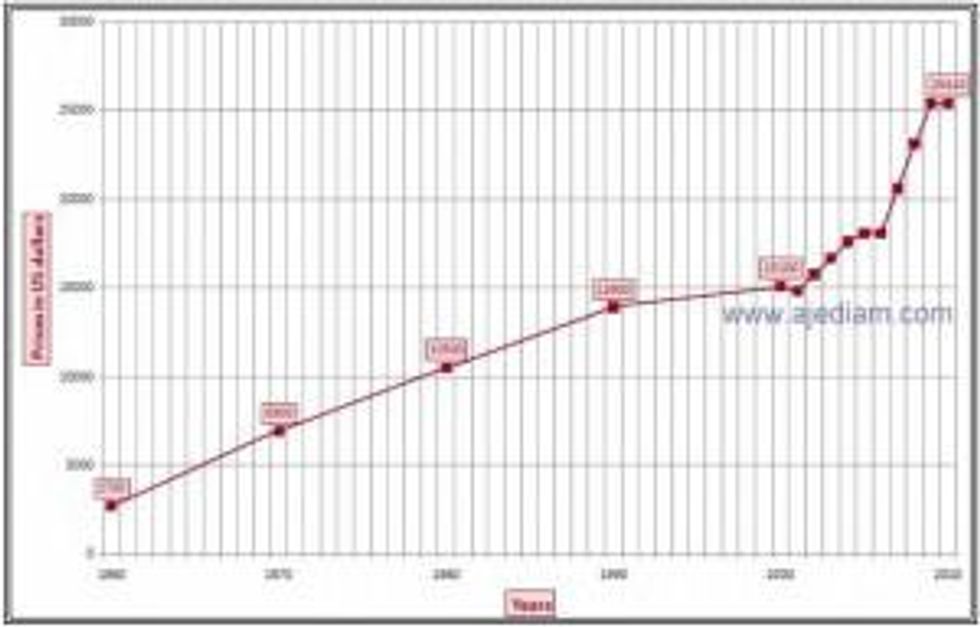

The actual tally has been 17 percent versus 16 percent in favor of investment diamonds for the first six months of the year. Not known for being a safe haven due to liquidity issues, diamond demand is outpacing supply, prices are on the rise again after the recession, and though a commodity, diamonds remain a wise hedge against inflation. One measure of this price performance is reflected in the following chart that depicts a 50-year history of the market price for a 1.0-carat diamond of premium, ideal cut:

The most recent recording in July of 2010 has been a price of $27,000, compared to a figure of $15,100 at the beginning of the decade. There has also been a 50 percnet increase in prices in just the past five years, although the recession did bring a slight pullback in momentum in 2009. Diamonds have always been treasured by consumers the world over. However, the market is unique in how it operates, and that uniqueness impacts its worthiness in an investor’s eye when it comes to choosing an investment vehicle.

Industrial uses for diamonds actually accounts for 80 percent of what comes out of mines, while 20 percent of production finds its way into the jewelry market. The De Beers Group, with nearly a 50 percent market share, controls the market supply for rough-cut diamonds in the absence of any commodity exchange for trading. The United State remains the largest consumer of diamonds in the world, accounting for 35 percent of all sales, but demand from China may cause a shift in leadership in subsequent years. Synthetic diamonds are available at lower cost, but these substitutes have not appreciably affected prices as with cultured pearls.

Polished diamond prices can vary widely due to the diamond’s carat, color, clarity and cut (The 4 C’s). Unlike pricing standards for precious metals, diamonds do not have specified prices per gram. Various professional groups within the industry publish pricing guides on a weekly or quarterly basis. The convoluted path taken by a rough diamond from mine, to grading table, to cutting and then to retail involves a global trek thought various countries and forex currency pairs. Forex broker reviews may be a necessity when attempting to invest in this international market.

Diamonds are an alternative investment vehicle, thereby necessitating specialized training and support from professionals in the market. Finding investment grade diamonds can be accomplished through respected dealer networks in the field. Investing directly in diamond mining companies offers another route and one where finding a buyer will not be as difficult when it comes time to sell.

Market trends are currently favorable. Prices have recovered, and from a supply perspective, the major mines have all passed their peaks. Demand will outstrip supply for the next decade as emerging economies in China and India transition to serving consumer-buying interests. Diamonds are the most concentrated sources of value on the planet, and their allure appeals to all cultures.