The Conversation (0)

Feb. 21, 2019 08:57AM PST

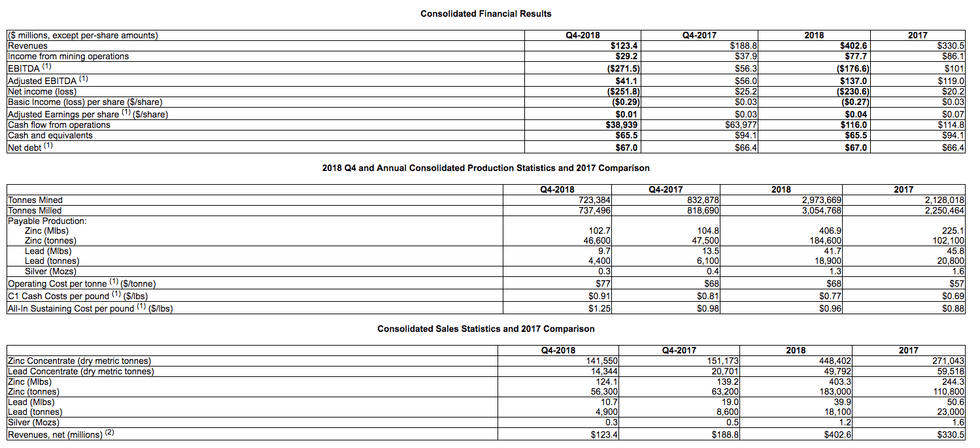

Trevali Mining Corporation (TSX:TV) (BVL:TV; OTC:TREVF; Frankfurt: 4TI) has released its audited annual financial results for the year ending December 31, 2018, with a net loss of $231 million, or ($0.27) per share, following non-cash impairment charges before tax of $312 million.

Trevali Mining Corporation (TSX:TV) (BVL:TV; OTC:TREVF; Frankfurt: 4TI) has released its audited annual financial results for the year ending December 31, 2018, with a net loss of $231 million, or ($0.27) per share, following non-cash impairment charges before tax of $312 million. The Company posted EBITDA1of ($177 million) and adjusted EBITDA1 (before impairments) of $137.0 million on total revenues of $403 million.

Summary:

- Total 2018 zinc production of 406.9 million payable pounds, in line with initial guidance of 400 – 427 million payable pounds set at the start of 2018. Total lead production of 41.7 million payable pounds and silver production of 1.3 million payable ounces.

- Consolidated cash costs of $0.77 per pound of payable Zn produced5 or $68 per tonne milled and all-in-sustaining costs5 of $0.96 per pound of payable Zn produced.

- Concentrate sales revenue of $402.6 million, up approximately 22% versus $330.5 million in 2017.

- Annual EBITDA1 of negative $177 million and annual net loss of $231 million or $0.27 per share. Annual Adjusted EBITDA1 of $137 million and Adjusted Earnings per Share of $0.04.

- Fourth quarter Adjusted EBITDA1 of $41 million and Adjusted Earnings per Share of $0.01.

- Maintained strong liquidity with cash of $65.5 million, Adjusted working capital position of $149 million, and net debt1 and total debt of $67.0 million and $132.4 million, respectively (as of December 31, 2018). In addition, $129 million remains available and undrawn on the revolving credit facility.

The negative EBITDA for year ended December 31, 2018 is due to the recognition of a non-cash impairment charge. The Company completed an impairment analysis which considered the indicators of impairment in accordance with IAS 36: Impairment of Assets; and reduced the carrying value of its mine operations by a net $263 million (comprised of $311.8 million impairment of property, plant and equipment and exploration and evaluation assets, goodwill and deferred tax recovery of $48.8 million). The Company is fully compliant with its debt covenants following the impairment.

Dr. Mark Cruise, Trevali’s President and Chief Executive Officer stated, “Over the past few months, we have completed a thorough review of our assets, which resulted in the non-cash impairment. However, efforts are underway at all our operations to maximize operating efficiencies and the Company is well positioned to improve operating performance going forward. In 2019, Trevali is placing an enhanced focus on improving transportation logistics and starting-up a new, more efficient power plant at Perkoa and is working with external consultant at Caribou to evaluate alternative, lower-cost mining methods. At Rosh Pinah, significant progress has been made over the past couple months understanding the new Western Ore Field, which accounts for approximately 80% of the mine’s reserves, with additional mill investments underway this year and the RP2.0 optimization study also progressing well. In Peru, the mine transitioned to fully owner operated and is well positioned for production in 2019 with all development in place for the year.”

“The full support of the Company’s banking syndicate on the $275 million of revolving credit facility and our healthy balance sheet place Trevali in a strong position to meet its commitments in 2019 and invest for the future,” continued Dr. Cruise. “We are committed to efficiently allocating capital, balancing the need for continued exploration and capital investment, with debt reduction and repurchasing shares under our existing normal course issuer bid.”

This news release should be read in conjunction with Trevali’s audited annual consolidated financial statements and management’s discussion and analysis for the year ended December 31, 2018, which is available on Trevali’s website and on SEDAR. Certain financial information is reported herein using non-IFRS measures. See Non-IFRS Financial Performance Measures below and in Trevali’s accompanying 2018 Management’s Discussion and Analysis.

2018 Annual and Q4 Financial Results and Conference Call

The Company will host a conference call and results presentation webcast at 10:30AM Eastern Time on Thursday, February 21, 2019 to review the 2018 operating and financial results. Participants are advised to dial in 5 minutes prior to the scheduled start time of the call.

Conference call dial-in details:

Date: Thursday, February 21, 2019 at 10:30AM Eastern Time

Toll-free (North America): 877-291-4570

International: 647-788-4919

Webcast: https://www.gowebcasting.com/9866

(1) Refer to the “Non-IFRS Financial Performance Measures” section of this press release.

(2) Revenues include provisional price adjustment and is calculated on a 100% basis. Fourth quarter 2018 revenues include a positive settlement adjustment of $1.6 million on sales from prior quarters.

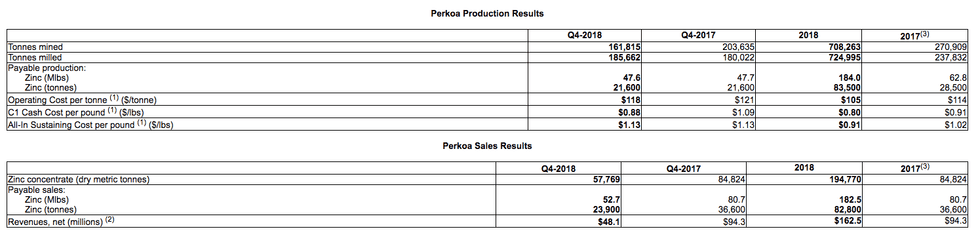

Perkoa Mine, Burkina Faso:

Q4 production was 47.6 million pounds (21,600 tonnes) of payable zinc. Metal sales for the quarter was 52.7 million pounds (23,900 tonnes) of payable zinc for net revenue of $48.1 million and resulted in Adjusted EBITDA1 of $11.7 million for the three months, prior to impairment and other non-cash charges that resulted in EBITDA1 of ($11.4 million).

Total ore milled in the fourth quarter of 2018 was slightly higher to the same period of the previous year. The decrease of mine site operating cost is consistent with the lower production volume in addition to the sale of a backlog of inventory at the end of 2017. In 2019, lower mined grades (estimated annual run-of-mine of 14.0% in 2019 versus 14.9% in 2018) will lead to reduced metal production and consequently slightly higher unit operating costs.

The Company approved the procurement of a more efficient site power generating station in the first quarter of 2018. This project entails the installation of two 2.5MW heavy fuel oil generators for an estimated capital cost of $9.2 million and is expected to reduce the mine’s operating cost by approximately $5 per tonne milled. The power generating station is expected to be commissioned in early 2019.

(1) Refer to the “Non-IFRS Financial Performance Measures” section of this press release.

(2) Revenues include effects of settlement adjustments on sales from prior quarters and is calculated on a 100% basis.

(3) The Perkoa Mine was acquired August 31, 2017. The 2017 comparatives include only the period of September to December 2017 result.

Rosh Pinah Mine, Namibia:

Q4 production was 25.4 million pounds (11,500 tonnes) of payable zinc and 1.5 million pounds (680 tonnes) of payable lead. Metal sales for the quarter were 39.1 million pounds (17,700 tonnes) of payable zinc and 3.3 million pounds (1,500 tonnes) of payable lead for $36.9 million in net revenue to deliver Adjusted EBITDA1 of $17.7 million for the three months, prior to impairment and other non-cash charges that resulted in EBITDA1 of ($64.5 million).

Zinc production was higher year-over-year as higher grades and recoveries offset lower mine output and mill throughput, as harder ore and head grades from the new Western Ore Field necessitated a reduction to milling rates. The increased operating cost per tonne1 is a direct result of lower milled tonnes due to higher feed grades from the mine.

Business improvement programs have been implemented to target key operational areas including production drilling support, introduction of raise-boring to improve the stope production cycle, improved ore blending strategies and mobile fleet optimization. The mine site is also implementing improved operational activity-based planning processes and compliance monitoring. The Rosh Pinah 2.0 optimization study remains on-going and is anticipated to be complete in the second half of 2019.

(1) Refer to the “Non-IFRS Financial Performance Measures” section of this press release.

(2) Revenues include effects of settlement adjustments on sales from prior quarters and is calculated on a 100% basis.

(3) The Rosh Pinah Mine was acquired August 31, 2017. The 2017 comparatives include only the period of September to December 2017 result.

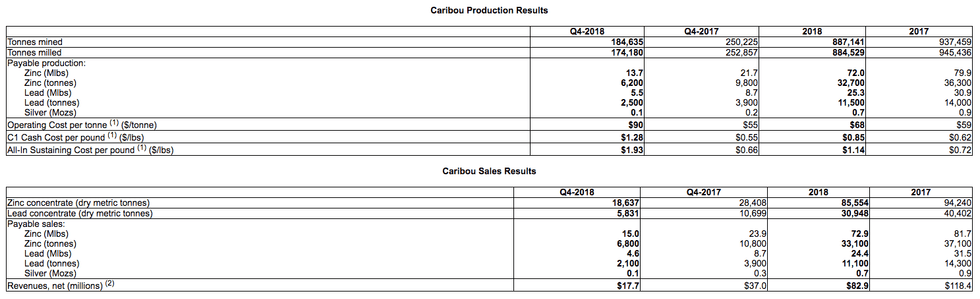

Caribou Mine, Canada:

Q4 production was 13.7 million pounds (6,200 tonnes) of payable zinc, 5.5 million pounds (2,500 tonnes) of payable lead and 0.1 million ounces of payable silver. Metal sales for the quarter were 15.0 million pounds (6,800 tonnes) of zinc, 4.6 million pounds (2,100 tonnes) of lead and 0.1 million ounces of silver for $17.7 million in net revenue to deliver Adjusted EBITDA1 of $2.6 million for the three months, prior to impairment and other non-cash charges that resulted in EBITDA1 of ($65.4 million).

Mine production for the quarter was 184,635 tonnes and mill throughput was 174,180 tonnes. The mine has experienced challenging hanging wall rock mass conditions leading to changes to geotechnical control management, primarily requiring the move to cemented rock fill from unconsolidated fill. As previously reported on October 22, 2018, adverse conditions were experienced in two mining zones resulting in the cessation of retreat mining and the subsequent loss of production (approaching 50,000 tonnes) from the remaining 2018 mine plan. This situation also led to a higher operating cost per tonne1 in the current quarter compared to the same quarter in the previous year.

Further external engineering studies are ongoing and in order to increase mining flexibility, Caribou management strategically slowed the mining rate in order to accelerate mine development in the fourth quarter 2018 through to the first quarter 2019 to build more optionality and stability in the mine to deliver safe, strong and reliable results in 2019. As part of the ongoing engineering studies, alternative mining methods are being evaluated with the objective of reducing costs to improve the mines productivity.

(1) Refer to the “Non-IFRS Financial Performance Measures” section of this press release.

(2) Revenues include effects of settlement adjustments on sales from prior quarters.

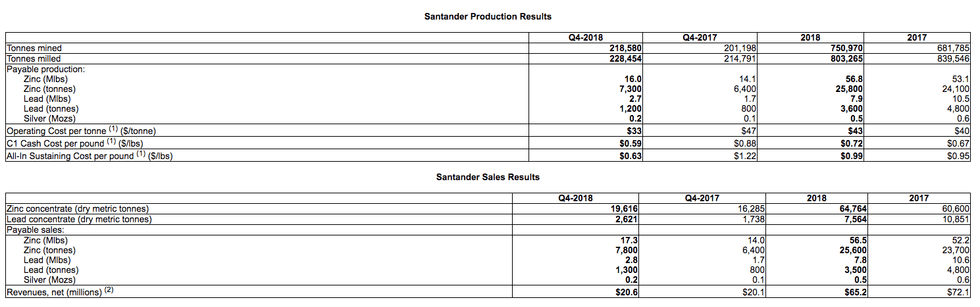

Santander Mine, Peru:

Q4 production was 16 million pounds (7,300 tonnes) of payable zinc, 2.7 million pounds (1,200 tonnes) of payable lead and 0.2 million ounces of payable silver. Metal sales for the fourth quarter were 17.3 million pounds (7,800 tonnes) of payable zinc, 2.8 million pounds (1,300 tonnes) of payable lead and 0.2 million ounces of payable silver for $20.6 million in net revenue to deliver Adjusted EBITDA1 of $11.6 million for the three months, prior to Impairment and other non-cash charges that resulted in EBITDA1 of ($77.0 million).

Mine production for the fourth quarter was 218,580 tonnes and mill throughput was 228,454 tonnes. Santander transitioned to fully owner operated in the quarter, recovered from third quarter production disruptions and managed to meet its forecasted annual production target delivering a 2018 monthly zinc production record for the mine in December. The mine is well positioned for production in 2019 with all development in place for the year.

(1) Refer to the “Non-IFRS Financial Performance Measures” section of this press release.

(2) Revenues include effects of settlement adjustments on sales from prior quarters.

2019 CONSOLIDATED PRODUCTION GUIDANCE

Production, operating cost and capital expenditure guidance remains unchanged from that reported on January 17, 2019. Consolidated production guidance for 2019 is estimated between 361 – 401 million pounds of payable zinc, 44 – 49 million pounds of payable lead and 1.3 – 1.5 million ounces of payable silver.

(1) Constitutes forward-looking information; see “Cautionary Note Regarding Forward-Looking Statements”.

(2) Trevali’s ownership interest is 90% of Perkoa and 90% of Rosh Pinah.

Consolidated operating costs are forecast to range from $69 – $76 per tonne, with C1 Cash Costs of between $0.81 – $0.88 per pound of zinc. Including capital expenditures forecast of $74 million, consolidated AISC are expected to range from $0.99 – $1.09 per pound of zinc (for the purpose of AISC guidance, all capital is considered to be sustaining). Relative to 2018, higher capital expenditures at Rosh Pinah and Santander are planned, with incremental spending on process plant upgrades (new filter press and floatation and grinding circuit improvements) and power infrastructure, respectively, the main drivers.

(1) Constitutes forward-looking information; see “Cautionary Note Regarding Forward-Looking Statements”.

(2) Trevali’s ownership interest is 90% of Perkoa and 90% of Rosh Pinah.

Quarterly Variability

Zinc: While production guidance has been provided on an annual basis, we expect moderate production fluctuations on a quarter-to-quarter basis due to mine scheduling. Zinc production overall is forecast to be slightly stronger in the second half of 2019, with Caribou expected to deliver a weaker quarter in Q1 as the Company completes the advanced rates of development and production catches up in Q2 – Q4. Conversely, Rosh Pinah is forecast to have a stronger start to 2019, with production strongest in Q1 and declining thereafter as zinc grades decline from approximately 10% to 8%. Due to the mining sequence, lower grades are planned at Perkoa in Q2 and Q3.

Lead: Production is expected to show more quarterly variability than zinc, with consolidated lead production increasing in each successive quarter throughout 2019. Lead grades at Santander and Rosh Pinah are forecast to increase throughout the year, with Rosh Pinah expected to mine significantly higher lead grades in the second half of 2019.

Operating costs: The Company expects costs to generally be at their highest level for each mine in Q1 with consolidated operating costs per tonne to range from $73–$81 per tonne during the quarter. Operating costs will be higher in Q1 compared to the yearly target due to the following:

- Increased mining scope to build inventories and further de-risk annual production;

- Seasonal impact of winter at Caribou Mine and reduced mined ore until planned development is in place;

- Benefit of the HFO generating plant at Perkoa is forecast to improve costs starting in Q2;

- Seasonal pumping requirements at Santander Mine; and

- Lower planned throughput due to planned maintenance.

Exploration – Targeting Resource and Reserve Growth and Mine Life Extensions

Exploration activities continued to focus on extending mineralized zones at depth at all operations. Specific highlights in 2018 include the emerging Santander Pipe deposit, which will remain a focus for 2019, extensions to the Perkoa deposit where the Hanging Wall zone was extended approximately 300 metres below the deepest level of the mine and material extensions along strike and at depth to the Western Ore field deposit at Rosh Pinah. Finally, regional exploration drilling commenced at Perkoa in Q4 of 2018 and has successfully intersected sulphide bearing (stringer – disseminated to narrow massive zones – non-economic to date) volcanogenic massive sulphide systems at several of the targets. Drill testing is ongoing.

The 2019 exploration program will continue to focus on brownfield, near-mine, exploration targets to expand and discover new resources in proximity to existing mine infrastructure and extend the current mine lives. For 2019, the Company intends to invest a minimum $8.4 million on approximately 36,300 metres of diamond drilling from surface and underground primarily focused on the Perkoa and Santander mineral systems. Contingent on positive results and available funds, additional funding may be deployed towards further drilling.

Updated resource and reserve estimates at all sites are expected to be completed at the end of the first quarter of 2019.

Qualified Person and Quality Control/Quality Assurance

EurGeol Dr. Mark D. Cruise, Trevali’s President and CEO, and Daniel Marinov, P.Geo, Trevali’s Vice President – Exploration, are qualified persons as defined by NI 43-101, and have supervised the preparation of the scientific and technical information that forms the basis for this news release.

ABOUT TREVALI MINING CORPORATION

Trevali is a zinc-focused, base metals company with four mines: the 90% owned Perkoa mine in Burkina Faso. the 90% owned Rosh Pinah mine in Namibia, the wholly-owned Caribou mine in the Bathurst Mining Camp of northern New Brunswick, and the wholly-owned Santander mine in Peru.

The shares of Trevali are listed on the TSX (symbol TV), the OTCQX (symbol TREVF), the Lima Stock Exchange (symbol TV), and the Frankfurt Exchange (symbol 4TI). For further details on Trevali, readers are referred to the Company’s website (www.trevali.com) and to Canadian regulatory filings on SEDAR at www.sedar.com.

On Behalf of the Board of Directors of

TREVALI MINING CORPORATION

“Mark D. Cruise” (signed)

Mark D. Cruise, President

Contact Information:

Steve Stakiw, Vice President – Investor Relations and Corporate Communications

Email: sstakiw@trevali.com

Phone: (604) 488-1661 / Direct: (604) 638-5623

Non-IFRS Financial Performance Measures

In this news release we refer to the following non-IFRS financial performance measures: Earnings Before Interest, Taxes, Depreciation and Amortization (“EBITDA”), Adjusted EBITDA, Operating Cost per tonne milled, C1 Cash Cost per pound and All-In Sustaining Costs (“AISC”) per pound. These measures are not recognized under IFRS as they do not have any standardized meaning prescribed by IFRS and are therefore unlikely to be comparable to similar measures presented by other issuers. Management uses these measures internally to evaluate the underlying operating performance of the Company for the reporting periods presented. The use of these measures enables management to assess performance trends and to evaluate the results of the underlying business of the Company. Management understands that certain investors, and others who follow the Company’s performance, also assess performance in this way.

Management believes that these measures reflect the Company’s performance and are useful indicators of its expected performance in future periods. This data is intended to provide additional information and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS.

EBITDA and EBIT:

EBITDA provides insight into Trevali’s overall business performance (a combination of cost management and growth) and is the corresponding flow drivers towards the objective of achieving industry-leading returns. This measure assists readers in understanding the ongoing cash generating potential of the business including liquidity to fund working capital, servicing debt, and funding capital expenditures and investments opportunities. EBITDA is profit attributable to shareholders before net finance expense, income and resource taxes and depreciation, depletion, and amortization. EBIT is EBITDA after depreciation, depletion, and amortization. Other companies may calculate EBITDA and EBIT differently.

Adjusted EBITDA and Adjusted Earnings per Share

Adjusted EBITDA consists of EBITDA less the impact of impairments or reversals of impairment and other non-cash expenses or recoveries. The non-cash expenses and recoveries are removed from the calculation of EBITDA as the Company does not believe they are reflective of the Company’s ability to generate liquidity and its core operating results.

Adjusted Earnings per Share consist of net income or loss in the period less the impact of impairments or reversals of impairment, gain (loss) on foreign exchange, business acquisition cost and other income or expenses.

Operating cost per tonne milled:

Cash operating cost per tonne milled measures the mine site operating cost per tonne milled. This measure includes mine operating production expenses such as mining, processing, administration, indirect charges such as surface maintenance and camp expenses, and inventory stock movement divided by tonnes milled. Operating cost per tonne milled does not include smelting and refining, distribution (freight), royalties, by-product revenues, depreciation, depletion, amortization, reclamation, and capital sustaining and exploration expenses.

C1 Cash Cost per pound:

C1 Cash Cost per pound measures the cash costs to produce a pound of payable zinc. This measure includes mine operating production expenses such as mining, processing, administration, indirect charges (including surface maintenance and camp), and inventory stock movement, smelting, refining and freight, distribution, royalties, and by-product metal revenues divided by pounds of payable zinc produced. C1 Cash Cost per Pound does not include depreciation, depletion, and amortization, reclamation expenses, capital sustaining and exploration expenses.

AISC per pound:

All-In Sustaining Cost per pound measures the cash costs to produce a pound of payable zinc plus the capital sustaining costs to maintain the mine and mill. This measure includes the C1 Cash Cost per Pound and capital sustaining costs divided by pounds of payable zinc produced. All-In Sustaining Cost per Pound does not include depreciation, depletion, and amortization, reclamation and exploration expenses.

See “Cautionary Notes Regarding Forward-Looking Statements” below as well as “Use of Non-IFRS Financial Performance Measures” in our Management’s Discussion and Analysis for the year ended December 31, 2018.

Cautionary Note Regarding Forward-Looking Statements

This news release contains “forward-looking information” within the meaning of the Canadian securities legislation and “forward-looking statements” within the meaning of Section 27A of the United States Securities Act of 1933, as amended, Section 21E of the United States Exchange Act of 1934, as amended, the United States Private Securities Litigation Reform Act of 1995, or in releases made by the United States Securities and Exchange Commission, all as may be amended from time. Statements containing forward-looking information express, as at the date of this news release, the Company’s plans, estimates, forecasts, projections, expectations, or beliefs as to future events or results. Such forward-looking statements and information include, but are not limited to statements as to the Company’s growth strategies, the leadership transition, expected annual savings from capital projects, demand for commodities, reduced interest payments, anticipated effects of commodity prices on 2019 revenues, expectations of positive operating cash flow and sufficient resources, estimation of mineral reserves and mineral resources, the realization of mineral reserve estimates, the timing and amount of estimated future production, costs of production, capital expenditures, success of mining operations, environmental risks, unanticipated reclamation expenses, title disputes or claims, future anticipated property acquisitions, the content, cost, timing and results of future anticipated exploration programs, life of mine expectancies and limitations on insurance coverage.

These statements reflect the Company’s current views with respect to future events and are necessarily based upon a number of assumptions and estimates that, while considered reasonable by the Company, are inherently subject to significant business, economic, competitive, political and social uncertainties and contingencies. If any assumptions are untrue, it could cause actual results, performance or achievements to be materially different from future results, performance or achievements expressed or implied by such statements. Assumptions have been made regarding, among other things, present and future business strategies and the environment in which the Company will operate in the future, including commodity prices, anticipated costs and ability to achieve goals.

Forward-looking statements are subject to known and unknown risks, uncertainties and other important factors that may cause the Company’s actual results, level of activity, performance or achievements to be materially different from those expressed or implied by such forward-looking statements, including but not limited to: risks related to joint venture operations; fluctuations in spot and forward markets for silver, zinc, base metals and certain other commodities (such as natural gas, fuel oil and electricity); fluctuations in currency markets; risks related to the technological and operational nature of the Company’s business; changes in national and local government, legislation, taxation, controls or regulations and political or economic developments in Canada, the United States, Peru, Namibia, Burkina Faso, or other countries where the Company may carry on business in the future; risks and hazards associated with the business of mineral exploration, development and mining (including environmental hazards, industrial accidents, unusual or unexpected geological or structural formations, pressures, cave-ins and flooding); risks relating to the credit worthiness or financial condition of suppliers, refiners and other parties with whom the Company does business; inadequate insurance, or inability to obtain insurance, to cover these risks and hazards; employee relations; relationships with and claims by local communities and indigenous populations; availability and increasing costs associated with mining inputs and labour; the speculative nature of mineral exploration and development, including the risks of obtaining necessary licenses and permits and the presence of laws and regulations that may impose restrictions on mining; diminishing quantities or grades of Mineral Resources as properties are mined; global financial conditions; business opportunities that may be presented to, or pursued by, the Company; the Company’s ability to complete and successfully integrate acquisitions and to mitigate other business combination risks; challenges to, or difficulty in maintaining, the Company’s title to properties and continued ownership thereof; the actual results of current exploration activities, conclusions of economic evaluations, and changes in project parameters to deal with unanticipated economic or other factors; increased competition in the mining industry for properties, equipment, qualified personnel, and their costs, as well as other risks as more fully described in the Company’s annual information form for the year ended December 31, 2017, which is available on the Company’s website (www.trevali.com) and filed under our profile on SEDAR (www.sedar.com). Investors are cautioned against attributing undue certainty or reliance on forward-looking statements. Although the Company has attempted to identify important factors that could cause actual results to differ materially, there may be other factors that cause results not to be as anticipated, estimated, described or intended. The Company does not intend, and does not assume any obligation, to update these forward-looking statements or information to reflect changes in assumptions or changes in circumstances or any other events affecting such statements or information, other than as required by applicable law.

Note to United States Investors

In accordance with applicable Canadian securities regulatory requirements, all mineral resource estimates of the Company disclosed or incorporated by reference in this news release have been prepared in accordance with Canadian National Instrument 43-101 – Standards of Disclosure for Mineral Projects, classified in accordance with Canadian Institute of Mining Metallurgy and Petroleum’s “CIM Standards on Mineral Resources and Reserves Definitions and Guidelines”.

The Company uses the terms “measured mineral resources”, “indicated mineral resources” and “inferred mineral resources”. While these terms are recognized by Canadian securities regulatory authorities, they are not recognized by the United States Securities and Exchange Commission. US investors are cautioned not to assume that any part or all of the material in these categories will ever be converted into reserves.

Click here to connect with Trevali Mining Corporation (TSX:TV) for an Investor Presentation.

Source: globenewswire.ca