The Conversation (0)

Galan Lithium Limited (ASX:GLN) (Galan or the Company) is pleased to announce a further consolidating increase to its JORC (2012) reported Mineral Resource estimate for the Hombre Muerto West Project (HMW Project) located in Catamarca Province, Argentina. The revised Mineral Resource estimate was completed by a team of leading independent geological consultants, WSP Chile (WSP).

The maiden HMW Project Mineral Resource Estimate (refer Galan ASX release dated 12 March 2020) was prepared by SRK and was further upgraded on 17 November 2020, 24 October 2022 and 1 May 2023. Each upgrade has not only significantly increased the Total Resource inventory but also enhanced the Resource category classifications and hence confidence in the viability and robustness of the HMW project. This latest resource upgrade enhances Galan’s objective to achieve the necessary production conditions for Stage 3 (40Ktpa LCE), towards our four-stage lithium production target of up to 60ktpa LCE (including Candelas).

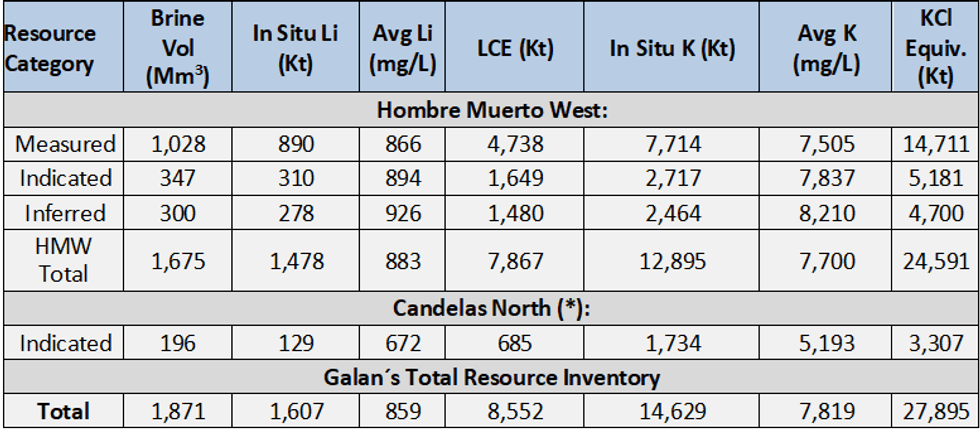

Table 1 Mineral Resource Statement for Hombre Muerto West and Candelas (effective date 26 March 2024)

Table 1 Mineral Resource Statement for Hombre Muerto West and Candelas (effective date 26 March 2024)

(*) Candelas North tenements are located about 40 km to the Southeast of the HMW Project. The Candelas North Mineral Resource Statement was originally announced by Galan on 1 October 2019.

Commenting on the significant Resource upgrade, Galan’s Managing Director, Juan Pablo (JP) Vargas de la Vega, said:

“This latest significant upgrade in the high grade, low impurity HMW Resource highlights the potential enormity of the brine resource that sits within Galan’s 100% owned tenements in Argentina. The initial HMW resource in March 2020 was 1.08Mt LCE @ 946mg/L Li, upgraded in May 2023 to 6.6MT LCE @ 880mg/L Li. This has now been increased a further ~20% to a tier one size of 8.6Mt LCE at 859mg/L Li, with the inclusion of our Catalina tenements. Coupled with our Candelas resource, Galan has a very solid foundation, and more importantly has delivered a further validation that its Hombre Muerto Salar resources fully support our four-stage lithium production target of up to 60ktpa LCE.

The HMW Project is robust and underpinned by strong financial metrics as illustrated in its Stage 1 and Stage 2 DFS results. We constantly evaluate opportunities to increase the value of the HMW Project in parallel with continuing to construct Stage 1 as we look forward to first commercial production in 1H 2025.”

Summary of Resource Estimate and Reporting Criteria

The Mineral Resource Estimate (MRE) for lithium (reported as Li2CO3 equivalent) and potassium (KCl equivalent) were completed by WSP (Chile). This updated MRE incorporates geological and geochemical information obtained from thirty one (31) drillholes totalling 9,043 metres within the Pata Pila, Rana de Sal I, Rana de Sal II, Casa del Inca III, Catalina, Del Condor, Pucara del Salar, Delmira, Don Martin, El Deceo I, El Deceo II, El Deceo III and Santa Barbara tenements (see Figure 1). A total of 697 brine assays were used as the foundation of the estimate, all of which were analysed at Alex Stewart International laboratory (Jujuy, Argentina). The QA/QC program includes duplicates, triplicates, and standards, In total, 376 QA/QC samples were considered using Alex Stewart (duplicates) and SGS in Argentina (triplicates) as the umpired laboratory.

Click here for the full ASX Release

This article includes content from Galan Lithium, licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.