The Conversation (0)

Alvo Minerals Limited (ASX: ALV) (“Alvo” or the “Company”) is pleased to provide its Quarterly Activities Report for the period ending 31 March 2023*. Alvo is exploring its Palma VMS Project in Brazil (“Palma Project” or the “Project”), a Project that has significant high-grade copper and zinc potential in existing prospects, brownfields prospects and greenfields targets within a district scale exploration package.

HIGHLIGHTS

*Refer to the detailed explanation of assumptions and pricing underpinning the copper equivalent (CuEq) on page 11 of this Quarterly Activities Report

Exploration Activities

Diamond Drilling at the Palma VMS Project

During the reporting period, Alvo announced assay results from its extensional diamond drill program at the C3 prospect, within the Palma Project in central Brazil1.

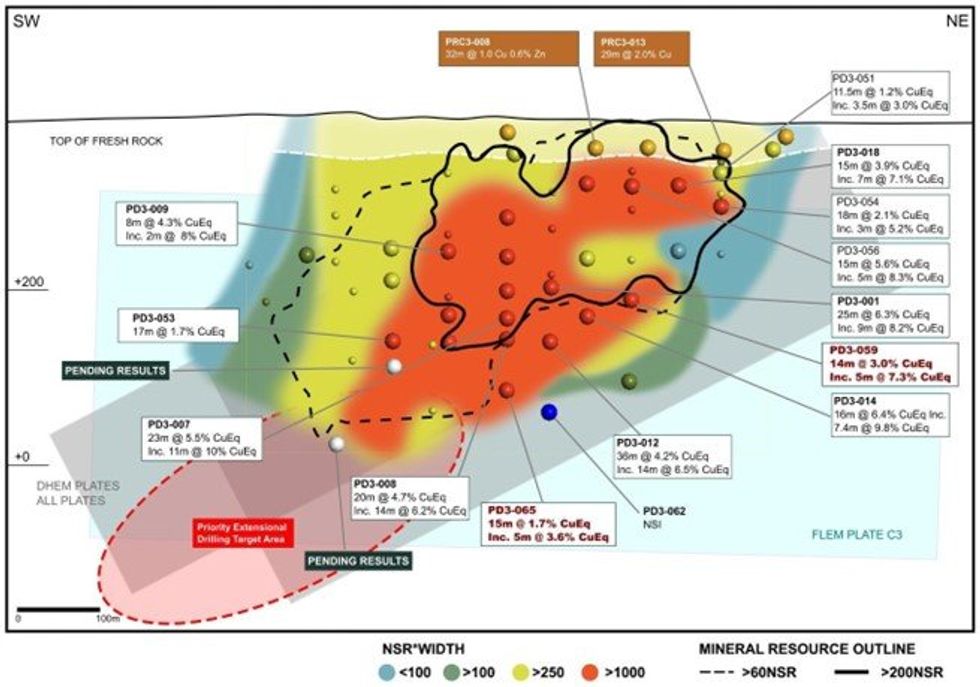

Phase 2 drilling at the C3 prospect is aiming to significantly expand the existing Palma Project JORC 2012 MRE2 of 4.6Mt @ 1.0% Cu, 3.9% Zn, 0.4% Pb & 20g/t Ag (see Figure 1). Phase 2 drilling follows an exceptional Phase 1 drill program that delivered high-grade Copper and Zinc in thick VMS intercepts. Phase 1 and initial Phase 2 drill results continue to exceed expectations on grade and thickness when compared to the existing JORC 2012 MRE that used historical drilling only.

Figure 1: C3 Long section illustrating selected significant intercepts, DHEM plates and Phase 2 drilling.

Figure 1: C3 Long section illustrating selected significant intercepts, DHEM plates and Phase 2 drilling.

C3 Upgrade Drilling

Phase 2 diamond drilling resumed during the reporting period and is targeting extensions to the high-grade VMS mineralisation, predominately focusing on the down-dip extensions emerging on the south-westerly plunge orientation from the known mineralisation. The Company believes this is the most prospective orientation extension defined to date.

Click here for the full ASX Release

This article includes content from Alvo Minerals, licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.