The Conversation (0)

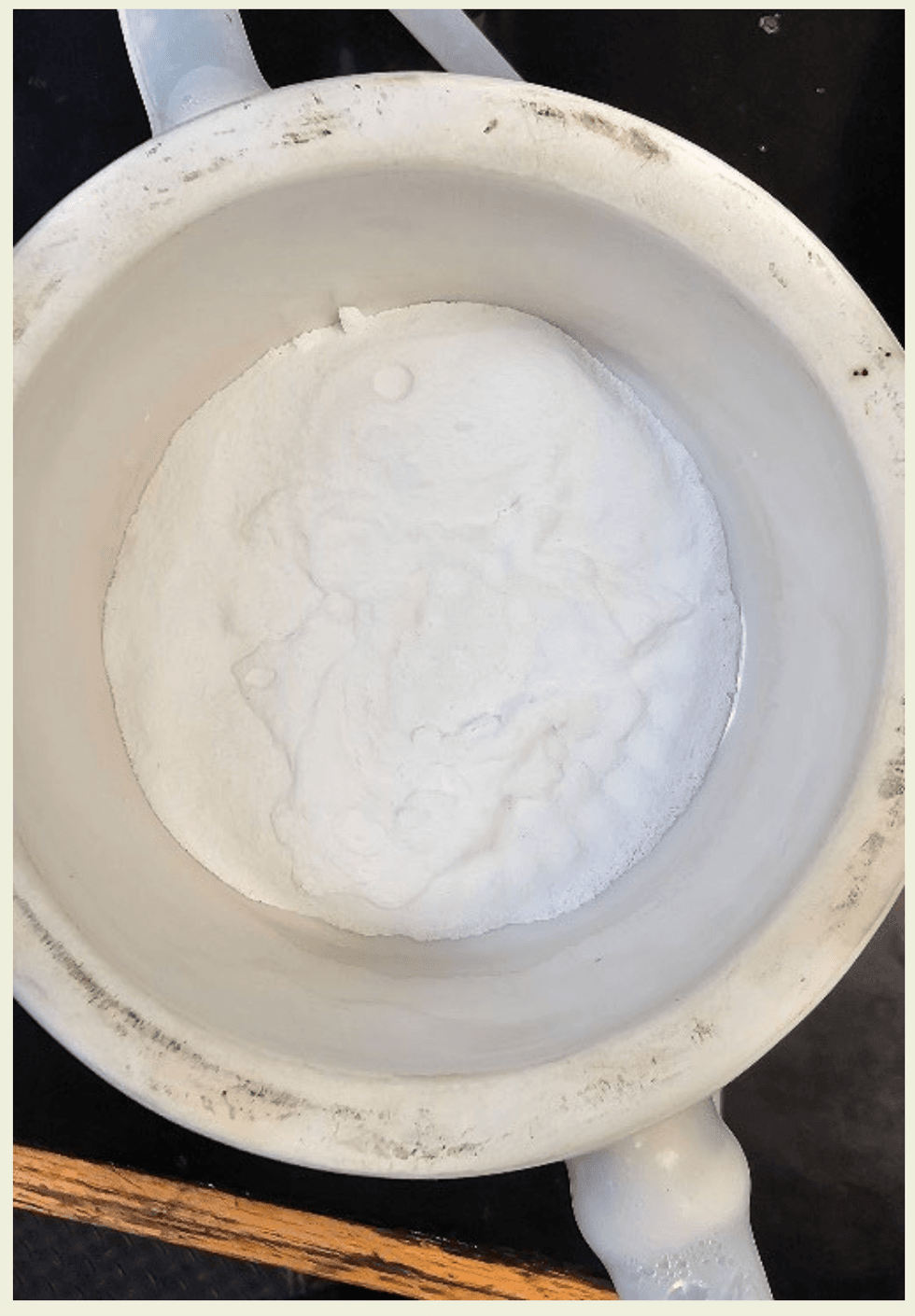

Jindalee Lithium Limited (Jindalee, the Company) is pleased to announce that battery-grade lithium carbonate has been successfully produced from ore from the McDermitt Lithium Project (the Project) (Figure 1). This marks an important milestone, with all steps of the processing flowsheet for the Project from ore beneficiation and leaching to purification and production of battery-grade lithium carbonate now validated (Figure 2).

Fig 1 – McDermitt Lithium Carbonate

Fig 1 – McDermitt Lithium Carbonate

Jindalee’s CEO Ian Rodger commented:

"The successful production of battery-grade lithium carbonate from McDermitt ore is a major milestone for Jindalee. This achievement substantially de-risks our processing flowsheet and demonstrates the potential for McDermitt to supply high-quality lithium chemicals to the expanding US battery value chain.

We have been greatly encouraged by the exceptional results we have achieved since commencing the PFS metallurgical test work program with Fluor and Hazen in mid-2023 and anticipate that these results will meaningfully support the outcomes of the McDermitt Lithium Project PFS which is now due for release in Q4 CY 2024.”

Discussion

After investigating various alternatives, in March 2023 acid leaching with beneficiation (see Figure 2) was selected as the preferred flowsheet for the Project2. This decision followed a review of prior test work and high-level benchmarking of five comparator lithium projects by the global engineering, procurement, construction and maintenance company Fluor Corporation (Fluor), which indicated that acid leaching with beneficiation was expected to produce the best economic outcome for the Project. The resultant McDermitt flowsheet (Figure 2) is very similar to that utilised and extensively validated by Lithium Americas Corporation (TSX: LAC) at its Thacker Pass project, which is currently under construction and is also located in the McDermitt Caldera (~30km south of the McDermitt Lithium Project).

Fluor was subsequently appointed as lead engineer for the McDermitt PFS in June 20233, including managing an extensive bench scale metallurgical test work program at Hazen Research Inc. in Colorado, USA, aimed at validating the preferred flowsheet and providing data to inform the PFS (PFS Test Work). To date Jindalee has announced exceptional results from the McDermitt PFS Test Work including results from beneficiation test work in November 20234 and acid leaching in January 20245. Respective highlights include:

Subsequent to the acid leaching test work described above, an additional 300 kg composite sample (250 µm, comprising Units 4, 6, 8, and 10) was leached, yielding lithium in solution (leachate) for downstream test work (post-leach process steps – see Figure 2). The purification of the lithium-rich solution was successfully completed, resulting in the first production of battery-grade lithium carbonate, assaying 99.8% Li₂CO₃ with acceptable levels of deleterious elements in accordance with a typical third-party contract specification. This achievement significantly de-risks the Project by demonstrating the effectiveness of all process steps of the flowsheet at bench scale. Reaching this milestone provides strong validation of the flowsheet developed for McDermitt.