The Conversation (0)

Galan Lithium Limited (ASX: GLN) (Galan or the Company) is pleased to announce that the Catamarca Ministro – Ministerio de Mineria (Mines Department Minister) has granted Galan the full Phase 2 mining permit for 21ktpa LCE production at its 100% owned HMW lithium brine project in Argentina. The grant of the permit means Galan has the ability to expand production up to 21ktpa LCE, subject to securing project finance and following the delivery of Phase 1 (up to 5.4ktpa LCE).

Highlights

“We are delighted with the grant of the Phase 2 mining permit which continues to solidify our strong relationship with the local Catamarcan authorities. It will allow Galan to increase production over threefold from Phase 1 and produce a premium quality lithium chloride product, which is in high demand.

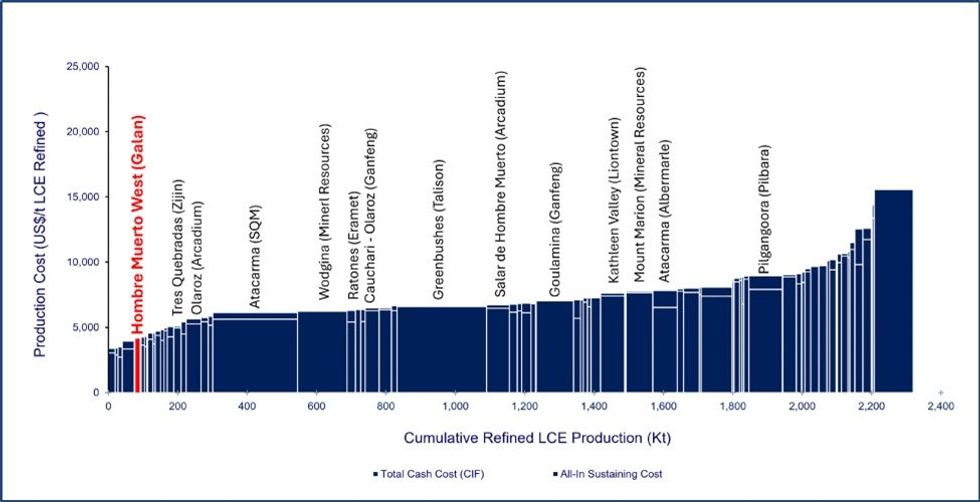

Importantly, HMW is positioned in the first quartile of the cost curve and Phase 2 production would be cash flow positive even at today’s prevailing lithium carbonate prices. HMW is now poised to be a long term and resilient globally significant source of lithium supply.”

Figure 1. Wood Mackenzie 2028 Lithium Cost Curve: AISC (US$/t LCE)Wood Mackenzie Disclaimer “The foregoing information was obtained from the Lithium Cost Service™ a product of Wood Mackenzie.” "The data and information provided by Wood Mackenzie should not be interpreted as advice and you should not rely on it for any purpose. You may not copy or use this data and information except as expressly permitted by Wood Mackenzie in writing. To the fullest extent permitted by law, Wood Mackenzie accepts no responsibility for your use of this data and information except as specified in a written agreement you have entered into with Wood Mackenzie for the provision of such of such data and information." Information sourced in December 2024.

Figure 1. Wood Mackenzie 2028 Lithium Cost Curve: AISC (US$/t LCE)Wood Mackenzie Disclaimer “The foregoing information was obtained from the Lithium Cost Service™ a product of Wood Mackenzie.” "The data and information provided by Wood Mackenzie should not be interpreted as advice and you should not rely on it for any purpose. You may not copy or use this data and information except as expressly permitted by Wood Mackenzie in writing. To the fullest extent permitted by law, Wood Mackenzie accepts no responsibility for your use of this data and information except as specified in a written agreement you have entered into with Wood Mackenzie for the provision of such of such data and information." Information sourced in December 2024.

Wood Mackenzie’s emissions benchmarking service has also placed HMW within the first quartile of the industry greenhouse gas emissions curve. Strong environmental, social and governance principles have been a governing tenet of the development strategy for HMW, which focuses on the production of a lithium chloride concentrate from conventional evaporation allowing for significantly reduced energy and water consumption. In line with Galan’s commitment to social principles, at least 70% local content in employment and contracting opportunities has been targeted at HMW and remains a keen focus for the Government of Catamarca and Galan. Skills and training opportunities have been provided to increase local participation, with a view to creating a skilled local workforce and supply chain for sustainable long-term operations.

Galan has demonstrated considerable progress on the HMW project, including:

Chairman of Galan, Richard Homsany, commented:

“The grant of the Phase 2 mining permit is testament to the hard work and commitment of our dedicated team, and also highlights the strong long-term relationships we have fostered with the Government of Catamarca and local communities, who we sincerely thank for their continued ongoing support. Through action we have demonstrated the benefits of our HMW operations: economically though the generation of employment, procurement and trade opportunities and socially through education, community programs and training opportunities. We look forward to continuing to work in co-operation with the Government of Catamarca and all stakeholders to maximise the benefits of Galan’s operations in the community, and ensure they are sustainable.”

The HMW project is separated into four production phases. The Phase 1 DFS is based on the production of 5.4ktpa LCE of lithium chloride concentrate, with production anticipated in the second half of 2025.

The Phase 2 DFS, announced on 3 October 2023, targets medium-term production of 21ktpa LCE of lithium chloride concentrate. Arcadium Lithium Plc, which is subject to a change of control transaction from Rio Tinto Limited, produced around 20ktpa LCE from the adjacent mining permit at Salar de Hombre Muerto in 2023.

Phase 3 at HMW aims to achieve 40ktpa LCE within a 2-5 year horizon whilst Phase 4 represents a longer-term target of 60ktpa LCE, leveraging lithium brine sourced from both HMW and Galan’s other 100%-owned project in Argentina, Candelas.

The phased development of the HMW and Candelas Mineral Resources mitigates funding and execution risk and allows for continuous process improvement. The production of lithium chloride as a product is in demand from lithium converters as battery chemistry is trending towards lithium iron phosphate technology. Galan received permission to sell lithium chloride from the Catamarca Government earlier in 2024.

The Phase 2 mining permit also supports Galan’s application for the Argentinian Régimen de Incentivo para Grandes Inversiones (RIGI). Subject to meeting the eligibility criteria for RIGI, the RIGI can provide the following key incentives:

Galan’s JP Vargas de la Vega further stated:

“Our plan for HMW is unchanged, beginning with Phase 1. Our immediate focus is finalising the financing and offtake arrangements for Phase 1. Once secured, our operations team will complete construction and commence first production of lithium chloride concentrate. While the operations team advances Phase 1 construction our corporate team, supported by advisors, will commence a project financing process for Phase 2.”

Click here for the full ASX Release

This article includes content from Galan Lithium, licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.