The Conversation (0)

Green Technology Metals Limited (ASX: GT1) (GT1 or the Company) is pleased to advise that drilling has commenced at its Root Project, located approximately 200 km west-north-west of GT1’s flagship Seymour Project. Drilling is initially focussed on the McCombe LCT pegmatite.

HIGHLIGHTS

“Commencing drilling at Root is another significant milestone for our business. The initial focus at the advanced McCombe LCT pegmatite is confirmation and extension of known mineralisation, followed by rapid estimation of a maiden Mineral Resource estimate. We then plan to target other known spodumene-bearing LCT pegmatites at Root, including Morrison and Root Bay.”

- GT1 Chief Executive Officer, Luke Cox

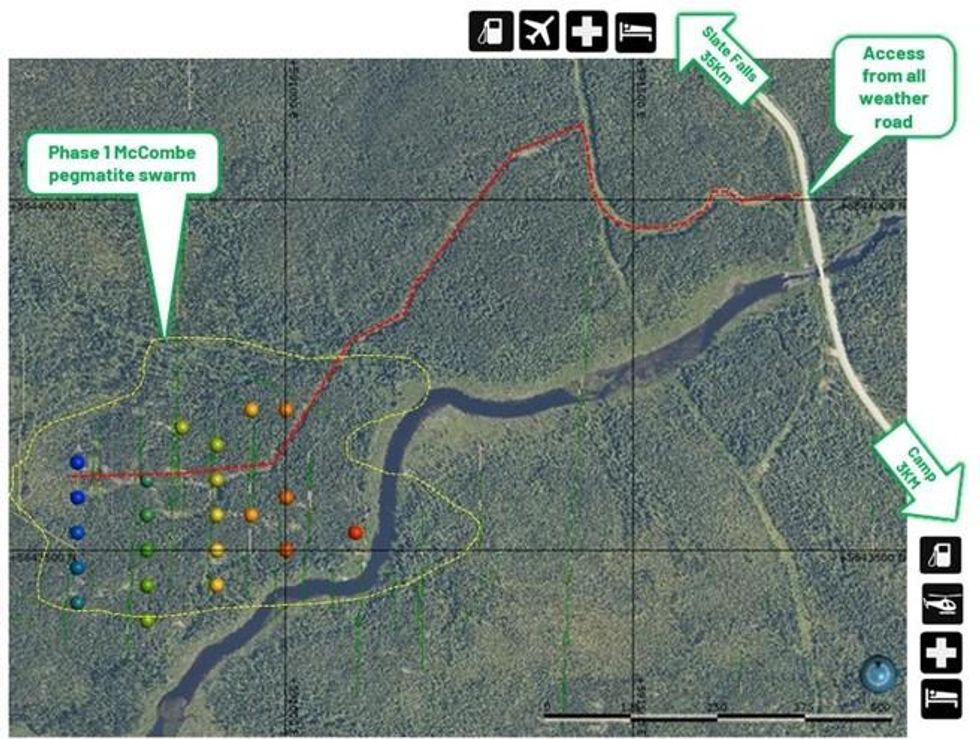

McCombe drilling program at Root

Initial drilling at McCombe (22 holes for 2,500m) is targeted to confirm historical drilling and sampling. The second phase of drilling is then planned to test for extensions of the mineralised pegmatites in all directions, infill key sections and rapidly facilitate delineation of a maiden Mineral Resource estimate for the Root Project.

The McCombe LCT (Lithium-Caesium-Tantalum) pegmatite is the most advanced prospect at Root. Historical drilling completed by Ardiden Limited in 2016 saw six holes drilled, which intersected numerous pegmatites, generally dipping to the south and striking east-west. This drilling confirmed historical drill results and demonstrated the down dip continuity of the lithium mineralisation, including a key extensional intercept of 67m @ 1.75% Li2O (see GT1 ASX release dated 8 November 2021, Prospectus).

Figure 1: Phase 1 drill collars at McCombe pegmatite – confirmation program of 22 holes for 2,500m

Field geologists continue to map the known LCT pegmatites, and determine their exposed lateral extents, across the broader Root Project. In combination with the recently acquired aerial photography, aerial geophysics and Lidar bare earth interpretations, a pipeline of initial targets for further field testing is being established at Root.

Click here for the full ASX release