The Conversation (0)

In mid-November 2023, Jindalee Lithium Limited (Jindalee, the Company) announced results from beneficiation of composite samples from the Company’s 100% owned McDermitt Lithium Project located in Oregon, USA, and noted that acid leaching of beneficiated samples was underway1.

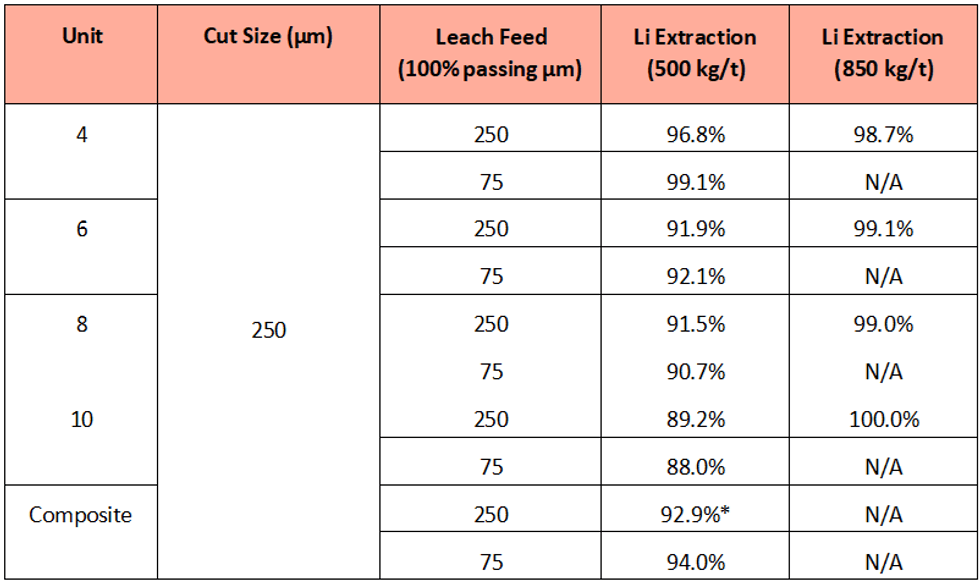

Jindalee is pleased to advise that initial results from acid leaching of the beneficiated samples have been received, with extremely high lithium extraction rates recorded from both the 250µm and 75µm leach feeds using 500kg sulphuric acid per tonne of leach feed. The 250µm leach feed was also leached with a higher strength acid (850 kg/t leach feed) and returned exceptional extraction rates (>98.5%) for all units (Table 1).

Table 1 – Maximum Lithium Extraction at variable feed sizes and acid strengths - Units 4, 6, 8 and 10 (* calculated)

Table 1 – Maximum Lithium Extraction at variable feed sizes and acid strengths - Units 4, 6, 8 and 10 (* calculated)

The leach testwork extended for up to four hours with most of the Li extraction occurring in the first hour. Optimised lithium extraction and acid addition rates will be incorporated into the Pre-Feasibility Study (PFS).

Leaching of a bulk composite has commenced to provide lithium in solution for downstream testwork. Beneficiated samples (250µm) have also recently been shipped to POSCO Holdings (NYSE: PKX) (POSCO) for testwork, pursuant to the Memorandum of Understanding signed with POSCO in February 20234.

Discussion

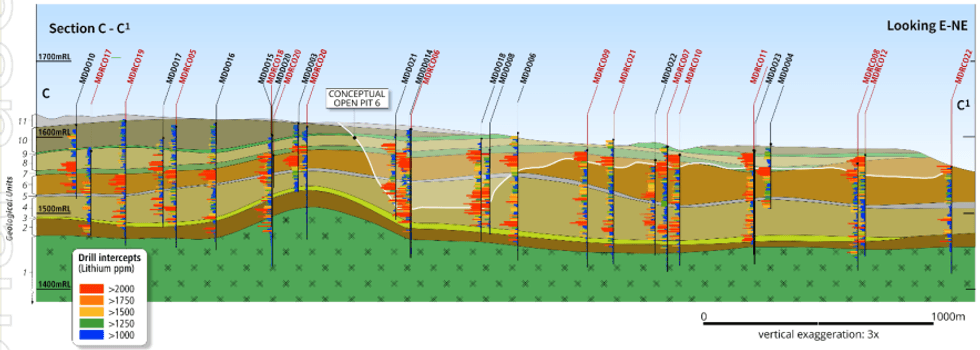

In July 2023 Jindalee shipped approximately 700kg of drill core to Hazen (Colorado, USA) for metallurgical testing, with this testwork being managed by global engineering, procurement, construction and maintenance (EPCM) company Fluor Corporation (Fluor). The core samples were selected from Units 4, 6, 8 and 10 within the Indicated portion of conceptual Pit Shell 6 (nominal 43 years); these units carry elevated lithium grades and selective mining of these units has the potential to deliver significantly higher-grade material (when compared to the Mineral Resource Estimate average grade) for processing (Figure 1) (Table 2)2.

Figure 1 – Schematic Section C-C’ with completed drilling, simplified geology and conceptual Pit Shell 6 (nominal 43 years). (Note: lateral projection onto section plane and 3x vertical exaggeration may cause distortion)

Figure 1 – Schematic Section C-C’ with completed drilling, simplified geology and conceptual Pit Shell 6 (nominal 43 years). (Note: lateral projection onto section plane and 3x vertical exaggeration may cause distortion)

Head assays for these samples were announced in October 20233 with Units 4, 6, 8 and 10 averaging 1,790 ppm Li, 34% higher than the average McDermitt Mineral Resource grade (1,340 ppm Li)2. Results from attrition scrubbing (beneficiation) of a composite sample of McDermitt ore (250µm cut-size) were announced mid- November 2023, recording 92.0% Li recovery with 25.3% mass rejection and the lithium grade to leach increasing to 2,107 ppm Li1.

The acid leaching testwork now being reported was conducted on both 250µm and 75µm leach feed sizes using 500 kg/t (and 850 kg/t for 250µm leach feed). A composite sample (representing a nominal life-of-mine average feed) was also tested using the two leach feed sizes, recording very high lithium extraction rates using 500 kg/t. Lithium extraction from the coarser (250µm) leach feed was 92.9% and compares favourably with the extraction rate (94.0%) achieved from the finer (75µm) leach feed (Table 1).

Next Steps

Acid leaching of a bulk composite sample is currently underway to provide lithium in solution for downstream work. Results from this testwork will feed into the PFS which is expected to be completed mid-2024.

Samples from Units 4, 6, 8 and 10 have been beneficiated (250µm) and shipped to POSCO for parallel leach testwork, pursuant to the Memorandum of Understanding signed with POSCO.

Click here for the full ASX Release

This article includes content from Jindalee Lithium Limited, licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.