The Conversation (0)

Green Technology Metals Limited (ASX: GT1) (GT1 or the Company), a Canadian-focused multi-asset lithium business, is pleased to announce that it has signed a binding option agreement (Option Agreement) for an option (Option) to purchase an 80% interest (80% Option Interest) in the Junior Lake Project (Junior Lake or the Project) from Landore Resources Canada Inc. (Landore) which comprise 591 staked mineral claims on 10,856 Hectares (109km2) of tenure located adjacent to the Flagship Seymour Project (Seymour) in Ontario, Canada.

HIGHLIGHTS

The tenements are located immediately adjacent (approximately 22km) from the Company’s Flagship Seymour project in Ontario, The Junior Lake Project is host to three drill-ready LCT pegmatite prospects, identified from previous exploration, indicating the Project’s lithium potential.

“We are excited to secure the agreement with Landore, adding a sizeable tenement package to our portfolio and look forward to commencing exploration on the Junior Lake Project which offers the company a unique combination of a close proximity location, identified targets through previous regional exploration and early indications of similar geology to our flagship Seymour Project.

We plan to commence exploration activities imminently at Junior Lake as we look to grow our resource base for greater Seymour and move swiftly into development ”

GT1 Chief Executive Officer, Luke Cox

Project Background

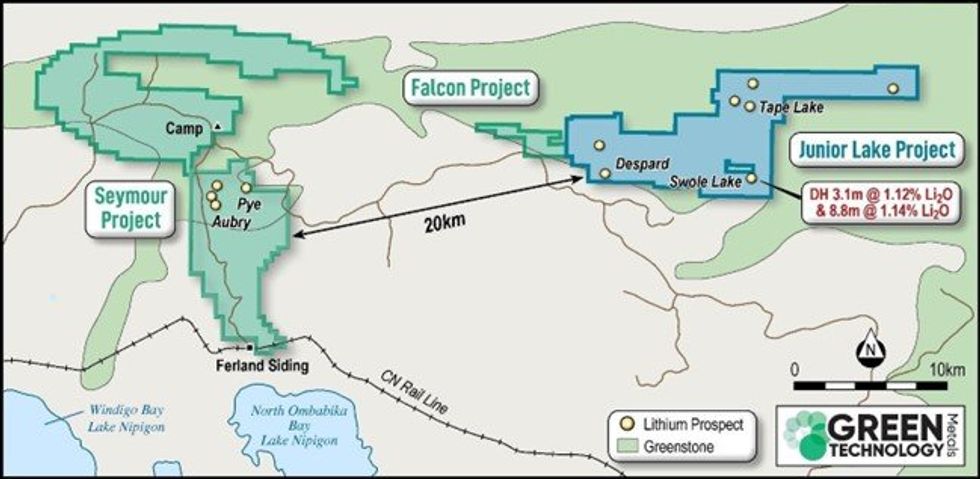

The Junior Lake Project, currently 100% owned by Landore, consists of 33,029 hectares, including 10,856 hectares relating to Lithium tenure (refer to figure 1) in the province of Ontario, Canada. The project is located approximately 235 kilometres north-northeast of Thunder Bay and 75km east-northeast from the town of Armstrong and easily accessible via Jackfish Highway which connects the Seymour, Falcon and Junior Lake project areas.

Junior Lake is located within the Caribou Lake – O’Sullivan greenstone belt of the East Wabigoon Sub province of the Superior Province, a highly prospective Archean greenstone belt known host to multiple known gold and other precious and base metal occurrences. The greentone belt traverses the Junior Lake Property from east to west for approximately 31 kilometres and ranges from 0.5 to 1.5 kilometres wide containing all of Landore’s stated mineral resources and prospects including the BAM Gold Deposit, Lamaune Gold Prospect, the B4-7 Nickel-copper-cobalt- Platinum-Palladium-gold Deposit and the VW Nickel-Copper-cobalt Deposit. Previous exploration has been largely focused on the gold potential of the area and a greater portion of the greenstone belt and Junior Lake project remains underexplored.

Figure 1: Junior Lake location relative to the Seymour Project

Figure 1: Junior Lake location relative to the Seymour Project

Junior Lake is host to several LCT pegmatites with three previously identified target areas; Despard, Swole Lake and Tape Lake, all presenting similar geology to Seymour based on the lithium exploration undertaken to date:

The Despard Lithium target

Located approximately 1km north of the east end of North Lamaune Lake, holding exposed outcrop and boulders intermittently over an east-west length of ~914 metres and across widths up to 27 metres, containing up to 30% spodumene. Historic exploration at Despard is limited with a 10 hole diamond drilling program undertaken in 1959 intersecting 1.68% Li2O over 6.1 metres, 1.70% Li2O over 2.01 metres and 1.53% Li2O over 2.74 metres.

Click here for the full ASX Release

This article includes content from Green Technology Metals, licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.