The Conversation (0)

Element 25 Limited (E25 or Company) (ASX: E25; OTCQX: ELMTF) is pleased to provide an update on activities to investigate the potential to recommence operations at the Company’s 100%-owned Butcherbird Manganese Project in Western Australia (Butcherbird) to take advantage of recent upward movement in manganese ore prices caused by market factors including disruptions at South 32 Limited’s Groote Eylandt (GEMCO) operations1. This may include the sale of stockpiles and or recommencing processing of run-of mine (ROM) stockpiles.

HIGHLIGHTS

GEMCO’s Groote Eylandt Mine typically produces more than 6M tonnes of high-grade manganese ore a year, and damage to the mine’s haul road and ship loading facilities from Tropical Cyclone Megan in March 2024 has resulted in a forecast supply disruption of up to twelve months. GEMCO is currently targeting a production restart in Q3 2025.2

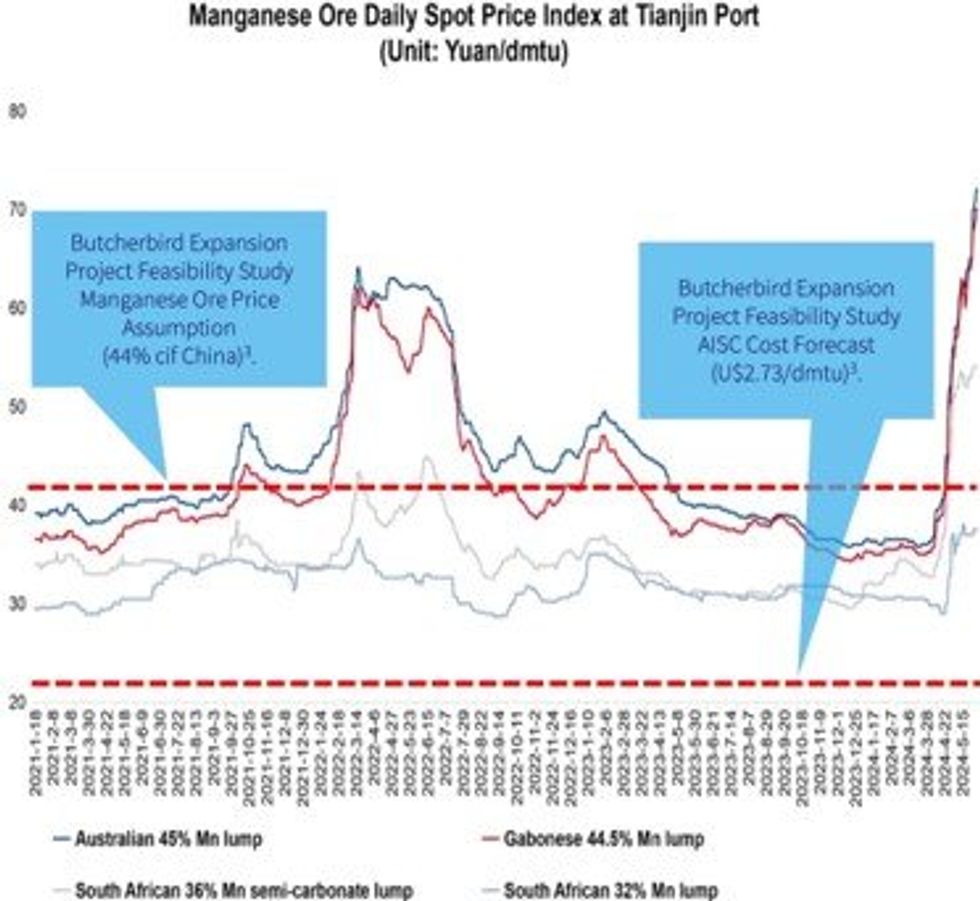

Figure 1: Manganese ore index – Yuan/dmtu Tianjin Port1. Butcherbird Expansion Feasibility Study parameters also shown3.

Figure 1: Manganese ore index – Yuan/dmtu Tianjin Port1. Butcherbird Expansion Feasibility Study parameters also shown3.

The loss of GEMCO supply coupled with political instability in South Africa has resulted in a significant and rapid increase in manganese ore prices due to increased competition for available supply. This presents an opportunity to potentially sell stockpiles that are of a lower grade, preventing their previous sale at lower prices but which may be profitable to ship now.

Additionally, ROM stockpiles that have been mined but not yet processed are available at site. The cost structure of a restart is not currently defined, however E25’s Board recognises the potential opportunity of selling existing product stockpiles and/or recommencing the processing of ROM stockpiles at Butcherbird to produce material for sale at current elevated prices. If viable, these activities will occur in parallel with and will not impact the expansion plans for the Butcherbird Project. E25 suspended Butcherbird production in early 2024 during a period of depressed ore prices while readying for an upgrade of facilities to achieve a nominal 1.1Mpta manganese concentrate production, as outlined in a Feasibility Study completed on January 20243.

The expansion of Butcherbird production aligns with E25’s strategy to produce high-purity manganese sulphate monohydrate (HPMSM) at a facility planned to be built in Louisiana, USA, in partnership with global automakers General Motors LLC and Stellantis NV4.

Element 25 Managing Director Justin Brown said:

“A potential restart of Butcherbird’s processing operations at these increased manganese ore prices on a de-risked basis may be an ideal opportunity to monetise existing stockpiles and generate short-term cashflow. E25 looks forward to updating the market further as these investigations are completed and we will continue to monitor ore markets in the meantime to optimise any potential opportunities that may arise.”

Click here for the full ASX Release

This article includes content from Element 25 Limited, licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.