The Conversation (0)

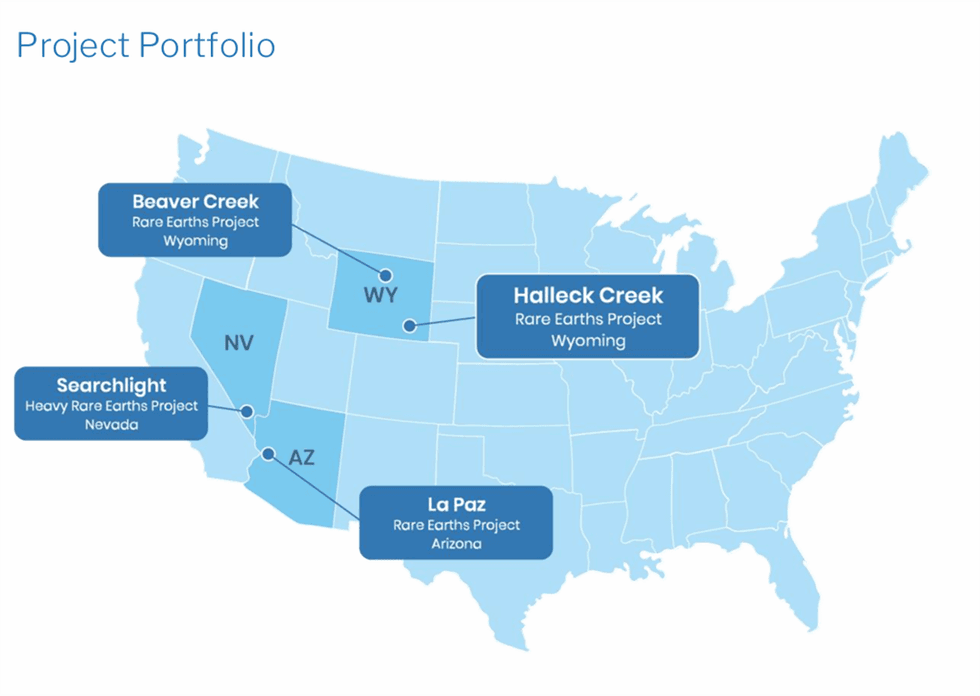

American Rare Earths (ASX:ARR,OTCQX:ARRNF,ADR:AMRRY) unlocks the USA’s rare earths potential through its strategic, high-value asset in Wyoming. The flagship project, Halleck Creek, is one of North America’s largest REE deposits. With a 2.63-billion-ton JORC resource at 3,292 ppm TREO, American Rare Earths is ramping up its development to bolster the North American critical minerals supply chain.

Halleck Creek offers significant exploration upside, presenting a multi-generational opportunity to establish a sustainable rare earths supply chain in the US. The support from EXIM Bank further highlights the strategic importance of Halleck Creek in reducing U.S. dependency on foreign suppliers.

Key Projects

Key ProjectsThe Halleck Creek project in Albany County, Wyoming, is the cornerstone of ARR’s growth strategy. Recognized as one of the largest, rare-earth deposits in North America, it boasts a JORC-compliant resource of 2.63 billion tons at 3,292 ppm TREO. The deposit is hosted in Precambrian granites and metamorphic rocks, which contain REE-enriched minerals like monazite and bastnaesite. The coarse-grained nature of the mineralization ensures cost-effective extraction and processing.

This American Rare Earths profile is part of a paid investor education campaign.*

Click here to connect with American Rare Earths (ASX:ARR) to receive an Investor Presentation