The Conversation (0)

Culpeo Minerals Limited (“Culpeo” or the “Company”) (ASX:CPO, OTCQB:CPORF) is pleased to provide the following activities report for the quarterly period ending 31 March 2023 (the “Quarter”).

HIGHLIGHTS

Lana Corina Copper and Molybdenum Project

Drilling Continues to Intersect Significant Copper Mineralisation

During the Quarter, the Company completed the Phase 2 drilling program at the Lana Corina Copper and Molybdenum Project in Chile (“Lana Corina” or the “Project”).

The Phase 2 drilling program was designed to expand the mineralised footprint at the Project, which remains open in all directions and at depth. The significant results from the Phase 2 drilling program (ASX announcement 16 January 2023) include:

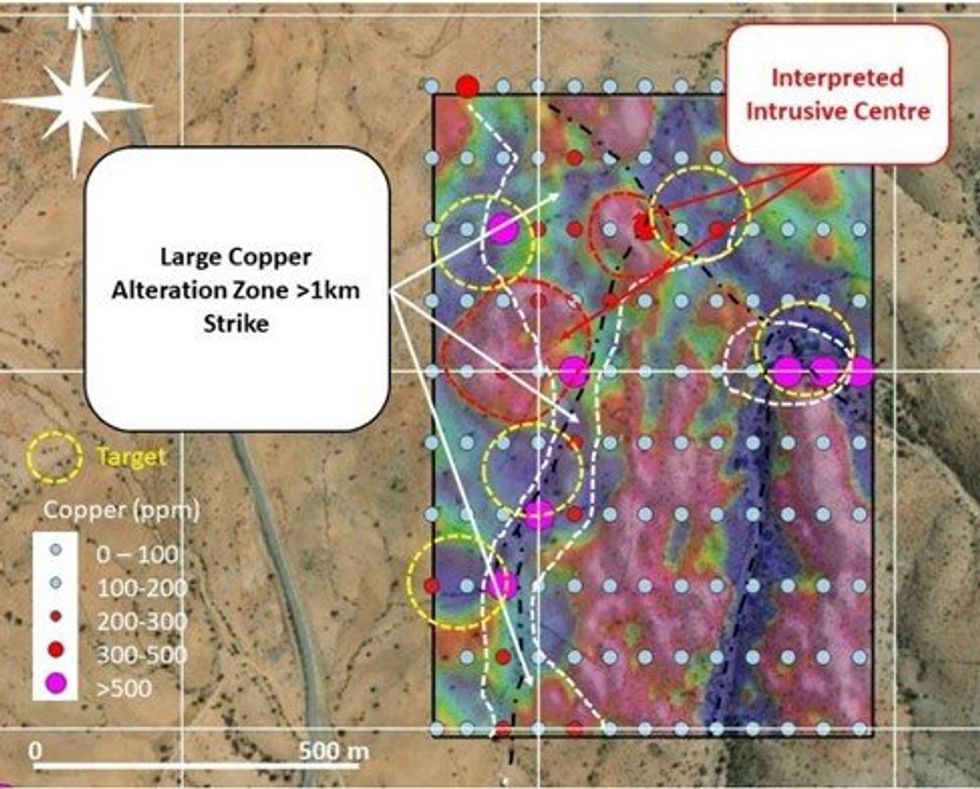

Geochemical Survey Identifies Multiple Surface Targets at Lana Corina

The Company completed a soil geochemical survey at the Vista Montana Prospect within the Lana Corina Project, resulting in the identification of five new high-priority targets within a >3km-long copper alteration zone defined by the geochemistry survey (Figure 1). This increases the overall strike length of the Cu-mineralised trend at Lana Corina to over 3km.

Figure 1: Plan view of the northeast sector, Vista Montana Prospect, of the Lana Corina Project, showing copper mineralisation detected in soil-geochemistry sampling program over a strike distance of >3km.

Figure 1: Plan view of the northeast sector, Vista Montana Prospect, of the Lana Corina Project, showing copper mineralisation detected in soil-geochemistry sampling program over a strike distance of >3km.

The soil geochemistry program was undertaken on a 50m x 100m grid and consisted of 321 samples in total. The results indicate that the overall pattern of the Cu, Cu + Mo, Cu/Mn and alkali elements suggest a copper bearing alteration zone is present at Vista Montana and is over three times the size of the Lana Corina mineralised zone defined from drilling to date (Figure 2).

Click here for the full ASX Release

This article includes content from Culpeo Minerals, licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.