The Conversation (0)

Olympio Metals Limited (ASX:OLY) (Olympio or the Company) is pleased to announce that it has signed an option to acquire 80% of the highly prospective Dufay Cu-Au Project on the Cadillac-Lake Larder Fault Zone, known as the ‘Cadillac Break’ (Dufay Option), in Canada.

Highlights

“The Dufay Project offers Olympio significant strike exposure to one of the world’s premier mineralised structures, the famed Cadillac Break. The Project offers a range of underexplored exploration targets, including high-grade copper showings that have never been drilled and compelling porphyry Cu-Au geophysical targets that remain untested.

“The Project is adjacent to numerous large gold-copper mineral resources, with a major highway through the project directly to the Rouyn-Noranda copper smelter 35km to the east. The Project has significant potential to host porphyry Cu-Au mineralisation, with exploration drilling planned to commence during the upcoming Canadian winter field season.”

This terrane bounding structure is associated with world class endowments of VMS and orogenic gold and copper mineralisation1. The Project is located 35km west of the Rouyn-Noranda mining centre and copper smelter in southwest Québec (Figure 3 and Figure 4).

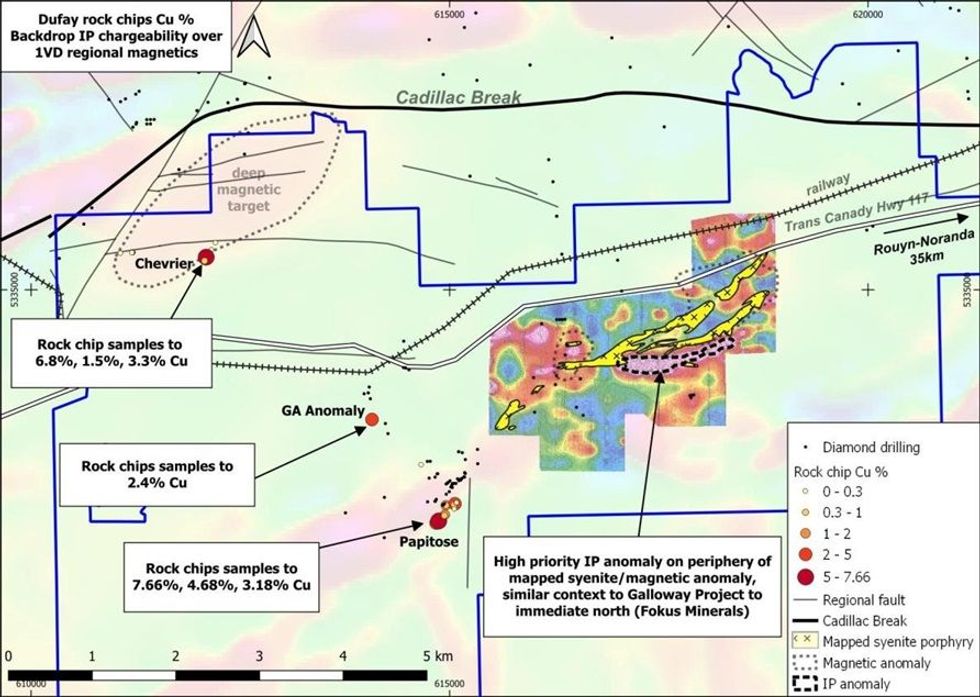

Figure 1 Rock chip sampling and IP geophysical survey over 1VD regional magnetics

Figure 1 Rock chip sampling and IP geophysical survey over 1VD regional magnetics

The Dufay Project contains numerous historical showings of chalcopyrite-rich quartz veining, including the Chevrier working (refer Figure 1 and Figure 2), which was mined briefly in the late 1920s. There has been limited drilling on the Property, with the majority of holes drilled pre-1945 and no drilling for the last 36 years.

Numerous high grade copper rock chips samples across many prospect locations within the tenure, including up to 7.66% at the Papitose Prospect and up to 6.78% at the Chevrier Prospect (Figure 1, Table 1).

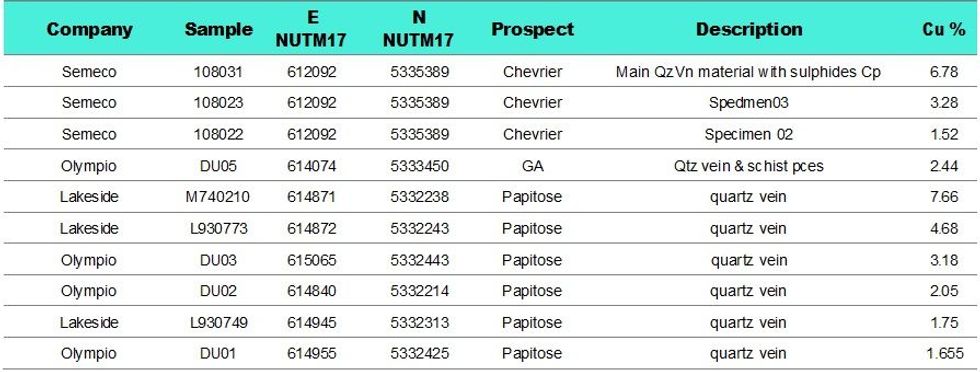

Table 1 Copper results of selected rock chip samples (See Table 2 attached for full summary of sampling)

Table 1 Copper results of selected rock chip samples (See Table 2 attached for full summary of sampling)

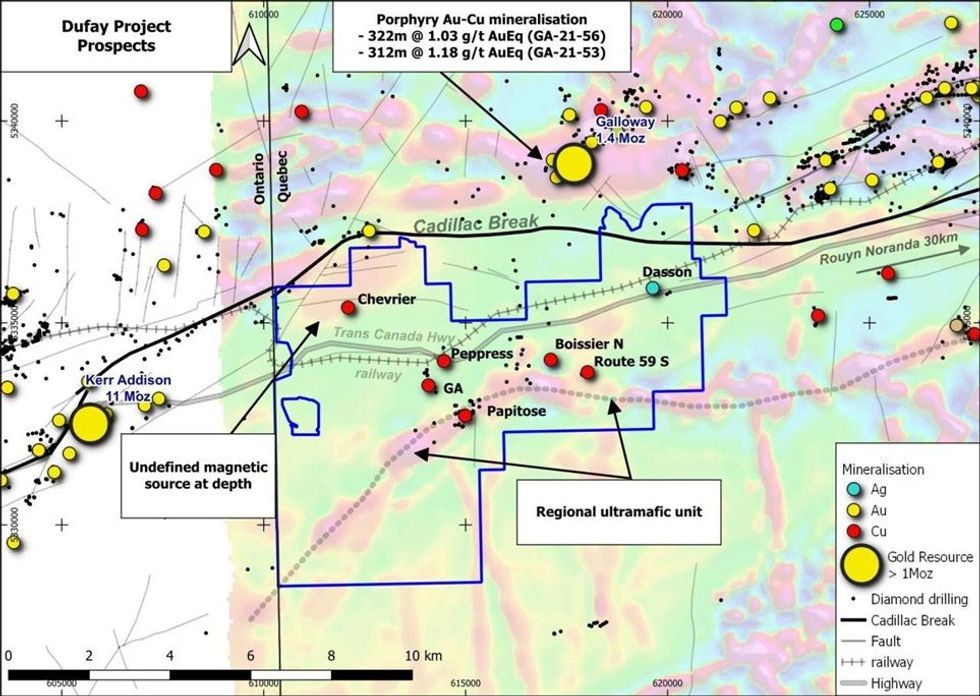

There are numerous elongated exposures of syenite porphyry mapped in the Dufay Project (Figure 1). The Dufay Project syenite occurs <4km south of the Renault Bay Syenite, which is directly associated with the >1.4 Moz Au-equivalent Galloway Project 4km to the north3 (Fokus Minerals) (Figure 2). An Induced Polarisation (IP) ground survey over the area was completed in 20114, and recorded a large (>1200m long), high conductivity anomaly typical of copper sulphide mineralization immediately adjacent to the syenite porphyry. Importantly, this compelling copper target has never been drilled.

The extensive IP anomaly, the Chevrier Prospect and the Papitose Prospect are immediate priority drill targets with the approvals process already underway for drilling planned to start in January 2025.

Figure 2 Dufay Project local mineralisation context. Hendricks drill intercept source5

Figure 2 Dufay Project local mineralisation context. Hendricks drill intercept source5

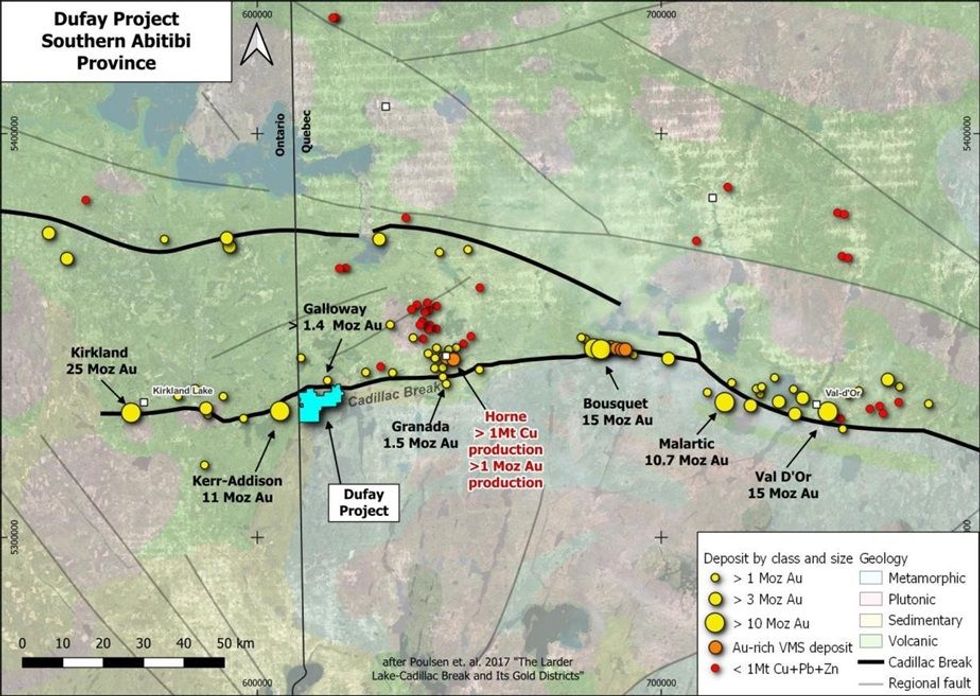

Figure 3 Copper and Gold mineralisation along the Cadillac Break, southern Abitibi Sub-Province

Figure 3 Copper and Gold mineralisation along the Cadillac Break, southern Abitibi Sub-Province

Figure 4 Dufay Project Location

Figure 4 Dufay Project Location

TECHNICAL INFORMATION

The Dufay Copper-Gold Project is located immediately south of the Cadillac-Lake Larder Fault Zone, or the Cadillac Break, a major crustal discontinuity separating the Archean Abitibi Greenstone sub-province to the north from the Pontiac sub-province to the south.

The gold endowment of the orogenic deposits located along the Cadillac Break totals approximately 111 Moz1. Multiple >1Moz gold projects occur within 5km of the Dufay Project , including Kerr-Addison (11 Moz2) and the recently increased Galloway Au-Cu mineral resource (Fokus Minerals, >1.4 Moz Au-equivalent3) (Refer Figure 2 and Figure 3). The Pontiac Sub-Province sediments host numerous gold mineral resources peripheral to the Cadillac Break, including the nearby Granada mineral resource (>1.0Moz)6 and the >10Moz Malartic deposit7.

The Cadillac Break is also linked to the Noranda Volcanic Complex, which hosts numerous VMS deposits (Cu-Au-Zn-Ag) including the Horne deposit (>1Mt Cu, 0.5Mt Ag, 9Moz Au production8; Refer Figure 3).

The Project is highly prospective for porphyry Au-Cu mineralisation and shear-hosted quartz- carbonate-pyrite lode gold mineralisation. The nearby Galloway gold deposit (<4 km to the north, Fokus Minerals) is strongly associated with a syenite intrusive, similar to those mapped within the Dufay tenure.

Dufay hosts numerous quartz vein-sulphide hosted copper-gold-silver prospects with strike extents to hundreds of metres. The Archaean host geology includes a wide variety of rock types, including metasediments, ultramafic talc-chlorite schists, porphyry/syenite, felsic to intermediate intrusives and gneisses, and Proterozoic dolerite dykes. Disseminated chalcopyrite mineralisation is widespread in selected areas examined by Olympio to-date, suggestive of a large pervasive mineralising system.

Click here for the full ASX Release

This article includes content from Olympio Metals Limited, licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.