The Conversation (0)

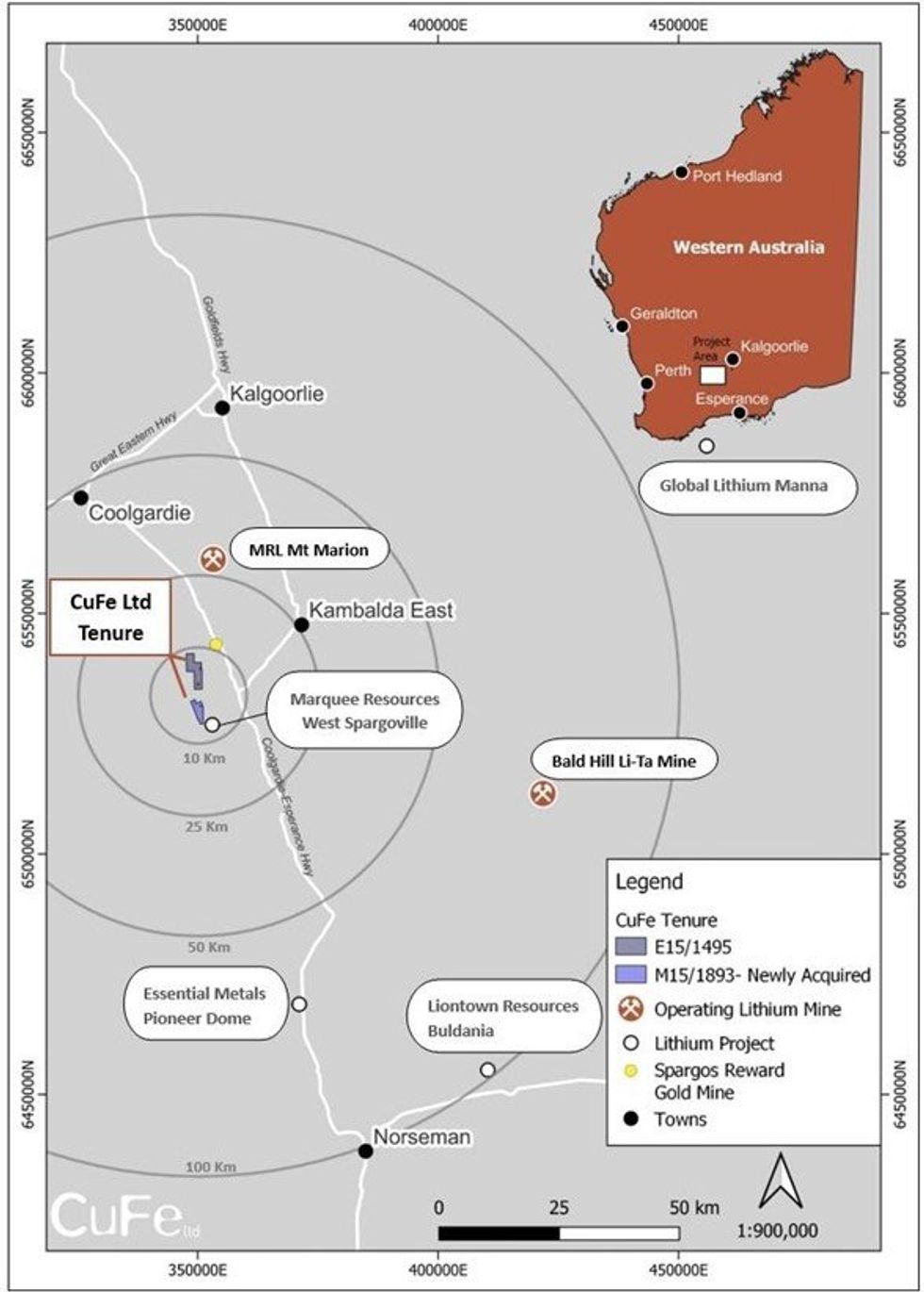

CuFe Ltd (ASX: CUF) (CuFe or the Company) is pleased to advise it has entered an agreement to acquire rights to lithium and rare earth related minerals over M15/1893, covering approximately 7.4km2 of ground, located 30km south of Mineral Resources Mt Marion Mine.

HIGHLIGHTS

Under the terms of the agreement, CuFe acquires rights to lithium and rare earth related minerals over M15/1893 (a mining lease which is presently under application pending finalisation of native title negotiations) from Rosa Management Pty Ltd (“Rosa”), and in return CuFe assigns Rosa rights to gold on the recently acquired E15/1495. The parties each assume the obligations to pay a $300,000 milestone payment payable to the previous owner in the event production occurs in the future from the tenure and a 1% gross sales royalty. Completion of the transaction is expected occur within 30 days.

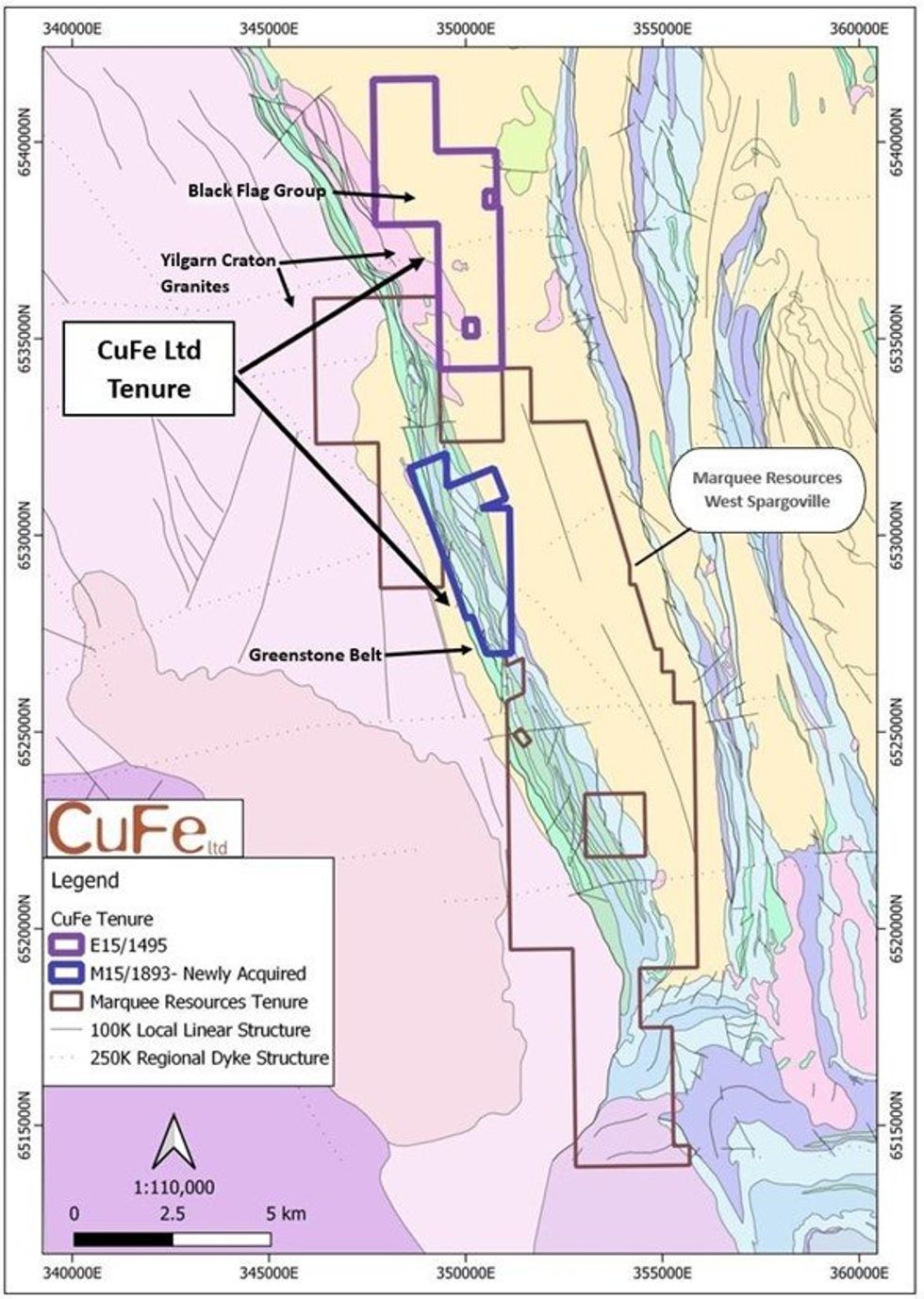

The local geology comprises mafic and ultramafic intrusive within felsic volcanics and siliciclastics of the Black Flag Group and is characterised by NNW trending networks of pegmatites (see Figure 2).

Initial visits to the site have occurred, with more detailed field work including detailed mapping and rock chip sampling planned across both tenements over the next 2-3 weeks.

CuFe Executive Director, Mark Hancock, commented “We are pleased to secure these rights in a commonsense way that enables each company to focus on their commodities of choice and maximise use of the ground. There is a lot of activity in the region, as illustrated by the recent acceleration of Mineral Resources farmin to the Marquee Resources tenure which surrounds our ground so that encourages us that we are in the right region. We look forward to the outcome and results of the planned field work across this tenement package.”

Released with the authority of the CuFe Board.

Figure 1 – Tenement Location and Regional Overview

Figure 1 – Tenement Location and Regional Overview

Figure 2 – Regional Geology and Tenement overview.

Figure 2 – Regional Geology and Tenement overview.

Click here for the full ASX Release

This article includes content from CUFE LTD, licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.