The Conversation (0)

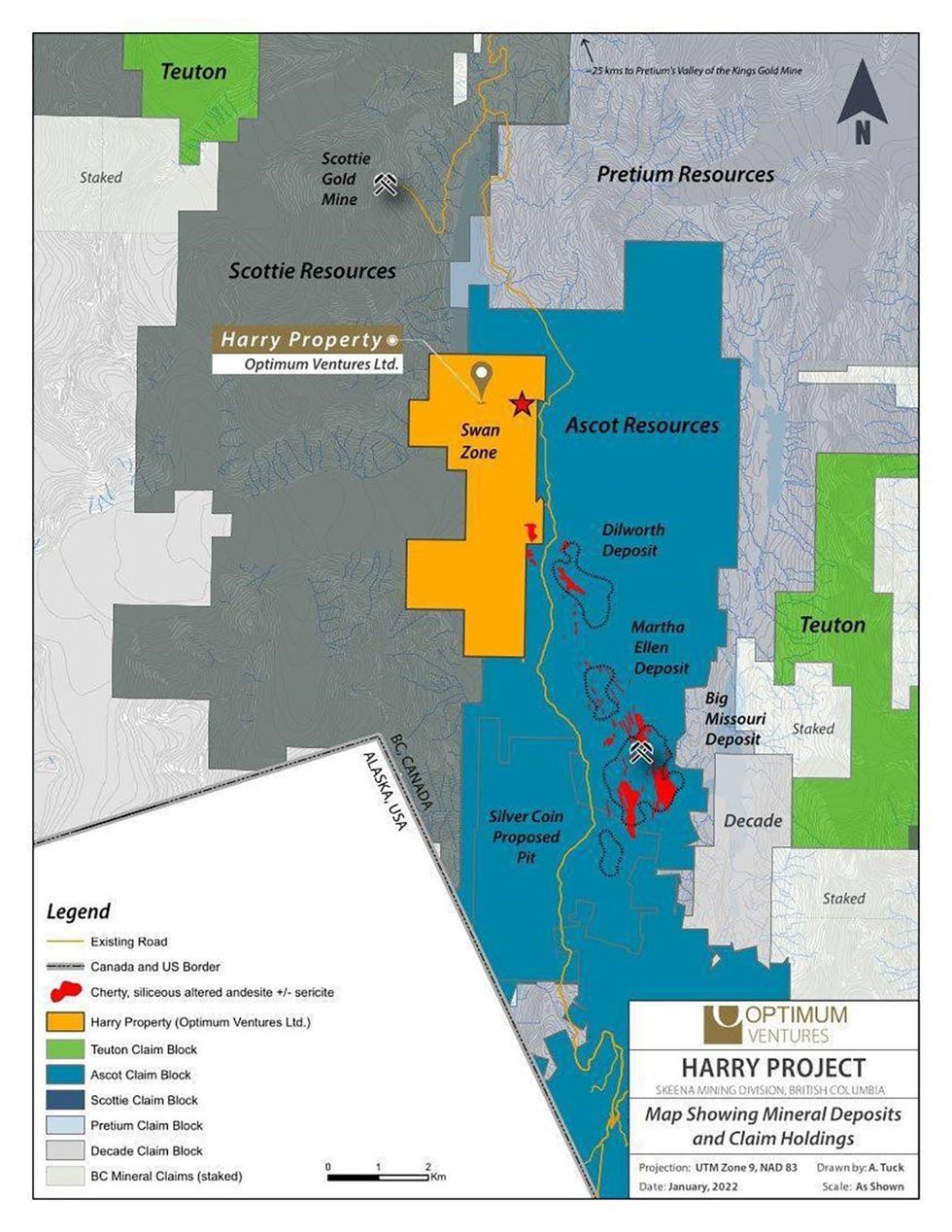

Optimum Ventures (TSXV:OPV, Frankfurt:41Q, OTC:OPVLF) focuses on its high-grade gold asset in the prolific Golden Triangle. The company’s flagship asset, the Harry property, is located between two large mineralized systems: sulphurets hydrothermal system (SHS) and premiere hydrothermal system. An experienced management team and board of directors lead Optimum Ventures toward bringing the asset to production.

The Harry property has surface samples with high-grade assays reaching upwards of 285.4 g/t gold and 1,949 g/t silver. An exploratory drill program at the property was recently completed by the company in 2022. Two notable drill holes produced up to 3.10 g/t gold, 690.1 g/t silver, and an additional 1,833 g/t silver equivalents.

Company Highlights

- Optimum Ventures is an exploration and development mining company focusing on its high-grade gold asset within the famed Golden Triangle in British Columbia.

- The Golden Triangle is globally recognized as one of the most prolific gold-producing regions in the world.

- The company’s flagship Harry property is ideally located between two major mineralized systems and has already produced high-grade gold and silver assays, including up to 3.10 g/t gold, 690.1 g/t silver, and an additional 1,833 g/t silver equivalents.

- Optimum Ventures has an option agreement with Teuton to acquire an 80 percent interest in the property and enter into a JV agreement.

- An experienced management team led by Andy Bowering, who was instrumental in numerous discoveries including the Silver Coin deposit with Ascot Resources (TSX:AOT)

This Optimum Ventures profile is part of a paid investor education campaign.*

OPV:CA