The Conversation (0)

Magna Mining Inc (TSXV: NICU) (the "Company") is pleased to announce that it has commissioned a second drill rig to accelerate exploration drilling at previously identified regional targets on the Shakespeare Nickel Project. The second rig was moved to site early this month, and recently began drilling at the Company's Spanish River Mine Option ("Spanish River"), located 1km south-west of the recent P-4 nickel discovery (see Fig. 1). Spanish River was previously in production as an underground Cu-Co-Au-Ag operation until 1970, and the current drill program is the first diamond drilling program since the mine closed.

The first drill rig of the 2022 drill program started in January and is currently drilling the P-4 Nickel target, which was discovered during the 2021 regional exploration drill program (see News Release). This drill is planning to complete an initial 2500m of drilling to further test the EM plate associated with the discovery hole, as well as the prospective trend of over 400m of strike length to the east. The Company expects this drilling to be completed in early April, with assay results coming out later that month. Magna is planning to complete 10,000m of drilling in 2022, with 5500 m still to be allocated based on results from the winter drilling program.

UPDATES ON THE EVALUATION OF NEAR-TERM NICKEL PRODUCTION VIA TOLL MILLING

Ongoing discussions with Sudbury mill owners have been positive, and Magna has decided to accelerate the evaluation of the toll milling of Shakespeare ore to better understand the potential economics. Once the current drilling is completed at Spanish River (within 2-3 weeks), the second rig will be prioritized to extract representative metallurgical core samples from the Shakespeare deposit. These samples will be used to determine the recoveries and payable terms from mills in the region, which will support the evaluation of the near-term restart of toll milling. The Shakespeare Mine was previously in commercial production from 2010 to 2012 via toll milling, and a total of approximately 490,000 tonnes of ore was sent to the Strathcona Mill in Sudbury for processing.

Magna Mining CEO Jason Jessup commented: "Given the recent moves in nickel and copper prices, we have decided to accelerate the studies associated with restarting production via toll milling. Nickel, copper and palladium prices have seen record highs recently and there is potentially a healthy margin associated with the near-term production of Shakespeare ore through a third-party mill. Given that major permits for production remain in place, we feel Magna is uniquely positioned to take advantage of the current metal price environment. We remain focused on our three pillars of growth: development of the Shakespeare open pit mine, mill and tailing facility, resource growth through exploration and executing accretive acquisitions of Sudbury nickel projects that have synergies with Shakespeare. The potential cash flows from toll milling could contribute meaningfully to all three of these growth initiatives."

ABOUT THE SPANISH RIVER MINE OPTION

Magna has an option to acquire 100% of the past-producing Spanish River Mine over a three-year term comprising exploration expenditures, cash and share payments. Once the option terms have been satisfied, the vendor will retain a 1.5% NSR royalty which 0.75% (50%) can be purchased by Magna for $1,000,000. Spanish River is adjacent to Magna's 100% owned Shakespeare Project, located approximately 5 km from the Shakespeare Mine and has potential to be an additional source of feed for a future Shakespeare mill.

Figure 1: Spanish River exploration target showing lithologies and the deformation corridor

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/8002/117440_36db8e64e4dcfbe8_002full.jpg

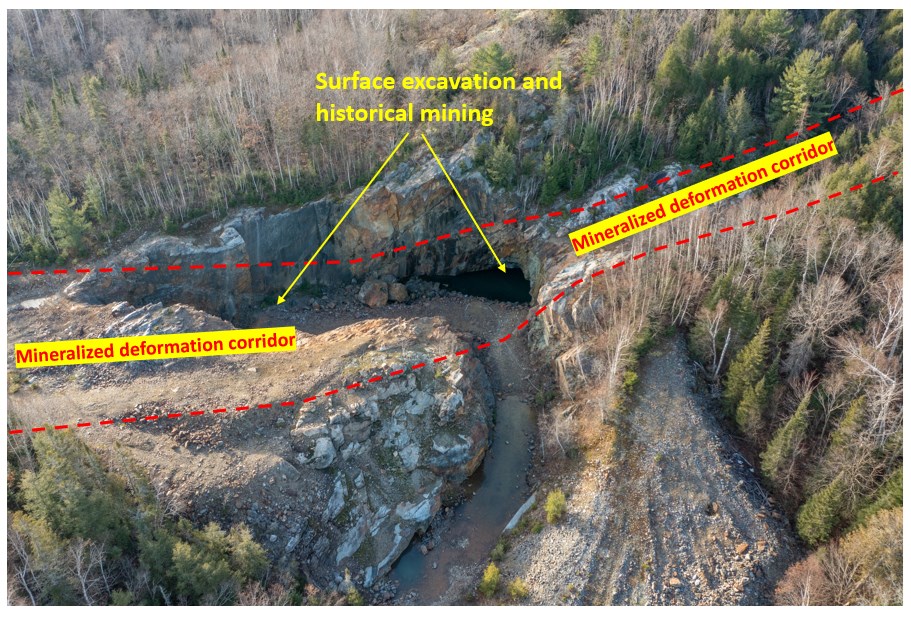

Image 1: Mineralized deformation corridor and surface excavation from past producing Spanish River underground mine, located 1km south-west of Magna Mining's P-4 nickel discovery

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/8002/117440_36db8e64e4dcfbe8_003full.jpg

Qualified Person

The technical information in this press release has been reviewed and approved by Mynyr Hoxha, Ph.D., P.Geo., the Company's Vice President of Exploration. Dr. Hoxha is a qualified person under Canadian National Instrument 43-101.

About Magna Mining Inc.

Magna Mining is an exploration and development company focused on nickel, copper and PGM projects in the Sudbury Region of Ontario, Canada. The Company's flagship asset is the past producing Shakespeare Mine which has major permits for the construction of a 4,500 tonnes per day open pit mine, processing plant and tailings storage facility and is surrounded by a contiguous 180km2 prospective land package. Additional information about the Company is available on SEDAR (www.sedar.com) and on the Company's website (www.magnamining.com).

For further information, please contact:

Jason Jessup

Chief Executive Officer

or

Paul Fowler, CFA

Senior Vice President

Email: info@magnamining.com

Cautionary Statement

This press release contains certain forward-looking information or forward-looking statements as defined in applicable securities laws. Forward-looking statements are not historical facts and are subject to several risks and uncertainties beyond the Company's control, including statements regarding the production at the Shakespeare Mine, the economic and operational potential of the Shakespeare Mine, potential acquisitions, plans to complete exploration programs, potential mineralization, exploration results and statements regarding beliefs, plans, expectations, or intentions of the Company. Resource exploration and development is highly speculative, characterized by several significant risks, which even a combination of careful evaluation, experience and knowledge may not eliminate. All forward-looking statements herein are qualified by this cautionary statement. Accordingly, readers should not place undue reliance on forward-looking statements. The Company undertakes no obligation to update publicly or otherwise revise any forward-looking statements whether as a result of new information or future events or otherwise, except as may be required by law.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accept responsibility for the adequacy or accuracy of this press release.

To view the source version of this press release, please visit https://www.newsfilecorp.com/release/117440

News Provided by Newsfile via QuoteMedia