The Conversation (0)

High-Tech Metals Limited (ASX: HTM) (High-Tech, HTM or the Company), a critical battery minerals exploration Company, is pleased to provide the following report on its activities for the Quarter ending 30 September 2024 (“Quarter”). The Company’s primary activities during the quarter were the desktop review of Werner Lake Project, Canada, (“Werner Lake”).

HIGHLIGHTS

Sonu Cheema, Executive Director, commented:

"It is a pleasure to update the market on quarterly activities of High-Tech’s, specifically the Werner Lake cobalt, nickel, and PGE Project. Over the last 18 months High-Tech has generated significant data from the successful sampling and drilling programs. Through the compilation of the available historical data and the data derived from our successful exploration, I believe we will unlock the true value of Werner Lake.”

Desktop Review – Werner Lake

HTM commenced a desktop review of Werner Lake in the previous quarter aimed at delineating future exploration programs based on all available historical data and newly acquired data. The data derived from the successful Drilling Program, which focused on high priority drill targets, adds to the extensive data available on Werner Lake (refer ASX announcement – Drilling Results at Werner Lake – released 27 November 2023).

High-Tech’s Exploration at Werner Lake

From the outset of the 2023 campaign, focus was on testing new targets away from the Werner Lake deposit. Two areas were selected for a comprehensive evaluation and assessment of the potential to locate economic cobalt, nickel, and PGE targets. These are shown below, essentially, the ‘East’ and ‘West’ blocks or grids.

The objective was to test cobalt, copper and nickel targets on a portion of the Werner Lake Property. The drill program was planned and carried out by the in-country geological consultants, Apex Geoservice (APEX). The program was completed on time and under budget.

Targets were based on a comprehensive appraisal and evaluation of historical geological and production data covering exploration and production on and around the Property, and on the somewhat limited geological and production data from the Gordon Lake Cu-Ni mine.

Table 1 – Total of 798 metres of NQ core was drilled over six holes.

Table 1 – Total of 798 metres of NQ core was drilled over six holes.

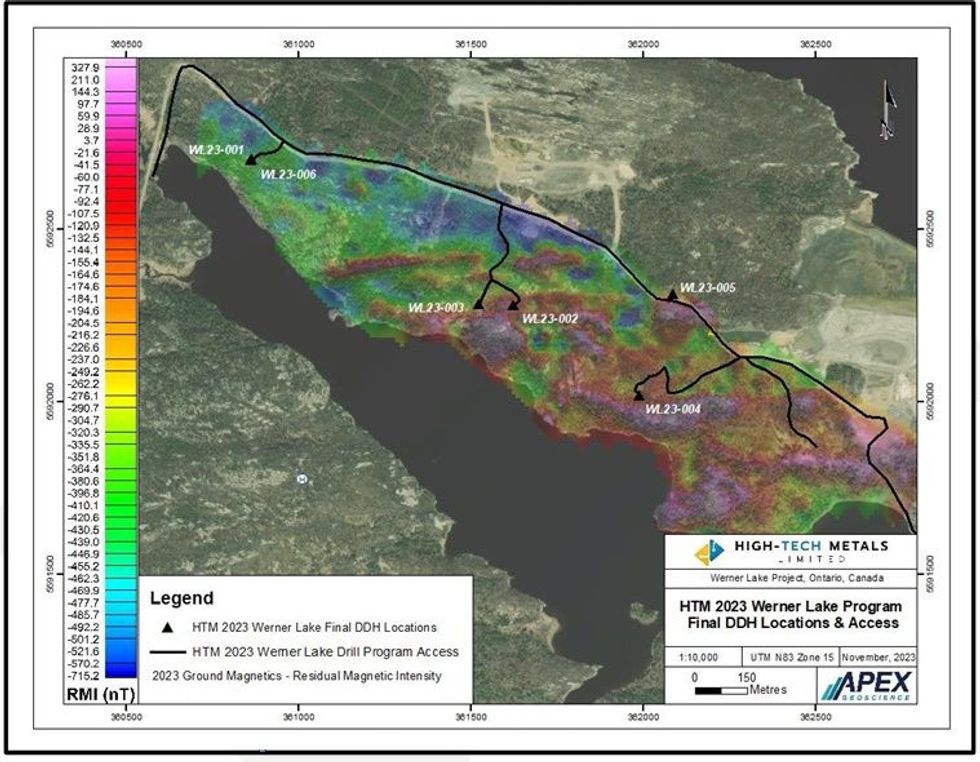

Figure 1 – Werner Lake final DDH locations and access.

Figure 1 – Werner Lake final DDH locations and access.

The results from the ground-based magnetometer survey, lithogeochemical sampling, and prospecting provided additional focus with the primary targets all located on the east block, east of Gordon Lake and the Gordon Lake mine (refer ASX announcement – WERNER LAKE SAMPLING DISCOVER HIGH GRADE Ni SULPHIDE & Cu-Co – released 30 August 2023).

Click here for the full ASX Release

This article includes content from High-Tech Metals, licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.