The Conversation (0)

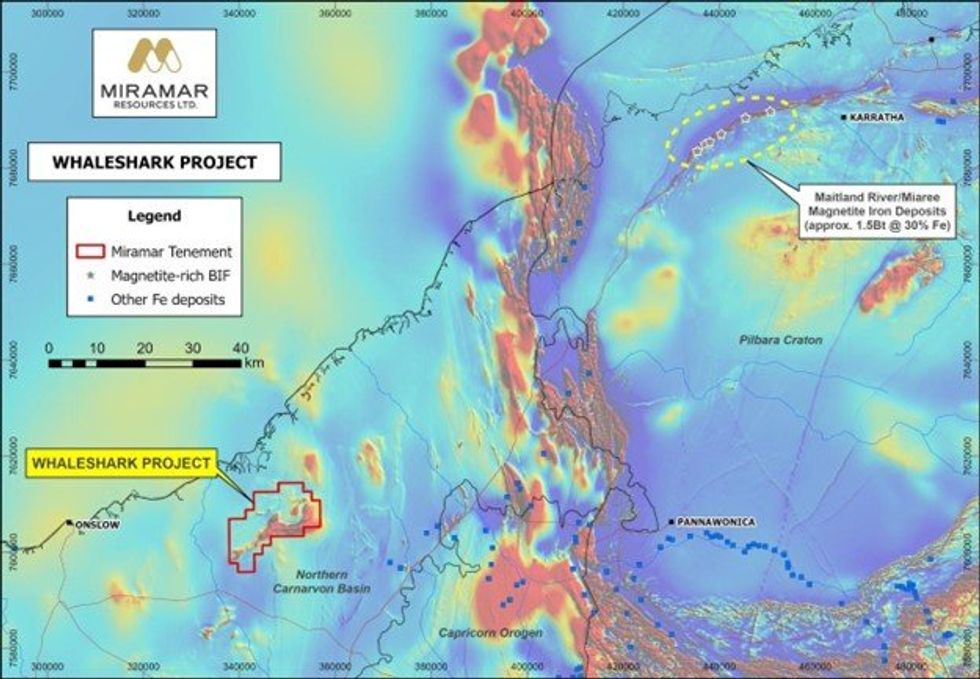

Miramar Resources Limited (ASX:M2R, “Miramar” or “the Company”) advises that a review of historical drilling data has revealed potentially very significant magnetite iron opportunities at the Company’s 100%- owned Whaleshark Project in the Ashburton Region of WA (Figure 1).

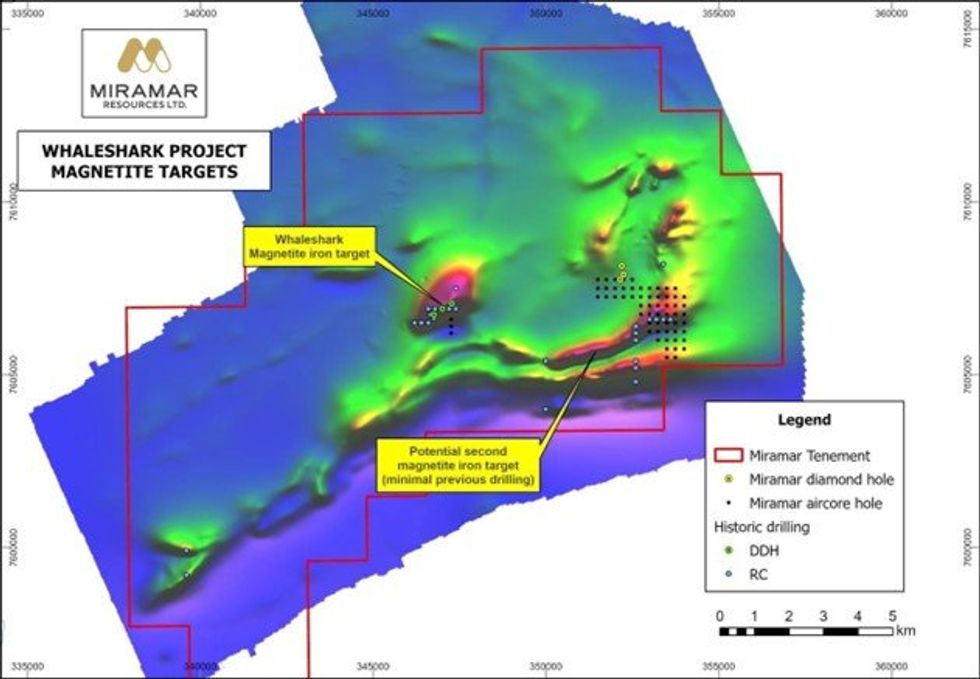

Drilling conducted at Whaleshark by Western Mining Corporation (WMC) in the 1990’s, whilst exploring for iron oxide copper-gold, intersected significant widths of magnetite-rich banded iron formation averaging >25% Fe beneath younger sediments, with several holes ending in mineralisation (Figures 2 and 3). Miramar recently re-examined those holes, following completion of its own diamond drilling campaign.

Miramar’s Executive Chairman, Mr Allan Kelly, said the magnetic anomalies seen at Whaleshark are similar in scale to the 1.5 billion tonne Maitland River and Miaree magnetite iron deposits1.

“The recognition of two potentially very large magnetite iron deposits is very significant for Miramar, especially given the location of the Whaleshark Project with respect to existing infrastructure,” he added.

Figure 1. Regional magnetic image showing Whaleshark Project in relation to the Maitland River and Miaree magnetite iron deposits.

Figure 1. Regional magnetic image showing Whaleshark Project in relation to the Maitland River and Miaree magnetite iron deposits.

Figure 2. Magnetic image of Whaleshark Project showing magnetite iron targets.

Figure 2. Magnetic image of Whaleshark Project showing magnetite iron targets.

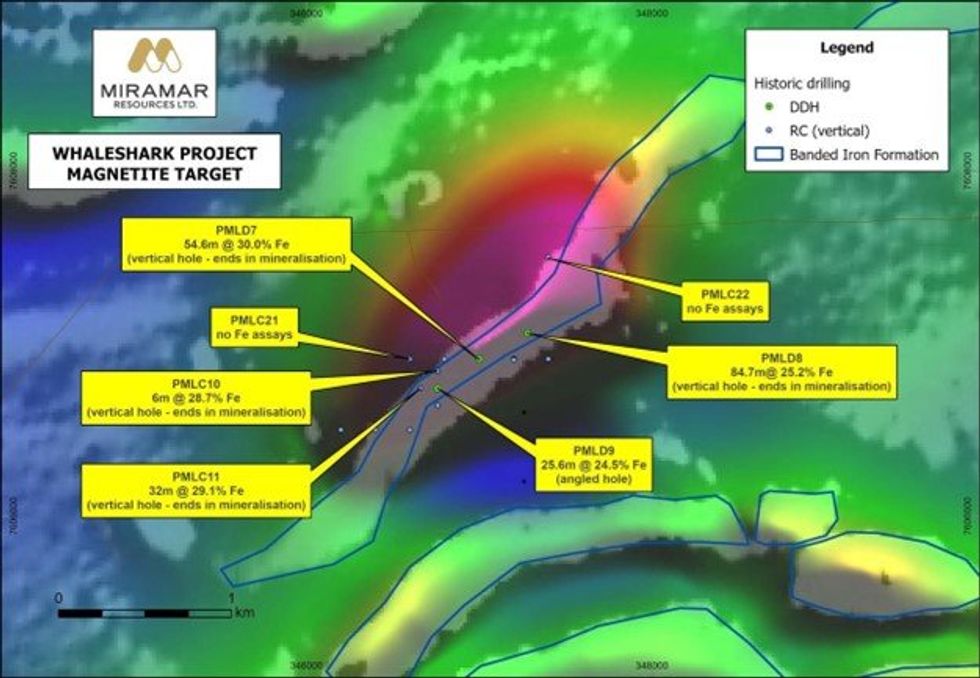

Figure 3. Magnetic image (RTP/2VD) of Whaleshark magnetite target showing historic drilling results.

Figure 3. Magnetic image (RTP/2VD) of Whaleshark magnetite target showing historic drilling results.

A larger and virtually untested magnetite target is observed on the southern side of the granodiorite pluton.

Drill testing of the second magnetic anomaly is limited, with only a handful of historic RC holes that were not assayed for iron, and recent aircore holes completed by Miramar in 2022 that ended in 18-32% Fe.

In general, the basement is significantly shallower within this target, with average cover thickness in the order of 25-30m.

Click here for the full ASX Release

This article includes content from Miramar Resources Limited, licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.