The Conversation (0)

High-Tech Metals Limited (ASX: HTM) (High-Tech, HTM or the Company), a critical battery minerals exploration Company, is pleased to provide the following report on its activities for the quarter ending 31 March 2024. The Company’s primary activities during the quarter were the planning of exploration of the Ketele LCTG Project in Ethiopia.

HIGHLIGHTS

Ketele LCT Project

During the quarter, HTM announced that the Company was planning its initial exploration program at the Company’s Ketele Exploration License (MOM-EL-05096-2023) (“License”) in Ethiopia (Refer ASX Announcement - HTM to Progress Exploration Sampling at Ketele LCT Project – dated 10 January 2024). The License will be the foundation of our exciting new Ketele LCT Project (“Ketele” or the “Project”).

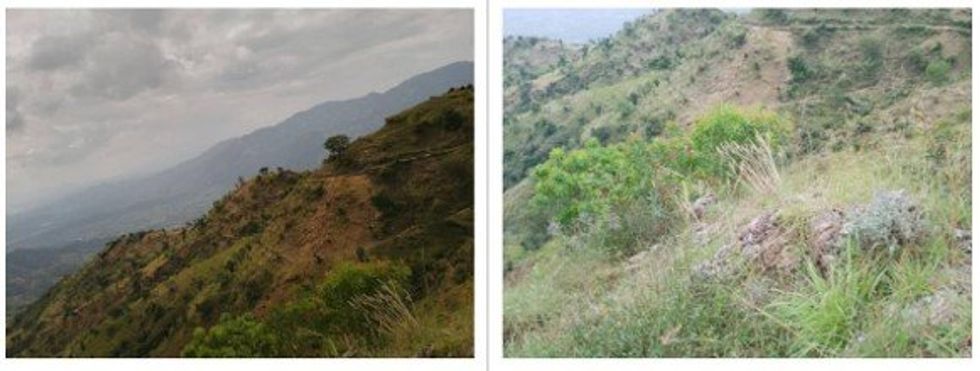

This initial program will comprise sampling of prospective geological units (inc. granites, pegmatites, etc) and regional structures which have previously been identified and mapped in this underexplored area of Ethiopia (Figure 1). This sampling will include rock chip sampling and channel samples, the latter yielding continuous samples across an entire outcrop. The planning process with regard to certain Project area access and exploration program approvals is ongoing.

Figure 1 – Example of previously identified outcrops for the planned rock and channel sampling at the Ketele LCT Project.

Figure 1 – Example of previously identified outcrops for the planned rock and channel sampling at the Ketele LCT Project.

Figure 2 – Ketele LCT Project Location.

Figure 2 – Ketele LCT Project Location.

Werner Lake Project

Following on from HTM’s successful drill program at Werner Lake Project (“Werner Lake”) (Refer to ASX Announcement - Drilling Results at Werner Lake Project – 27 November 2023), the Company continues to evaluate the next steps to realise the value of the asset.

Business Development

During the quarter, HTM considered several project opportunities. HTM will continue to identify and review projects which complement the Company’s existing assets and support its strategy of building a portfolio of exploration, development, and operating mining assets.

Click here for the full ASX Release

This article includes content from High-Tech Metals, licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.