The Conversation (0)

High-Tech Metals Limited (ASX: HTM) (High-Tech, HTM or the Company) is pleased to announce it has entered into an agreement to acquire the Norpax Deposit (Norpax) and acquired an option to purchase the Reynar Lake Project (Reynar Lake) (Together, the Projects) which are both located in Ontario, Canada. The Projects are directly west and adjoin the Company’s existing project, Werner Lake Project (Werner Lake, or the Project), located in northwestern Ontario.

HIGHLIGHTS

The Company has significantly increased its exposure to nickel sulphides and copper through the following acquisition and option agreement:

Norpax Nickel Sulphide Deposit:

Reynar Lake Ni-Cu-Co Project:

The Company plans to build on the recent exploration success at Werner Lake by immediately begin planning exploration on the newly acquired Projects.

The acquisition of the Projects increases HTM’s landholding in the Werner Lake Area and the Company’s exposure to battery metals such as copper, cobalt, and nickel.

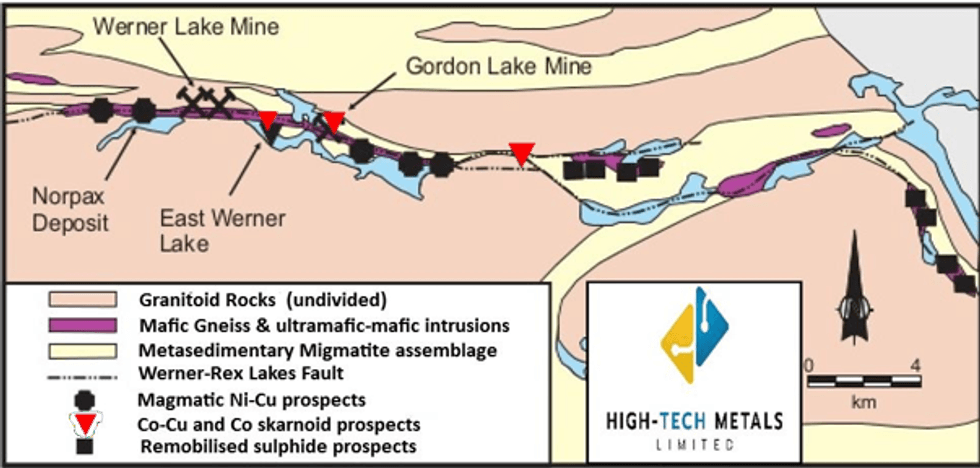

Figure 1 – Location of Mineral Deposits in the Werner Lake Belt.

Figure 1 – Location of Mineral Deposits in the Werner Lake Belt.

Sonu Cheema, Executive Director commented:

"We are excited by the acquisition of Norpax and the option over Reynar Lake with the potential for a nickel discovery in a historic nickel producing province of Canada. Not only do the acquisitions increase our exposure to nickel, but it also increases the Company’s land holding substantially making High-Tech one of the largest land holders in the area.

“As the Projects lay in the area of Werner Lake, the Company’s geological team are familiar with the geological setting. This has been recently proven by the Company’s discovery of high-grade samples of nickel sulphide (that exceeded assay detection limits) in the Werner Lake Project.

“The Company plans to utilise its expertise in the area by undertaking a review of all available geological data, performing a systematic geochemical sampling program of known mineral occurrences on the projects in conjunction with reconnaissance geological mapping and relog and assay all known and available core.”

Click here for the full ASX Release

This article includes content from High-Tech Metals, licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.