The Conversation (0)

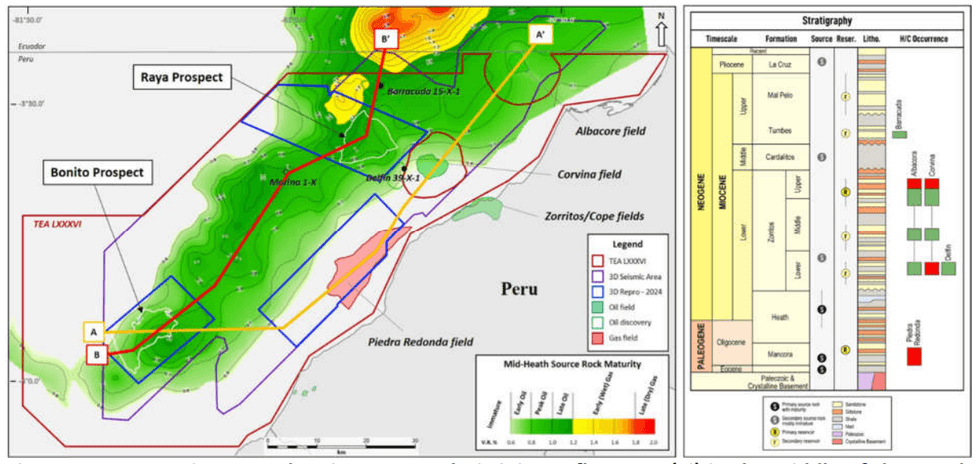

Condor Energy Ltd (ASX: CND) (Condor or the Company) is pleased to provide an update on exploration progress at its Technical Evaluation Agreement (TEA) offshore Peru where two large oil prospects (Raya and Bonito) have already been identified and regional mapping shows that the primary source rock interval, the Oligocene/Miocene aged Heath Formation, is mature for oil generation over much of the TEA area.

Figure 1 – Maturation map showing expected Vitrinite Reflectance (%) in the middle of the Heath Formation. The peak oil generation zone corresponds to a range in vitrinite reflectance between 0.8 and 1.2% shown in green.

Figure 1 – Maturation map showing expected Vitrinite Reflectance (%) in the middle of the Heath Formation. The peak oil generation zone corresponds to a range in vitrinite reflectance between 0.8 and 1.2% shown in green.

The Raya and Bonito prospects are large features in the Zorritos Formation, which present structural closure at multiple levels and the potential for stacked pay with multiple Zorritos reservoir-seal pairs present.

Based on analysis of surface outcrops, cuttings and core samples from previous wells published by Perupetro (the Peruvian national oil regulator), there are numerous potential source rock intervals in the Tumbes Basin.

The Company recently completed an interpretation of the wider regional seismic data which mapped key intervals and confirmed that the Heath Formation (Figure 1) and Mancora Formation likely sit within the maturity window for oil and gas generation respectively.

Click here for the full ASX Release

This article includes content from Condor Energy, licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.