The Conversation (0)

Condor Energy Limited (ASX: CND) (Condor or the Company) is pleased to provide the following report on exploration activities for the quarter ending 30 September 2024.

Highlights

During the reporting quarter, Condor and US-based joint venture partner Jaguar Exploration Limited (Jaguar), continued the evaluation of the 4,858km2 Technical Evaluation Agreement (TEA or block) offshore Peru in conjunction with the Company’s technical advisors Havoc Services Pty Ltd (Havoc).

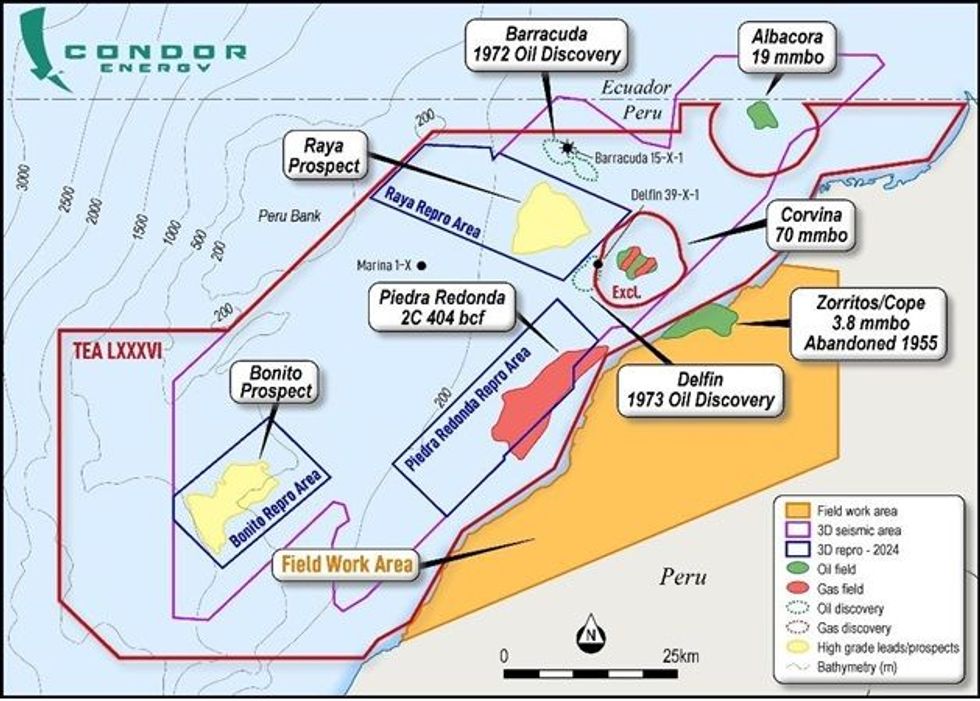

Condor’s block comprises over 3,800km2 of existing 3D seismic data from which an aggregate of 1,000km2 have been selected to undergo pre-stack depth migration (PSDM) reprocessing and interpretation across three discrete highly prospective areas (Figure 1). The three areas selected for reprocessing were chosen following the identification of the Raya and Bonito prospects and the Piedra Redonda gas field.

Figure 1 – TEA Prospects and 3D Seismic areas selected for reprocessing.

Figure 1 – TEA Prospects and 3D Seismic areas selected for reprocessing.

The Raya1 and Bonito2 prospects are large features in the Zorritos Formation, which present structural closure at multiple levels and the potential for stacked pay with multiple Zorritos reservoir-seal pairs present. The Piedra Redonda gas field contains ‘Best Estimate’ Contingent Resources (2C) of 404 Bcf (100% gross)3 which potentially underpins a standalone gas development and additional low-risk upside located updip from the C-18X discovery well with ‘Best Estimate’ Prospective Resources (2U) of 2.2 Tcf# (gross unrisked) of natural gas4.

Click here for the full ASX Release

This article includes content from Condor Energy, licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.