The Conversation (0)

Platreef ranks as world's largest precious metals deposit under development

Phase 1 mine in construction, advancing towards first production in Q3 2024

2022 Feasibility Study yields an after-tax NPV8% of US$1.7 billion and IRR of 18.5% at long-term consensus metal prices

After-tax NPV8% of US$4.1 billion and IRR of 29.3% at current spot metal prices

Shaft 2 accelerated to 2027, advancing Phase 2 expansion with annual forecast production of greater than 590,000 ounces of palladium, platinum, rhodium, gold and more than 40 million pounds of nickel and copper

2022 Feasibility Study confirms Platreef's potential to be the industry's largest and lowest-cost primary PGM producer

Fort Lauderdale, Florida--(Newsfile Corp. - February 28, 2022) - Ivanhoe Mines (TSX: IVN) (OTCQX: IVPAF) Co-Chair Robert Friedland announced today at the 31st BMO Global Metals & Mining Conference that the company's South African subsidiary, Ivanplats, and its partners, welcome the outstanding positive findings of an independent Platreef 2022 Feasibility Study for the tier-one Platreef palladium, rhodium, nickel, platinum, copper and gold project in South Africa.

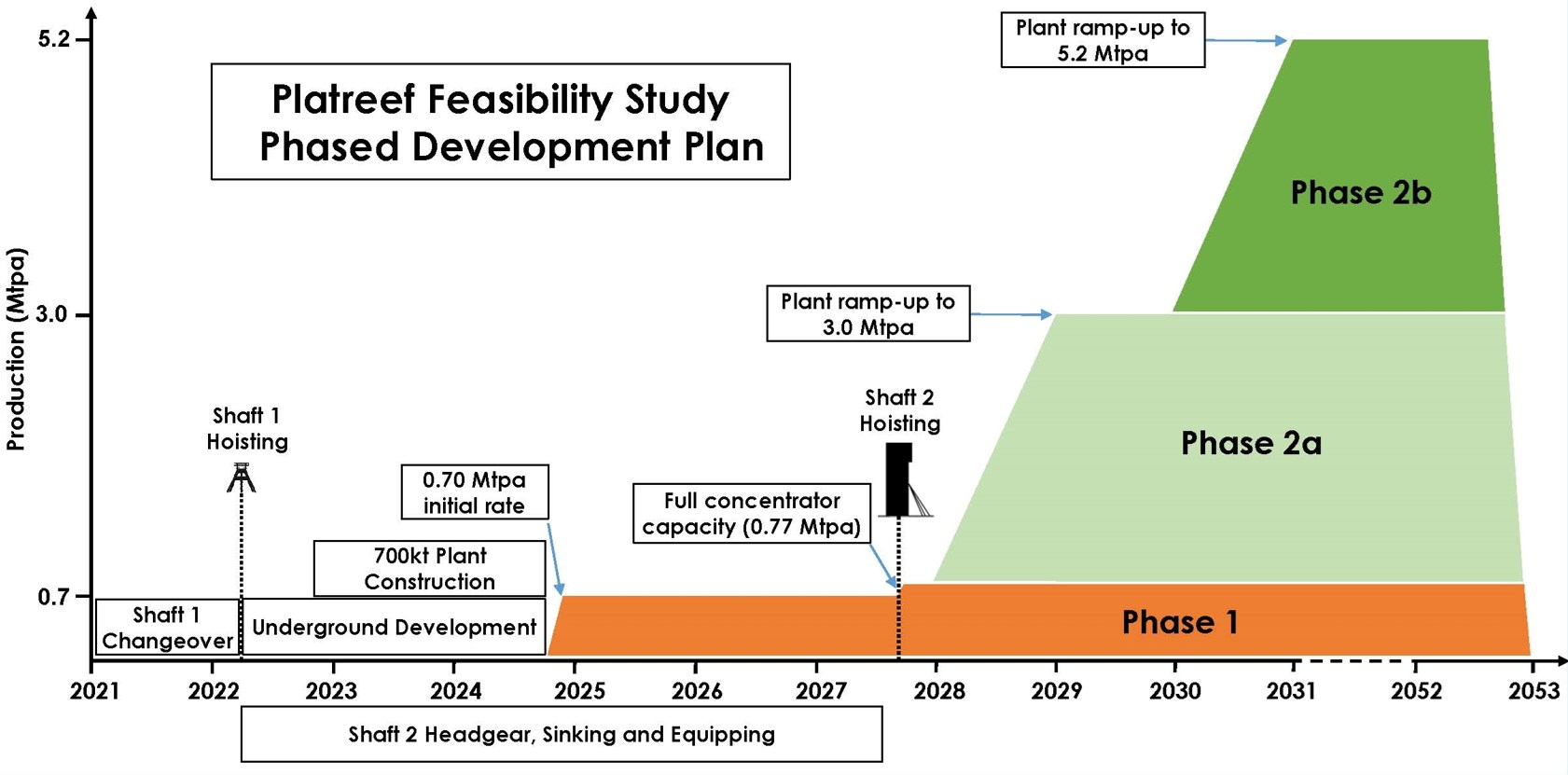

The 2022 Feasibility Study provides the blueprint for the ongoing development of Platreef and builds on the excellent results of the preliminary economic assessment (PEA) for a phased-development scenario to expedite production, announced in November 2020, alongside the 2020 Feasibility Study. The Platreef 2022 Feasibility Study is based on a steady state production rate of 5.2 million tonnes per annum (Mtpa), as well as an accelerated ramp up to steady state through the earlier development of Shaft 2. The 2022 Feasibility Study is based on the detailed design and engineering scenario first presented in the 2020 PEA, confirming the viability of a new phased development pathway to fast-track Platreef into production by Q3 2024.

The Platreef 2022 Feasibility Study first phase of production includes an initial 700,000 tonnes per annum (700 ktpa) underground mine and 770-ktpa-capacity concentrator, targeting high-grade mining areas close to the project's recently completed Shaft 1 (Figure 1).

Platreef's Phase 2, 5.2-Mtpa steady state production rate would rank it as the world's fifth largest primary platinum-group metals (PGM) mine on a palladium equivalent basis, with annual forecast production of more than 590,000 ounces of palladium, platinum, rhodium and gold, plus more than 40 million pounds of nickel and copper (Figure 8).

The Platreef 2022 Feasibility Study reflects the initial two phases of development for the Platreef Mine. Previous studies have demonstrated the resource base for future expansions up to 12 Mtpa, which would position Platreef among the very largest PGM producing mines in the world (Figure 8).

Watch a new video showcasing Platreef: https://vimeo.com/682603861/dce81b5e3a

Construction activities at the Platreef Project site, including Shaft 1 on the left, and the hitch-to-collar advancement for Shaft 2 on the right

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115055_dc4a96bb34cc28e8_002full.jpg

Platreef poised to complete journey from tier-one discovery to one of the world's largest and lowest-cost PGM producers

The Platreef Project, which includes an underground deposit of thick, high-grade PGE-nickel-copper-gold mineralization discovered by Ivanhoe's geologists, is in the northern limb of the Bushveld Complex approximately 11 kilometres from Mokopane, and 280 kilometres northeast of Johannesburg.

PGE-nickel-copper-gold mineralization in the northern limb is primarily hosted within the Platreef, a mineralized sequence which is traced more than 30 kilometres along strike. The Platreef Project is situated in the southern sector of the Platreef on two contiguous properties, Turfspruit and Macalacaskop, which comprise, in aggregate, approximately 7,842 hectares. The northernmost property, Turfspruit, is contiguous with and along strike from Anglo Platinum Limited's Mogalakwena group of properties and mining operations.

Ivanplats acquired a prospecting permit for Macalacaskop and Turfspruit in February 1998. In 1999, Ivanhoe began a series of drilling campaigns, totalling more than 726,000 metres, to advance Platreef from a greenfield exploration project focused on shallow mineralized zones through to focusing on deeper underground targets. At the height of the drilling campaign, 30 diamond drill rigs were producing more than 10,000 metres of core a week.

Since 2007, Ivanplats has focused its Platreef exploration and development activities on defining and advancing the thick, high-grade, down-dip extension of its original discovery at Platreef, now known as the Flatreef Deposit. In 2012, the Merensky Reef analogue was recognized.

The Flatreef Deposit lies entirely on the Turfspruit and Macalacaskop properties that form part of Ivanhoe's mining right. The thickness of the mineralized reef (T1 & T2 mineralized zones) intersected in Shaft 1 is 29 metres, with average grab sample grade of 6.35 grams per tonne (g/t) platinum, palladium and rhodium plus gold (3PE+Au), ranging up to 9.6 g/t 3PE+Au, as well as significant quantities of nickel and copper. This thickness is exceptional when compared to the typical, approximately one-metre-thick reefs being mined elsewhere on South Africa's Bushveld Complex.

A Japanese consortium led by JOGMEC, a Japanese government entity, and including Itochu and Japan Gas Corporation, acquired a 10% interest in the Platreef Project for approximately US$290 million.

The thick, high-grade, flat-lying Flatreef deposit was discovered in 2010. Ivanplats conducted an exploration program with 30 drill rigs totalling over 260,000 metres in 2011. Platreef has excellent exploration upside for further expansion and discovery.

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115055_dc4a96bb34cc28e8_003full.jpg

In June 2020, Ivanplats completed the sinking of Platreef's initial shaft, Shaft 1, to its final depth of 996 metres below surface. Shaft 1 is located approximately 450 metres away from a high-grade area of the Flatreef orebody, which will provide initial mining areas for Phase 1 production in 2024.

The thick Flatreef orebody also is flat-lying, which is ideal for safe, bulk-scale, mechanized mining and processes optimized for maximum ore extraction. Flatreef is characterized by its high-grade mineralization and a palladium-to-platinum ratio of approximately 1:1, which is considerably higher than other PGMs discoveries on the Northern Limb of the Bushveld.

Through phased development, Platreef is projected to become one of the world's largest and lowest-cost producers of palladium, platinum, rhodium, nickel, copper and gold. The 2022 Feasibility Study considers Phase 1 and Phase 2 development, including only one third of Platreef's Indicated Resources above an US$80/tonne Net Smelter Return (NSR) cut-off.

2022 Feasibility Study re-affirms outstanding economics of phased development at Platreef with an accelerated ramp up to 5.2 Mtpa

Mr. Friedland commented: "The Platreef discovery remains the world's greatest precious metals deposit under development, with a peerless endowment of palladium, rhodium, platinum, and gold; as well as highly significant quantities of strategic 'electric' metals such as nickel and copper. These outstanding economic results define our commitment to advance Platreef to first production, alongside our local communities and Japanese partners. We are counting down to less than 30 months from now. This achievement will only mark the first milestone, as we plan to expand this world-scale operation into one of the largest and lowest-cost, integrated PGM producers on the planet … all while generating outstanding returns on capital for a major, disruptive mine.

"PGMs have an integral role to play in the global transition to clean technologies, specifically the adoption of hydrogen energy systems; as well as the international push for lower emissions, which is led by developed economies … but let us not forget that emerging markets are catching up quickly … Platreef will be a responsible, industry leading, long-life supplier of palladium, rhodium, nickel, platinum, copper and gold … as well as a leading economic driver for South Africa. Ivanhoe Mines remains committed to 're-inventing mining' and will continue to leverage the most sustainable technologies available … as evidenced by our commitment to zero-emission, battery-powered equipment, and the adoption of the safest possible tailings method utilizing dry-stack technology, which has the added benefit of minimizing water consumption.

"Palladium and rhodium have reached all-time highs in recent years, currently trading at approximately $2,480 an ounce and $18,750 an ounce respectively, as progressively stricter air-quality rules increase demand for the metals used in vehicle pollution-control devices. Meanwhile, copper and nickel will continue to realize historic and sustained rallies due to underinvestment in new mine supply and massive growing demand tied to electric vehicles and global clean-energy initiatives."

Platreef's Indicated Mineral Resources contain an estimated 18.9 million ounces of palladium, 18.7 million ounces of platinum, 3.1 million ounces of gold, and 1.2 million ounces of rhodium (a combined 41.9 million ounces PGMs plus gold), plus 2.4 billion pounds of nickel and 1.2 billion pounds of copper, at a 2.0 g/t 3PE+Au cut-off.

Platreef's Inferred Mineral Resources contain an additional 23.8 million ounces of palladium, 23.2 million ounces of platinum, 4.3 million ounces of gold, and 1.6 million ounces of rhodium (a combined 52.8 million ounces PGMs plus gold), plus 3.4 billion pounds of nickel and 1.78 billion pounds of copper, also at a 2.0 g/t 3PE+Au cut-off.

Mr. Friedland added: "The thick and flat-lying nature of the high-grade mineralization of the Flatreef deposit allows for the use of state-of-the-art, automated, electric mining machinery, including cutting-edge battery driven underground vehicles.

"For Ivanhoe Mines, achieving first production at Platreef will mark the next milestone in the journey to become a new-age, major diversified mining company ..... we intend to build on the achievements of the Kamoa-Kakula Copper Joint Venture in the Democratic Republic of Congo, and leverage the countless lessons we have learned during phased development at our tier-one copper asset … and let us not forget, Platreef still has vast potential to significantly expand the already enormous resource base … as well as a plethora of new nickel-sulphide exploration opportunities, many of which are near surface."

Phase 1 construction underway, with first production expected in Q3 2024

Detailed engineering studies are underway on the initial 770-ktpa mine and concentrator, in parallel with the changeover of Shaft 1 into a production shaft, with expected completion in March 2022. First delivery of the initial battery-electric underground fleet is expected imminently, and the first blast on the 950-metre level is anticipated in April 2022. The initial underground development focus from Shaft 1 will be the on the first ventilation raise and ore passes connecting the 750-metre level to the 950-metre level.

Earthworks for the first concentrator are planned to begin in Q2 2022, followed by civil works and the ordering of long-lead-time items in H2 2022. First ore feed to the concentrator is planned for Q3 2024.

Phase 1 average annual production is estimated at 113,000 ounces (oz.) of platinum, palladium, rhodium and gold (3PE+Au), plus 5 million pounds of nickel and 3 million pounds of copper.

Figure 1: Production and timeline schematic of Platreef 2022 Feasibility Study.

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115055_dc4a96bb34cc28e8_004full.jpg

William Mamashela (left) and William Mello, with local contractor Somuthwa Construction, assisting with construction of the Platreef Mine.

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115055_dc4a96bb34cc28e8_005full.jpg

Shaft 2 commissioning accelerated to 2027, expediting Phase 2 expansion

While the 700-ktpa initial mine is operating using Shaft 1, the sinking of the project's second, larger shaft (Shaft 2), that drives the Phase 2 expansion to 5.2 Mtpa, will progress at the same time. The 2022 Feasibility Study envisions Shaft 2 equipped for hoisting in 2027, an accelerated schedule by approximately 18 months compared to the 2020 PEA, coming online just over three years from first production of Phase 1.

Once Shaft 2 is complete, two 2.2-Mtpa concentrator modules will be commissioned, and the initial concentrator will be ramped up to its full capacity of 770-ktpa; increasing the steady-state production to 5.2 Mtpa (Figure 1).

The Phase 2 expansion would result in Platreef becoming the world's fifth largest primary platinum-group metals (PGM) mine on a palladium equivalent basis, with annual forecast production of more than 590,000 ounces of palladium, rhodium, platinum, and gold, plus more than 40 million pounds of nickel and copper (Figure 6).

Construction at Shaft 2, which now is expected to be commissioned by 2027.

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115055_dc4a96bb34cc28e8_006full.jpg

Platreef's immense mineral endowment supports future expansions

The 2022 Feasibility Study considers Platreef's Phase 1 and Phase 2 development, including only one third of the Indicated Resources above an US$80/tonne Net Smelter Return (NSR) cut-off. If the remainder of the Indicated Resources were to be converted to reserves, it would provide an opportunity to massively expand production.

As development of the project progresses, additional drilling from underground will be undertaken with the goal of increasing the confidence of the current mineral resources, as well as to expand the resource base. Additional studies will follow up on the previous work that envisaged further phased expansions based on updated reserves.

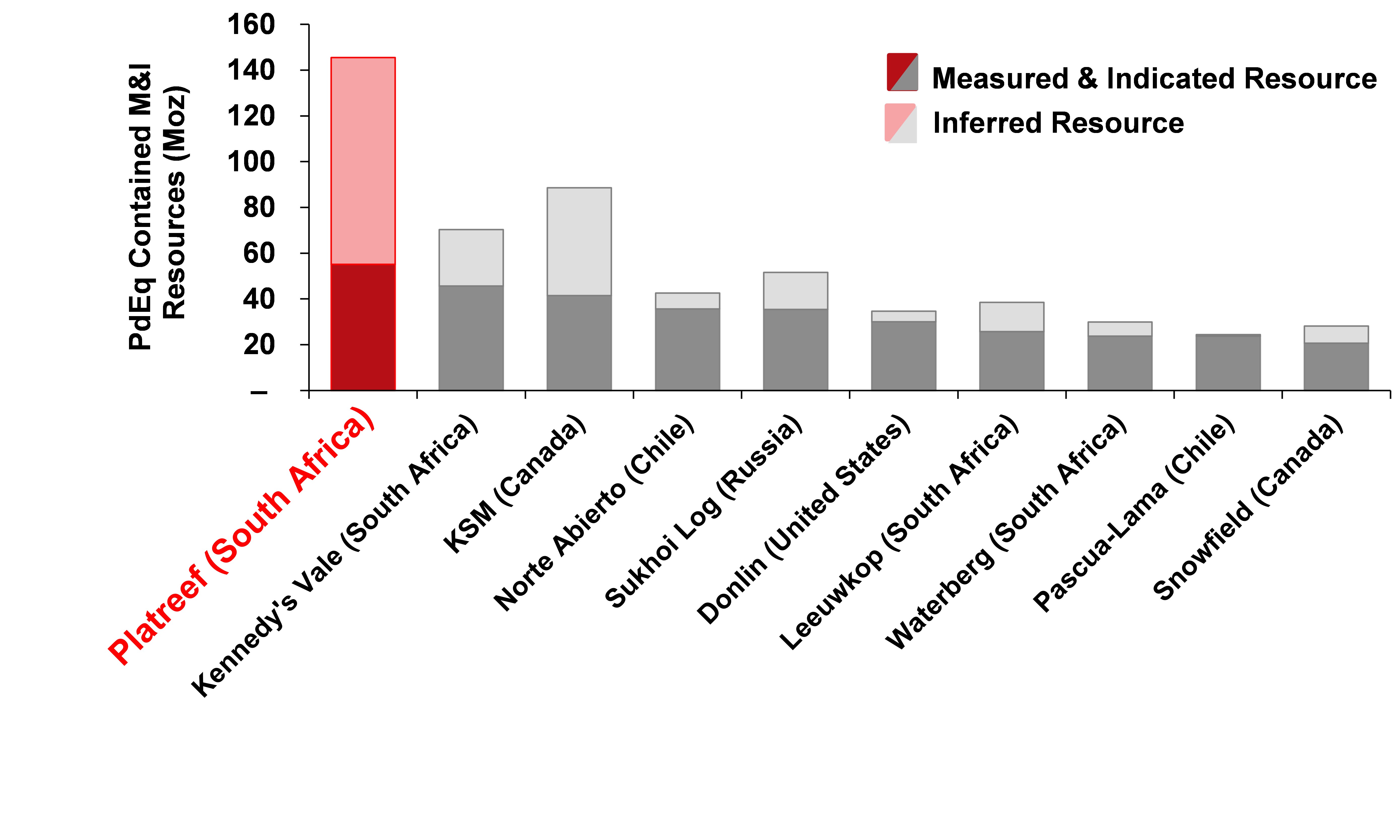

Figure 2: World's largest precious metal deposits under development ranked by contained metal in Measured & Indicated Resources.

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115055_dc4a96bb34cc28e8_007full.jpg

Source: Company filings, S&P Global Market Intelligence. Notes: Chart ranks the largest undeveloped primary palladium, platinum, gold, silver and rhodium projects from the S&P Global Market Intelligence database based on measured and indicated palladium equivalent resource. Palladium equivalent calculation includes palladium, platinum, gold, silver and rhodium ounces and has been calculated using spot price metal price assumptions (February 23, 2022) of US$1,095/oz platinum, US$2,480/oz palladium, US$18,750/oz rhodium, US$1,909/oz gold and US$24.55/oz silver. Measured and Indicated resources for Platreef correspond to palladium, platinum, gold and rhodium ounces at a 1 g/t cut-off grade.

Tshifhiwa Netshirando, Platreef's Production Manager, is focused on equipping Shaft 1 for first production within just over two years.

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115055_dc4a96bb34cc28e8_009full.jpg

Aerial view from February 2022 of current construction at the Platreef site, including Shaft 1 (right) and progress at Shaft 2 (left).

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115055_dc4a96bb34cc28e8_008full.jpg

Platreef will positively transform mining and community development in Limpopo Province

Ivanhoe Mines' President, Marna Cloete, commented: "Ivanhoe Mines is excited to become a disruptive, cornerstone participant in the future of South Africa's platinum-group-metals mining industry. We have established a strong strategic foothold on the giant polymetallic Northern Limb of the renowned Bushveld Complex. We look forward to sharing the benefits of this truly unique orebody with our partners and local communities, as well as all the people of South Africa … Platreef represents an important, long-life economic driver for the nation, and we have only just begun to tap into the potential of this amazing discovery.

"We are pleased to be building the cutting-edge transformation in future underground platinum-group-metals mining operations in South Africa. We are charting a new path in the empowerment of the local people in Limpopo Province and in the training of women in the mining industry. We are focused on creating a vibrant local economy that's not just going to be mining, as we are enabling entrepreneurs to create and expand a plethora of new businesses.

Dr. Patricia Makhesha, Ivanhoe's Executive Vice President, Sustainability and Special Projects, added: "The agreement with the Mogalakwena Local Municipality to recycle wastewater is an important milestone in Platreef's development. Recycling locally treated water is a cost-effective and sustainable approach to securing water for the Platreef Project."

Ivanhoe Mines indirectly owns 64% of the Platreef Project through its subsidiary, Ivanplats, and is directing all mine development work. The South African beneficiaries of the approved broad-based, black economic empowerment structure have a 26% stake in the Platreef Project. The remaining 10% is owned by a Japanese consortium of ITOCHU Corporation; Japan Oil, Gas and Metals National Corporation; ITC Platinum Development Ltd., an ITOCHU affiliate; and Japan Gas Corporation.

The Platreef 2022 Feasibility Study was independently prepared by OreWin Pty Ltd. of Adelaide, Australia; Mine Technical Services of Reno, USA; SRK Consulting Inc. of Johannesburg, South Africa; DRA Global of Johannesburg, South Africa; and Golder Associates Africa of Midrand, South Africa.

A National Instrument 43-101 technical report will be filed on SEDAR at www.sedar.com and on the Ivanhoe Mines website at www.ivanhoemines.com within 45 days of the issuance of this news release.

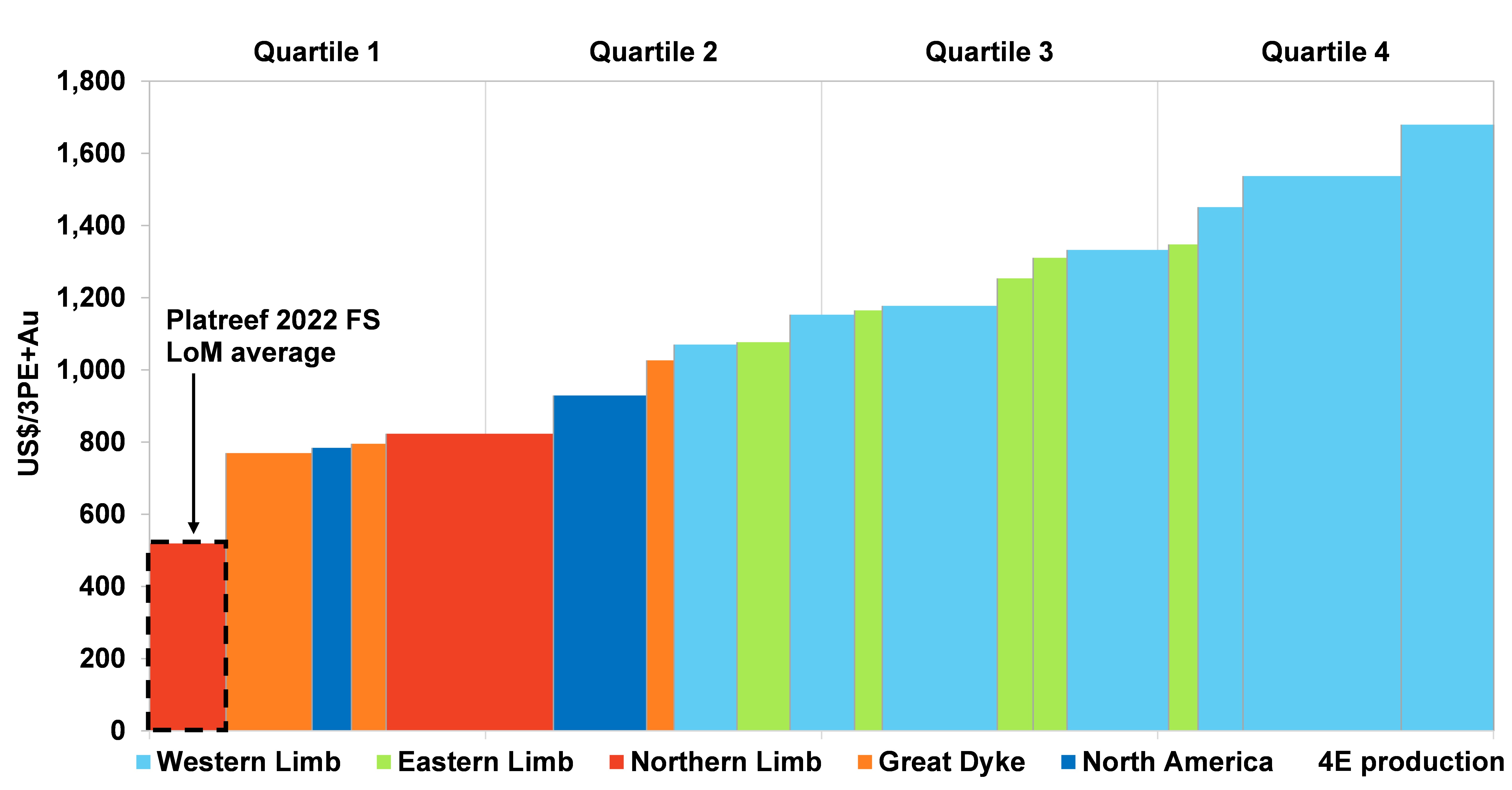

Platreef's thick mineralization, which will be mined with highly-productive mechanized methods, combined with higher nickel and copper grades, contribute to lower cash costs compared to other primary platinum-group-metal producers (Figures 7). Among global primary platinum-group-metals producers, Platreef's estimated net total cash cost of US$514 per 3PE+Au ounce, net of copper and nickel by-product credits and including sustaining capital costs, ranks at the bottom of the cash-cost curve (Figure 7).

Construction of the Shaft 1 waste-rock conveyor system is progressing in advance of the start of underground mining operations.

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115055_dc4a96bb34cc28e8_010full.jpg

Thapelo Kadi, Senior Manager for Safety Legal and Compliance, fosters a safety culture that strives toward Platreef's vision of zero harm.

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115055_dc4a96bb34cc28e8_011full.jpg

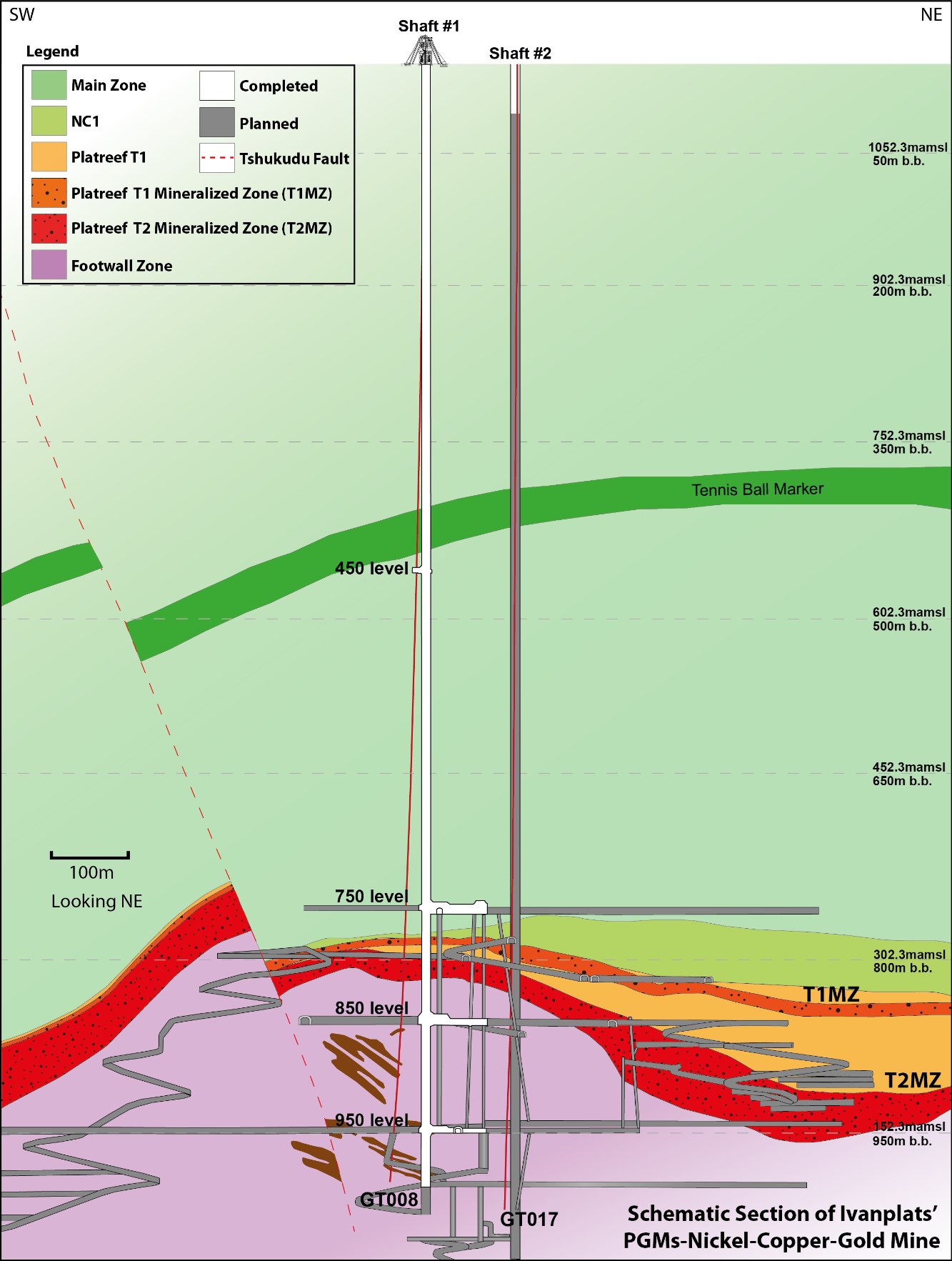

Figure 3: Schematic section of the Platreef Mine, showing Flatreef's thick, high-grade T1 and T2 mineralized zones (dark orange and red), underground development work completed to date in shafts 1 and 2 (white) and planned development work (grey).

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115055_dc4a96bb34cc28e8_012full.jpg

Members of Ivanplat's underground mining team advancing the world-scale Platreef Mine toward first production in 2024.

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115055_dc4a96bb34cc28e8_013full.jpg

Alfred Masimine, Bell Operator (left), and Malesela Magongoa, Sinker, underground at the 950-level station discussing the installation of the loading box at shaft bottom.

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115055_dc4a96bb34cc28e8_014full.jpg

Figure 4: Map of South Africa's Bushveld Igneous Complex.

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115055_dc4a96bb34cc28e8_015full.jpg

Source: SFA (Oxford).

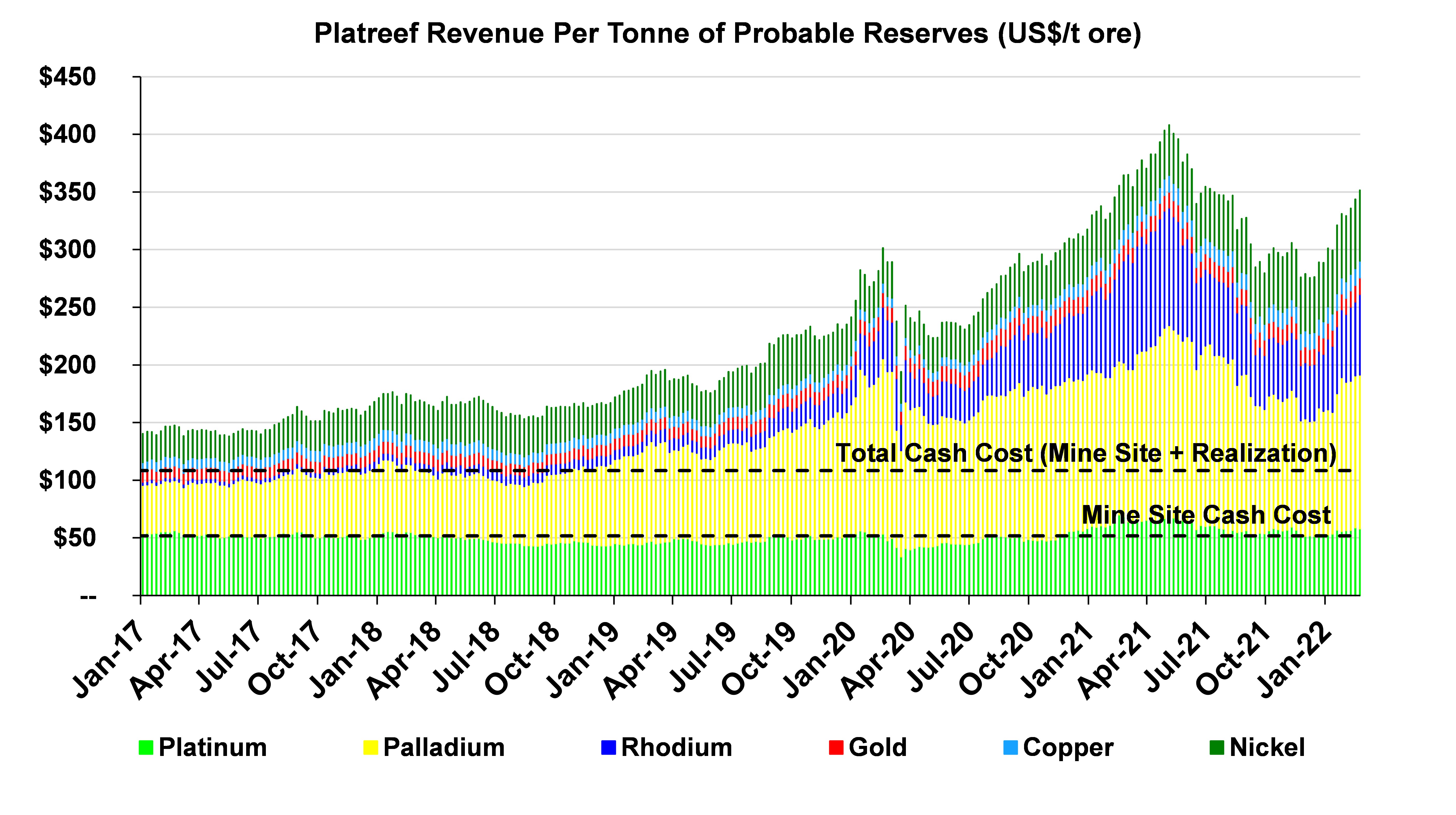

Figure 5: Revenue per tonne of ore at the Platreef Project since 2017 (shown in US dollars).

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115055_dc4a96bb34cc28e8_016full.jpg

Figure 6: Revenue per tonne of ore at the Platreef Project has risen significantly since 2017 (shown in South African rand).

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115055_dc4a96bb34cc28e8_017full.jpg

Source for figures 5 and 6: Bloomberg. Based on historical weekly commodity prices at the end of each week.

Notes for figures 5 and 6:

- Based on Platreef Mineral Reserves with an effective date of January 26, 2022.

- Probable Mineral Reserve of 124.7 million tonnes at a grade of 1.95 grams per tonne (g/t) platinum, 2.01 g/t palladium, 0.30 g/t gold, 0.14 g/t rhodium, 0.34% nickel and 0.17% copper.

- A declining Net Smelter Return (NSR) cut-off of $155 per tonne (t) to $80/t was used for the Mineral Reserve estimates.

- The NSR cut-off is an elevated cut-off above the marginal economic cut-off.

- Metal prices used in the Mineral Reserve estimate: US$1,600 per ounce (oz.) platinum, US$815/oz. palladium, US$1,300/oz. gold, US$1,500/oz. rhodium, US$8.90 per pound (lb) nickel and US$3.00/lb copper.

- Tonnage and grade estimates include dilution and mining recovery allowances.

- Applies life-of-mine average recoveries of 87.4% for platinum, 86.9% for palladium, 78.6% for gold, 80.5% for rhodium, 87.9% for copper and 71.9% for nickel.

- Total cash cost includes mine site costs, plus realization costs such as treatment and refining charges, royalties and transportation.

Figure 7: Global primary producers' net total cash cost + sustaining capital (2021E), US$/3PE+Au oz.

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115055_dc4a96bb34cc28e8_018full.jpg

Source: SFA (Oxford), Ivanplats. Notes: Cost and production data for the Platreef project is based on the Platreef Feasibility Study parameters, applying payabilities and smelting and refining charges as agreed with purchase of concentrate partners for Platreef concentrate (this is not representative of SFA's standard methodology). SFA's peer group cost and production data follows a methodology to provide a level playing field for smelting and refining costs on a pro-rata basis from the producer processing entity. Net total cash costs have been calculated using Ivanplats' long term price assumptions of 16:1 ZAR:USD, US$1,100/oz platinum, US$1,450/oz palladium, US$5,000/oz rhodium, US$1,600/oz gold, US$8.00/lb nickel and US$3.50/lb copper.

Figure 8: Ranking of selected global primary PGM producers, based on 2021E palladium equivalent production

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115055_dc4a96bb34cc28e8_019full.jpg

Source: SFA (Oxford), Ivanplats. Notes: Chart excludes by-product PGM producers. Nornickel (by-product PGM producer) is the largest producer on a palladium equivalent basis. Cost and production data for the Platreef project is based on the Platreef 2022 FEASIBILITY STUDY and 2014 PEA parameters. Production data for the peer group is provided by SFA (Oxford). Equivalent palladium production has been calculated using Ivanplats' long term price assumptions of 16:1 ZAR:USD, US$1,100/oz platinum, US$1,450/oz palladium, US$5,000/oz rhodium, US$1,600/oz gold, US$8.00/lb nickel and US$3.50/lb copper.

2022 FEASIBILITY STUDY HIGHLIGHTS

Phased development plan targets first production from Phase 1 in Q3 2024, and accelerated Phase 2 expansion to realize potential of Platreef orebody

- The Platreef 2022 Feasibility Study evaluates the phased development of Platreef, with an initial 700-ktpa underground mine and a 770-ktpa capacity concentrator, targeting high-grade mining areas close to Shaft 1, with an initial capital cost of US$488 million.

- First concentrate production for Phase 1 is planned for Q3 2024, with the Phase 2 expansion based on the commissioning of Shaft 2 in 2027, followed by the commissioning of two 2.2-Mtpa concentrators in 2028 and 2029. This would increase the steady-state production to 5.2 Mtpa by using Shaft 2 as the primary production shaft.

- Expansion capital cost for Phase 2 is estimated at US$1.5 billion, which may be partially funded by cash flows from Phase 1 and a project financing package.

- Ivanplats' dedicated engineering teams and leading consultants are evaluating optimizations to the sinking methodology for Shaft 2 to further accelerate the availability of the shaft for hoisting, which may accelerate the overall development timeline.

- Phase 1 average annual production of 113,000 ounces (oz.) of platinum, palladium, rhodium and gold (3PE+Au), plus 5 million pounds of nickel and 3 million pounds of copper.

- Phase 2 average annual production of 591,000 oz. of 3PE+Au, plus 26 million pounds of nickel and 16 million pounds of copper, which would rank Platreef as the fifth largest primary PGM producer on a palladium equivalent basis (Figure 8)

- Life-of-mine cash cost of US$514 per ounce of 3PE+Au, net of by-products, and including sustaining capital costs would rank Platreef as the lowest cost primary PGM producer (Figure 7)

- After-tax net present value at an 8% discount rate (NPV8%) of US$1.7 billion and an internal rate of return (IRR) of 18.5%, based on long-term consensus prices.

- At spot prices as at February 23, 2022, the after-tax NPV8% increases to US$4.1 billion and the IRR increases to 29.3%.

- Shaft 1 equipping and changeover to hoisting is nearing completion, expected by end of March 2022, together with the arrival of initial battery electric underground mining fleet.

- In parallel with the changeover of Shaft 1 for permanent hoisting, detailed engineering and certain optimization initiatives are underway on the mine design, 770-ktpa concentrator and associated infrastructure design, which also will include the dry stack tailings storage facility. In addition, amendments to the water use licence, waste licence and environmental impact assessment required for the phased development plan have been lodged.

- Following the completion of the changeover of Shaft 1, off-shaft development will start in April 2022 with the initial aim of enabling construction of the first ventilation raise.

- With the focus shifting to execution, appointment and onboarding of earthworks contractors is the next short-term milestone for surface work, while detailed design across the project ramps up.

Figure 9: Plan of the Platreef 2022 Feasibility Study mine design, highlighting areas that are mined during Phase 1 (700-ktpa) and Phase 2 (5.2 Mtpa).

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115055_dc4a96bb34cc28e8_020full.jpg

Figure by OreWin, 2022.

KEY INITIAL RESULTS FROM THE PLATREEF 2022 FEASIBILITY STUDY

Table 1: Summary of key results of the Platreef 2022 Feasibility Study.

| Item | Units | Total / Average Life of Mine |

| Mined and processed | ||

| Material Milled | Million tonnes | 125 |

| Platinum | g/t | 1.94 |

| Palladium | g/t | 1.99 |

| Gold | g/t | 0.30 |

| Rhodium | g/t | 0.13 |

| 3PE+Au | g/t | 4.37 |

| Copper | % | 0.16 |

| Nickel | % | 0.34 |

| Peak Production (Year 8) | ||

| 3PE+Au | koz | 697 |

| Nickel | kt | 13 |

| Copper | kt | 8 |

| Key financial results | ||

| Life of mine | Years | 28.3 |

| Initial capital | US$ million | 488 |

| Expansion capital | US$ million | 1,480 |

| Peak capital | US$ million | 1,364 |

| Mine-site cash cost | US$ per ounce 3PE+Au | 429 |

| Total cash cost after credits | US$ per ounce 3PE+Au | 452 |

| All-in cash cost after credits | US$ per ounce 3PE+Au | 514 |

| Mine-site operating costs | US$ per tonne milled | 52 |

| After-tax NPV8% | US$ million | 1,690 |

| After-tax IRR | % | 18.5 |

| Project payback period | years | 7.9 |

Notes:

- 3PE+Au = platinum, palladium, rhodium and gold.

- Long-term metal price assumptions for economic analysis are as follows: US$1,100/oz. platinum, US$1,450/oz. palladium, US$1,600/oz. gold, US$5,000/oz. rhodium, US$8.00/lb nickel and US$3.50/lb copper.

- All-in cash costs include sustaining capital costs.

Khazamola Baloyi, Government Relations Manager, at the Platreef site office.

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115055_dc4a96bb34cc28e8_021full.jpg

Sample of the high-grade palladium-platinum-rhodium-nickel-copper-gold ore.

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115055_dc4a96bb34cc28e8_022full.jpg

Table 2: Platreef 2022 Feasibility Study financial results at base case and spot prices.

| Discount Rate | Base Case Prices (1) | Spot Prices (2) | |

| Net present value (NPV) | Undiscounted | 8,543 | 17,130 |

| (US$ million, after tax) | 5.0% | 3,098 | 6,815 |

| 8.0% | 1,690 | 4,116 | |

| 10.0% | 1,104 | 2,979 | |

| 12.0% | 692 | 2,169 | |

| Internal rate of return (IRR) | 18.5% | 29.3% | |

| Project payback period | (Years) | 7.9 | 6.4 |

| Exchange rate | (ZAR: USD) | 16:1 | |

- Base case metal price assumptions are as follows: US$1,100/oz. platinum, US$1,450/oz. palladium, US$1,600/oz. gold, US$5,000/oz. rhodium, US$8.00/lb nickel and US$3.50/lb copper.

- Spot metal prices as at February 23, 2022 are as follows: US$1,095/oz. platinum, US$2,480/oz. palladium, US$1,909/oz. gold, US$18,750 /oz. rhodium, US$11.31/lb nickel and US$4.48/lb copper.

Table 3: Platreef 2022 Feasibility Study average mine production and processing statistics.

| Item | Units | Phase 1 Average (1) | Phase 2 Average (2) | LOM Average |

| Production | Mtpa | 0.7 | 4.9 | 4.4 |

| Platinum | g/t | 2.53 | 1.93 | 1.94 |

| Palladium | g/t | 2.54 | 1.98 | 1.99 |

| Gold | g/t | 0.38 | 0.30 | 0.30 |

| Rhodium | g/t | 0.17 | 0.13 | 0.13 |

| 3PE+Au(2) | g/t | 5.63 | 4.34 | 4.37 |

| Copper | % | 0.19 | 0.16 | 0.16 |

| Nickel | % | 0.40 | 0.34 | 0.34 |

| Recoveries | ||||

| Platinum | % | 90.4 | 87.2 | 87.2 |

| Palladium | % | 90.2 | 86.7 | 86.8 |

| Gold | % | 80.4 | 78.5 | 78.5 |

| Rhodium | % | 84.4 | 80.2 | 80.3 |

| 3PE+Au(2) | % | 89.4 | 86.0 | 86.2 |

| Copper | % | 90.0 | 87.6 | 87.7 |

| Nickel | % | 77.5 | 71.4 | 71.6 |

| Concentrate produced | kt/a (dry) | 34.9 | 216.2 | 195.7 |

| Platinum | g/t | 38.1 | 38.2 | 38.2 |

| Palladium | g/t | 38.1 | 39.0 | 39.0 |

| Gold | g/t | 5.1 | 5.3 | 5.3 |

| Rhodium | g/t | 2.4 | 2.4 | 2.4 |

| 3PE + Au (3) | g/t | 83.8 | 85.0 | 85.0 |

| Copper | % | 2.8 | 3.3 | 3.3 |

| Nickel | % | 5.1 | 5.4 | 5.4 |

| Recovered metal | ||||

| Platinum | koz/a | 51 | 266 | 240 |

| Palladium | koz/a | 51 | 271 | 245 |

| Gold | koz/a | 7 | 37 | 33 |

| Rhodium | koz/a | 3 | 17 | 15 |

| 3PE + Au(2) | koz/a | 113 | 591 | 535 |

| Copper | Mlb/a | 3 | 16 | 14 |

| Nickel | Mlb/a | 5 | 26 | 23 |

- Phase 1 production over 3.3 years from 2024 to 2027 at 0.7 Mtpa.

- Phase 2 production over 25.0 years from 2028 to 2052 at 5.2 Mtpa.

- 3PE+Au is the sum of the grades for and production of platinum, palladium, rhodium and gold.

Figure 10: Platreef 2022 Feasibility Study concentrator production (tonnes milled and grades for the life-of-mine).

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115055_dc4a96bb34cc28e8_023full.jpg

Figure by OreWin, 2022.

Figure 11: Platreef 2022 Feasibility Study estimated 3PE+Au recovered metal and nickel/copper recovered metal for the life-of-mine.

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115055_dc4a96bb34cc28e8_024full.jpg

Figure by OreWin, 2022.

Table 4: Platreef 2022 Feasibility Study unit operating costs and cash costs after credits.

| US$ per ounce of 3PE+Au | |||

| Phase 1 Average (1) | Phase 2 Average (2) | LOM Average | |

| Mine site | 822 | 419 | 429 |

| Transport | 13 | 13 | 13 |

| Treatment & Refining | 369 | 366 | 366 |

| Royalties | 8 | 90 | 88 |

| Total cash costs before credits | 1,212 | 887 | 895 |

| Nickel credits | 334 | 351 | 351 |

| Copper credits | 84 | 92 | 92 |

| Total cash costs after credits | 794 | 443 | 452 |

| Sustaining capital costs (3) | - | 63 | 62 |

| All-in cash costs after credits (4) | 794 | 506 | 514 |

- Phase 1 production over 3.3 years from 2024 to 2027 at 0.7 Mtpa.

- Phase 2 production over 25.0 years from 2028 to 2052 at 5.2 Mtpa.

- Phase 1 operating costs include allowance for sustaining capital costs.

- All-in cash costs include sustaining capital costs.

Table 5: Platreef 2022 Feasibility Study capital investment summary.

| Description | Initial Capital | Expansion Capital | Sustaining Capital | Total |

| US$M | US$M | US$M | US$M | |

| MINING | ||||

| Exploration and geology | 9 | 31 | 32 | 72 |

| Mining | 187 | 697 | 861 | 1,744 |

| Subtotal | 195 | 728 | 893 | 1,816 |

| CONCENTRATOR | ||||

| Concentrator | 73 | 273 | 2 | 349 |

| Subtotal | 73 | 273 | 2 | 349 |

| INFRASTRUCTURE | ||||

| Infrastructure | 95 | 251 | 25 | 371 |

| Subtotal | 95 | 251 | 25 | 371 |

| INDIRECTS | ||||

| Owners Cost | 93 | 126 | 2 | 222 |

| Closure | - | - | 11 | 11 |

| Subtotal | 93 | 126 | 13 | 233 |

| CAPITAL EXPENDITURE BEFORE CONTINGENCY | 456 | 1,378 | 933 | 2,768 |

| Contingency | 32 | 101 | 1 | 134 |

| CAPITAL EXPENDITURE AFTER CONTINGENCY | 488 | 1,480 | 934 | 2,902 |

Note: Initial capital reflects the capital costs from January 1, 2022, to achieve initial production of 0.7 Mtpa, followed by expansion capital to reflect the capital costs to achieve full production of 5.2 Mtpa. Expansion capital includes US$50 million spent during the Phase 1 pre-production period to continue construction on Shaft 2.

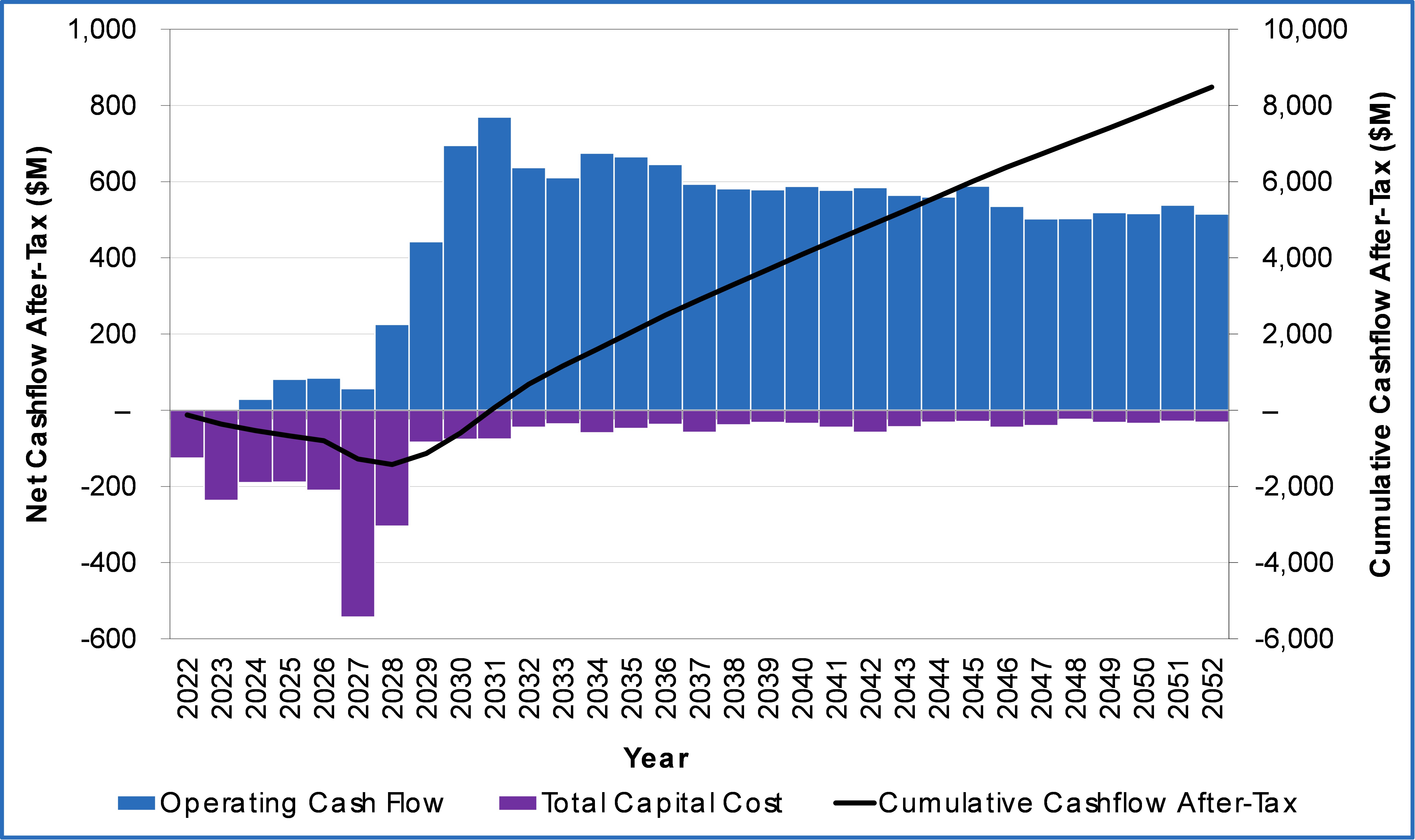

Figure 12: Platreef Mine 2022 Feasibility Study projected operating surplus, total capital costs and cumulative net cash flow after tax, at base case assumptions.

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115055_dc4a96bb34cc28e8_025full.jpg

Figure by OreWin, 2022.

Platreef Mineral Resources

The mineral resources used in the Feasibility Study were those amenable to underground selective mining.

Table 6: Mineral Resources amenable to underground selective mining methods (base case is highlighted).

| Indicated Mineral Resources Tonnage and Grades | ||||||||

| Cut-off 3PE+Au | Mt | Pt (g/t) | Pd (g/t) | Au (g/t) | Rh (g/t) | 3PE+Au (g/t) | Cu (%) | Ni (%) |

| 3 g/t | 204 | 2.11 | 2.11 | 0.34 | 0.14 | 4.70 | 0.18 | 0.35 |

| 2 g/t | 346 | 1.68 | 1.70 | 0.28 | 0.11 | 3.77 | 0.16 | 0.32 |

| 1 g/t | 716 | 1.11 | 1.16 | 0.19 | 0.08 | 2.55 | 0.13 | 0.26 |

| Indicated Mineral Resources Contained Metal | ||||||||

Cut-off | Pt (Moz) | Pd Moz) | Au (Moz) | Rh (Moz) | 3PE+Au (Moz) | Cu (Mlb) | Ni (Mlb) | |

| 3 g/t | 13.9 | 13.9 | 2.2 | 0.9 | 30.9 | 800 | 1,597 | |

| 2 g/t | 18.7 | 18.9 | 3.1 | 1.2 | 41.9 | 1,226 | 2,438 | |

| 1 g/t | 25.6 | 26.8 | 4.5 | 1.8 | 58.8 | 2,076 | 4,108 | |

| Inferred Mineral Resources Tonnage and Grades | ||||||||

| Cut-off 3PE+Au | Mt | Pt (g/t) | Pd (g/t) | Au (g/t) | Rh (g/t) | 3PE+Au (g/t) | Cu (%) | Ni (%) |

| 3 g/t | 225 | 1.91 | 1.93 | 0.32 | 0.13 | 4.29 | 0.17 | 0.35 |

| 2 g/t | 506 | 1.42 | 1.46 | 0.26 | 0.10 | 3.24 | 0.16 | 0.31 |

| 1 g/t | 1,431 | 0.88 | 0.94 | 0.17 | 0.07 | 2.05 | 0.13 | 0.25 |

| Inferred Mineral Resources Contained Metal | ||||||||

Cut-off | Pt (Moz) | Pd Moz) | Au (Moz) | Rh (Moz) | 3PE+Au (Moz) | Cu (Mlb) | Ni (Mlb) | |

| 3 g/t | 13.8 | 14.0 | 2.3 | 1.0 | 31.0 | 865 | 1,736 | |

| 2 g/t | 23.2 | 23.8 | 4.3 | 1.6 | 52.8 | 1,775 | 3,440 | |

| 1 g/t | 40.4 | 43.0 | 7.8 | 3.1 | 94.3 | 4,129 | 7,759 | |

- Mineral Resources were estimated and finalized April 22, 2016. On 28 January 2022, updated criteria for assessing reasonable prospects of eventual extraction were reviewed to ensure the estimate remained current. The updated effective date is 28 January 2022. The Qualified Person for the estimate is Mr. Timothy Kuhl, RM SME.

- Mineral Resources are reported inclusive of Mineral Reserves. Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability.

- The 2 g/t 3PE+Au cut-off is considered the base-case estimate and is highlighted. The rows are not additive.

- Mineral Resources are reported on a 100% basis. Mineral Resources are stated from approximately -200 m to 650 m elevation (from 500 m to 1,350 m depth). Indicated Mineral Resources are drilled on approximately 100 x 100 m spacing; Inferred Mineral Resources are drilled on 400 x 400 m (locally to 400 x 200 m and 200 x 200 m) spacing.

- Reasonable prospects for eventual economic extraction were determined using the following assumptions. Assumed commodity prices are US$1,600/oz. platinum, US$815/oz. palladium, US$1,300/oz. gold, US$1,500/oz. rhodium, US$3.00/lb copper, and US$8.90/lb nickel. It has been assumed that payable metals would be 82% from smelter/refinery and that mining costs (average US$34.27/t) and process, general and administrative costs, and concentrate transport costs (average US$15.83/t of mill feed for a four-Mtpa operation) would be covered. The processing recoveries vary with block grade but typically would be 80%-90% for platinum, palladium and rhodium; 70-90% for gold; 60-90% for copper; and 65-75% for nickel.

- 3PE+Au = platinum, palladium, rhodium and gold.

- Totals may not sum due to rounding.

Platreef 2020 Feasibility Study Mineral Reserve

The mineral resources used as the basis of the Feasibility Study were those amenable to underground selective mining.

Table 7: Probable Mineral Reserves - tonnage and grades as at January 26, 2022.

| Method | Mt | NSR ($/t) | Pt (g/t) | Pd (g/t) | Au (g/t) | Rh (g/t) | 3PE+Au (g/t) | Cu (%) | Ni (%) |

| Ore development | 11.0 | 142 | 1.79 | 1.85 | 0.27 | 0.12 | 4.03 | 0.15 | 0.31 |

| Long-hole | 93.9 | 152 | 1.88 | 1.95 | 0.29 | 0.13 | 4.25 | 0.16 | 0.33 |

| Drift-and-fill | 20.3 | 184 | 2.30 | 2.25 | 0.37 | 0.15 | 5.07 | 0.18 | 0.37 |

| Total | 125.2 | 156 | 1.94 | 1.99 | 0.30 | 0.13 | 4.37 | 0.16 | 0.34 |

| Method | Mt | Pt (Moz) | Pd (Moz) | Au (Moz) | Rh (Moz) | 3PE+Au (Moz) | Cu (Mlb) | Ni (Mlb) |

| Ore development | 11.0 | 0.6 | 0.7 | 0.1 | 0.04 | 1.42 | 37 | 76 |

| Long-hole | 93.9 | 5.7 | 5.9 | 0.9 | 0.40 | 12.84 | 336 | 687 |

| Drift-and-fill | 20.3 | 1.5 | 1.5 | 0.2 | 0.10 | 3.31 | 83 | 166 |

| Total | 125.2 | 7.8 | 8.0 | 1.2 | 0.54 | 17.57 | 455 | 929 |

- Mineral Reserves have an effective date of January 26, 2022. The Qualified Person for the estimate is Curtis Smith (OreWin), MAusIMM (CP).

- A declining NSR cut-off of US$155/t to US$80/t was used for the Mineral Reserve estimates.

- The NSR cut-off is an elevated cut-off above the marginal economic cut-off.

- Metal prices used in the Mineral Reserve estimate are as follows: US$1,600/oz. platinum, US$815/oz. palladium, US$1,300/oz. gold, US$1,500/oz. rhodium, US$8.90/lb nickel and US$3.00/lb copper.

- Metal-price assumptions used for the Feasibility Study economic analysis are as follows: US$1,100/oz. platinum, US$1,450/oz. palladium, US$1,600/oz. gold, US$5,000/oz. rhodium, US$8.00/lb nickel and US$3.50/lb copper.

- Tonnage and grade estimates include dilution and mining recovery allowances.

- Total may not add due to rounding.

- 3PE+Au = platinum, palladium, rhodium and gold.

Platreef to be mined primarily using highly productive mechanized methods

Mining zones in the current Platreef mine plan occur at depths ranging from approximately 700 metres to 1,200 metres below surface. Mining will be performed using highly productive mechanized methods, including long-hole stoping and drift-and-fill. Each method will utilize cemented backfill for maximum ore extraction.

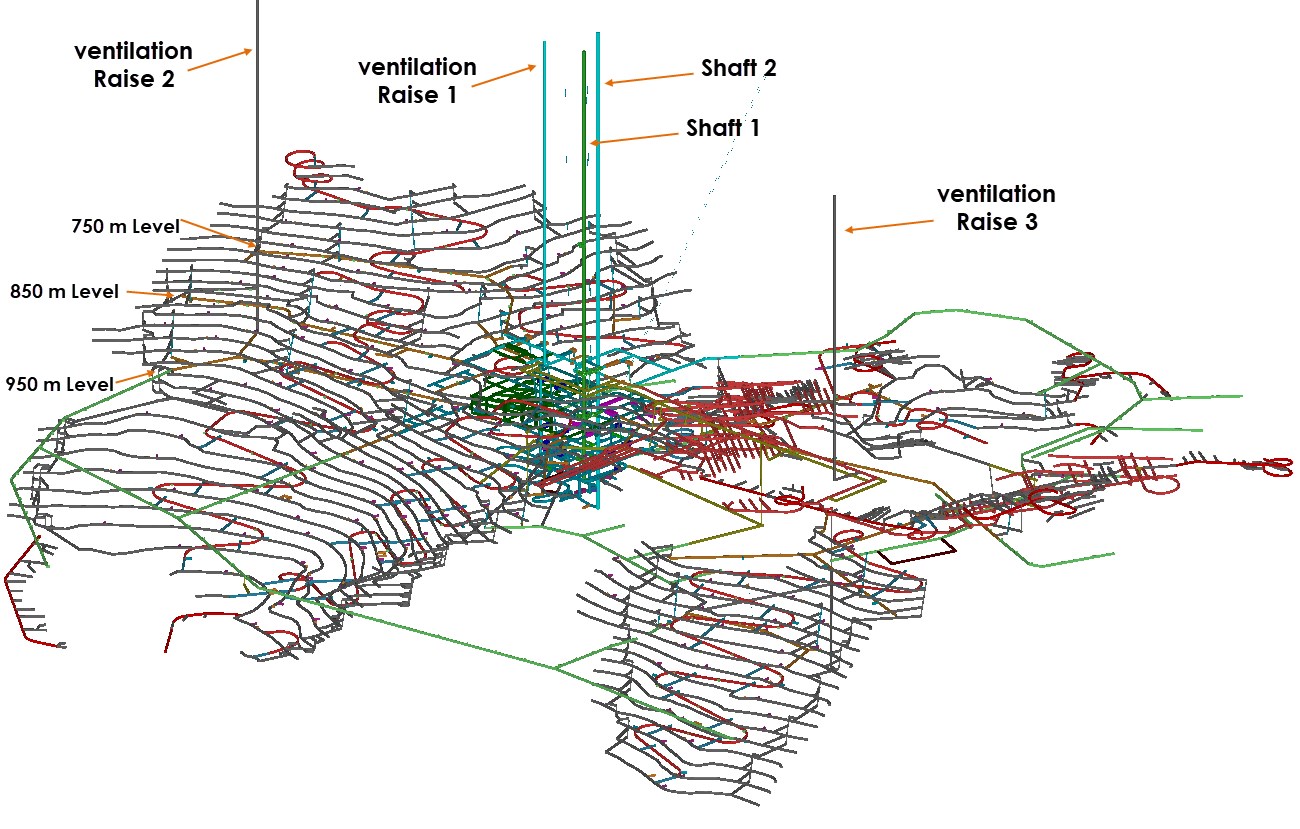

Figure 13 shows the proposed shaft and ventilation raise locations, and the main access levels in an elevated view (looking north-east). Mining access ramps will connect the haulage levels with the mining sublevels and other infrastructure. The mining sublevels will be developed from the ramps at regular vertical intervals in the production areas. Drilling and extraction levels for stopes will be driven from the sublevels.

Figure 13: Platreef underground mine access layout.

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115055_dc4a96bb34cc28e8_026full.jpg

Figure by OreWin, 2022.

Following the completion of the changeover of Shaft 1, off-shaft development would start in April 2022 with the initial aim of enabling construction of the critical ventilation shaft 1 (Figure 14). This ventilation shaft not only enables future development of underground infrastructure but is planned to be the secondary means of egress from the mine until Shaft 2 is complete. Once Phase 1 ore production commences in Q3 2024, mining will focus on the higher-grade area approximately 450 metres from Shaft 1 (Figure 14), requiring less underground infrastructure to access.

Figure 14: Underground mine layout of initial development.

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115055_dc4a96bb34cc28e8_027full.jpg

Figure by Ivanhoe, 2022.

During Phase 2, primary access to the mine will be by way of a 1,104-metre-deep, 10-metre-diameter production shaft (Shaft 2). Secondary access to the mine will be via the 996-metre-deep, 7.25-metre-diameter ventilation shaft (Shaft 1). During mine production, both shafts also will serve as ventilation intakes. During Phase 2, ore will be hauled from the stopes to a series of internal ore passes and fed to the bottom of Shaft 2, where it will be crushed and hoisted to surface.

Conventional metallurgical flowsheet for Phase 1 and 2

Metallurgical testwork has focused on maximizing recovery of platinum-group elements (PGE) and base metals (mainly nickel) while producing an acceptably high-grade concentrate suitable for further processing and/or sale to a third party. The three main geo-metallurgical units and composites tested produced smelter-grade final concentrates averaging 85 g/t PGE+Au, at acceptable PGE recoveries. Testwork also has shown that the material is amenable to treatment by conventional flotation without the need for mainstream or concentrate re-grinding. Extensive bench-scale testwork comprising of open-circuit and locked-cycled flotation testing, comminution testing, mineralogical characterization, tailings dewatering, and rheological characterization was performed at Mintek of South Africa, an internationally accredited metallurgical testing facility and laboratory.

Comminution and flotation testwork have indicated that the optimum grind for beneficiation is 80% passing 75 micrometres. Platreef ore is classified as being "hard" to "very hard", and thus not suitable for semi-autogenous grinding; a multi-stage crushing and ball-milling circuit has been selected as the preferred size reduction method.

Improved flotation performance has been achieved using high-chrome grinding media, as opposed to carbon steel media. The inclusion of a split-cleaner flotation circuit configuration, in which the fast-floating fraction is treated in a cleaner circuit separate from the medium- and slow-floating fractions, resulted in improved PGE, copper and nickel recoveries and concentrate grades.

A phased development approach was adopted for the flow-sheet design in the 2022 Feasibility Study. Phase 1 comprises a stand-alone concentrator with a design capacity of 770 ktpa. Phase 2 comprises an additional two 2.2-Mtpa modules, which will be constructed sequentially to meet the mine ramp-up schedule.

Both Phase 1 and Phase 2 flowsheets incorporate a three-stage crushing circuit, feeding crushed material to the milling and flotation modules. Flotation is followed by concentrate thickening, concentrate filtration, tailings handling and tailings disposal facility. It is expected that plant performance over life-of-mine will achieve 3PGE+Au recovery of 86% at a concentrate grade averaging 85 g/t 3PGE+Au.

Members of the Orion Mine Finance and Nomad Royalty teams, with members of Platreef's mine development team, on the top platform of the Shaft 1 headgear.

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115055_dc4a96bb34cc28e8_028full.jpg

Kgalalelo Tladi, Chief Safety Officer, conducting a safety inspection of the Shaft 1 underground equipping stage.

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115055_dc4a96bb34cc28e8_029full.jpg

Sustainable, dry stacking tailings storage methodology

The tailings storage facility (TSF) design in the 2022 Feasibility Study is based on the dry stack methodology. Previously, a hybrid paddock deposition methodology was considered; however, Ivanplats opted to change the TSF deposition methodology from conventional upstream design to dry stacking, which has numerous benefits.

Dry stacking facilities are deemed to be inherently safer, as there is no hydraulic deposition; hence, in the unlikely event of a catastrophic failure, the risk of flooding the surrounding areas with tailings will be minimal. Stacked tailing storage facilities also are more water efficient in that most of the water in the tailings is captured in the dewatering plant, pumped directly back to the concentrator and re-used within the process.

During the 2022 Feasibility Study mine life, approximately 53 million tonnes of tailings will be stored in the dry stack TSF, with the remainder of the tailings (approximately 60% overall) to be used as backfill in the underground mine, further reducing the project footprint.

The TSF design also caters for a potential future expansion to 8-Mtpa production capacity, to be explored in future studies.

It is envisaged to use the approved rock-dump footprint within the immediate Platreef mine and concentrator areas as a dry stacking tailings facility during Phase 1. Golder Associates currently is performing the design work to apply for the relevant licences and/or amendments to the existing authorizations.

Ivanplats signs new agreement to provide local, treated water for Platreef's Phase 1 and 2 operations; supply of electricity also secured

The water requirement for the Phase 1 operation is projected to peak at approximately three million litres per day, which will then increase to nine million litres per day once the Phase 2 expansion is complete. On January 17, 2022, Ivanhoe announced the signing of new agreements for the rights to receive local, treated water to supply the bulk water needed for the phased development plan at Platreef. These agreements replace those originally signed in 2018.

Under the terms of a new offtake agreement, the Mogalakwena Local Municipality (MLM) has agreed to supply at least three million litres per day of treated effluent, up to a maximum of 10 million litres per day for 32 years, from the date of first production, sourced from the town of Mokopane's Masodi Waste Water Treatment Works, currently under construction.

Ivanplats also has signed a sponsorship agreement where Ivanplats has undertaken the commitment to complete the partially constructed Masodi Waste Water Treatment Works, which was halted in 2018. Ivanplats anticipates spending approximately ZAR 215 million (US$14 million) to complete the works, whereby Ivanplats' financial contribution will take the form of a sponsorship in favour of the municipality. Ivanplats will purchase the treated water at a reduced rate of ZAR 5 per thousand litres. Arrangements are underway to re-commence the construction works in Q3 2022, which are scheduled to take approximately 18 months.

On February 24, 2017, the 5 million-volt-ampere (MVA) electrical power line connecting the Platreef site to the Eskom public electricity utility was energized and now is supplying electricity to Platreef for shaft equipping and construction activities.

Ivanplats has reached an agreement with Eskom for the supply of a total of 100 MVA of power, which represents Platreef's electrical power requirement for the full Phase 2 mine, concentrator and associated infrastructure. As part of the 2022 Feasibility Study, Ivanhoe negotiated the load build-up with Eskom to cater for Phase 1's construction requirement of up to 8 MVA, Phase 1's production requirement of 25 MVA and later ramping up to 100 MVA for Phase 2.

Ivanplats opted for a self-build, with the construction contract awarded. The construction of the 2 X 27km Overhead lines for the 100MVA power supply commenced in November 2021. The contractors site establishment is completed, with bush clearing, and soil nomination tests under way, for the structure foundations.

Ivanplats arranges offtake for Platreef's Phase 1 production; evaluating options for Phase 2

Ivanplats recently signed documents relating to offtake for 100% of Phase 1's PGM concentrate production of approximately 40,000 tonnes per year, based on standard commercial terms for PGM mines in South Africa. The ability to place Phase 1 PGM concentrate reflects its high quality, which contains six payable metals including palladium, rhodium, platinum, nickel, copper and gold.

The offtake arrangements are with Northam Platinum Limited and Heron Metals Pty Ltd., a joint venture in which Trafigura Pte. Ltd. ("Trafigura"), a Singaporean registered company, has a majority shareholding. Northam Platinum is an independent, fully empowered, integrated PGM producer, with primary operations in South Africa including the wholly owned Zondereinde Mine and metallurgical complex, and Booysendal Mine. The Trafigura Group is one of the world's leading independent commodity trading and logistics houses.

The terms of the proposed offtake with Heron Metals / Trafigura are based on a non-binding indicative term sheet and are subject to negotiation and execution of definitive documentation for a concentrate sales agreement.

Ivanplats is evaluating alternatives for the processing of concentrate production during Phase 2, from 2028 onwards. This includes placing concentrates with smelters in South Africa or elsewhere, where additional capacity is expected to become available by the time steady-state production is achieved. Ivanplats is also considering standalone downstream processing options, including both conventional smelting and refining, and hydrometallurgical processes.

Shaft 1 changeover nearing completion with Shaft 2 early works underway

The construction of the 996-metre-level station at the bottom of Shaft 1 was completed in July 2020. Shaft 1 initially will be used to access the orebody and is approximately 450 metres away from a high-grade area of Flatreef that is planned for mining in Phase 1. The three development stations that will provide initial, underground access to the high-grade orebody also have been completed on the 750-, 850-, and 950-metre levels.

Shaft equipping commenced in May 2021 and remains on track to be completed in March 2022. Following the completion of the changeover work in the shaft, underground stations, and establishment of the ore and waste passes, lateral underground mine development will commence toward high-grade ore zones.

Lateral mine development on the 950-metre level toward the Flatreef orebody is expected to begin in Q2 2022. The initial development will use battery electric M2C drill rigs and 14-tonne load haul dumpers being manufactured by Epiroc, a leading mining equipment manufacturer, at its facilities in Örebro, Sweden. The partnership with Epiroc for emissions-free mining equipment is an important first step toward reducing the carbon footprint of the mine, with learnings to be applied across Ivanhoe Mines' operations. The battery electric mining fleet is expected to arrive on site in March 2022.

The contract for the initial mine development has been adjudicated and is in the final stages of negotiation. Newly designed rock chutes on surface will connect the conveyors feeding the concentrator plant and the waste rock area; from there the waste rock will be crushed and used as cemented backfill underground for maximum ore extraction, as well as for protection berms to contain storm water and reduce noise emissions.

Pilot drilling of the first main ventilation shaft will commence in Q2 2022, after which it will be reamed to its final diameter of 5.1 metres, providing the main return airway for the Phase 1 development. On completion, this ventilation shaft also will serve as a second egress from the mine.

Early-works surface construction for Shaft 2, including the excavation of a surface box-cut to a depth of approximately 29 metres below surface and construction of the concrete hitch for the 103-metre-tall concrete headframe, have been completed. The Shaft 2 headframe construction, from the hitch to the collar level, is progressing well with the third and fourth headgear lifts well advanced. Ten civil lifts are to be constructed in total, including a ventilation plenum and personnel access tunnel, with targeted completion in May 2022.

Phillip Ramphisa, Platreef's Environmental Manager, Business Sustainability, analyzing project water samples. Ivanhoe Mines is committed to responsible water use at all its projects in support of the United Nations' Sustainable Development Goals.

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115055_dc4a96bb34cc28e8_030full.jpg

Development of human resources and job skills

Current and future human resource development at the Platreef Project is one of the largest contributors to the sustainable development of the project. Ivanplats has a commitment and dedication to being a Mine of the Future and an employer of choice, underpinned by excellence, and overseen by strategic and valuable recruitment, human resource development and workplace safety programs, among others. The Platreef Project's first five-year Social and Labour Plan (SLP) contributed R67 million (US$4 million) for the development of job skills among local residents.

Implementation of the second SLP currently is underway, through which Ivanplats plans to build on the foundation laid in the first SLP and continue with its training and development suite, which includes 15 new mentors, internal skills training for 78 staff members, a legends program to prepare retiring employees with new/other skills, community adult education training for host community members, core technical skills training for at least 100 community members, portable skills, and more.

Local economic development projects will contribute to community water source development with the Mogalakwena Municipality boreholes program, educational program in partnership with Department of Education, and significant funding for sanitation infrastructure at the municipality. The refurbishment and equipping of a health clinic in Tshamahansi Village, which will be conducted in partnership with other parties, will enable better access to health services for local residents.

Ivanplats proudly launched its first cadetship program, providing opportunities to 50 local youths every year. The program seeks to enhance gender diversity, with 54% of the students being female; and offers these cadets, who are scheduled to graduate in March, a national certificate in health and safety, as well as mining competencies, such as utility vehicle operations.

Chuene Matlala, Platreef's Senior Project Officer, responsible for the implementation of local economic development initiatives as part of the project's Social Labour Plan.

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115055_dc4a96bb34cc28e8_031full.jpg

Hendrietta Sarila, Project Geologist and Environmental Management Coordinator and Chairperson of the Women in Mining Committee, at the Platreef Project, a member of Deloitte's Women in Mining Class of 2021.

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/3396/115055_dc4a96bb34cc28e8_032full.jpg

Ivanplats draws down initial US$75-million tranche of US$300 million streaming facilities; financing focus now on securing US$120 million in senior debt

Ivanplats recently concluded stream-financing agreements for a US$200 million gold-streaming facility and a US$100 million palladium- and platinum-streaming facility, which will fund a large portion of the Phase 1 capital costs, with initial production scheduled in 2024. The stream facilities are to be drawn in two tranches, with the first tranche of US$75 million drawn in December 2021, and the second tranche of US$225 million to be drawn upon satisfaction of certain conditions precedent.

The conclusion of the stream-financing agreements allows Ivanplats to focus efforts on finalizing the senior debt facility for up to US$120 million. Both the gold stream facility and palladium and platinum stream facility will be subordinated to any senior secured financing.

The senior debt facility is anticipated to be used only after the stream facilities are fully drawn. Ivanplats remains flexible to raise additional capital at a later date.

Future expansion options

The 2022 Feasibility Study considers Platreef's Phase 1 and Phase 2 development, including only one third of the Indicated Resources above an US$80/t NSR cut-off. If the remainder of the Indicated Resources were to be converted to Mineral Reserves, it would provide an opportunity to significantly expand production.

The full indicated and inferred resource base at Platreef may support additional expansions and larger production capacity. As development and stoping continues, an infill drilling program from underground is recommended to increase confidence and potentially expand the resource base, which would underpin future studies on further mine expansions.

Qualified persons

The 2022 Feasibility Study and Technical Report has been prepared by:

- OreWin of Adelaide, Australia - Overall report preparation and economic analysis, Mineral Reserve estimation and mine plan.

- Mine Technical Services of Nevada, USA - Mineral Resource estimation.

- SRK Consulting of Johannesburg, South Africa - Mine geotechnical recommendations.

- DRA Global of Johannesburg, South Africa - Process and infrastructure.

- Golder Associates Africa of Midrand, South Africa - Water and tailings management.

The independent qualified persons responsible for preparing the Platreef 2022 Feasibility Study, on which the technical report will be based, are Bernard Peters (OreWin); Curtis Smith (OreWin); Timothy Kuhl (Mine Technical Services); William Joughin (SRK); Val Coetzee (DRA Global); and Riaan Thysse (Golder Associates). Each qualified person has reviewed and approved the information in this news release relevant to the portion of the Platreef 2022 Feasibility Study for which they are responsible.

Other scientific and technical information in this news release has been reviewed and approved by Stephen Torr, P.Geo., Ivanhoe Mines' Vice President, Project Geology and Evaluation, a Qualified Person under the terms of NI 43-101. Mr. Torr is not considered independent under NI 43-101 as he is the Vice President, Project Geology and Evaluation of Ivanhoe Mines. Mr. Torr has verified the technical data disclosed in this news release.

Sample preparation, analyzes, and security

During Ivanhoe's work programs, sample preparation and analyses were performed by accredited independent laboratories. Sample preparation is accomplished by Set Point laboratories in Mokopane. Sample analyses have been accomplished by Set Point Laboratories in Johannesburg, Lakefield Laboratory (now part of the SGS Group) in Johannesburg, Ultra Trace Laboratory in Perth, Genalysis Laboratories in Perth and Johannesburg, SGS Metallurgical Services in South Africa, Acme in Vancouver, and ALS Chemex in Vancouver. Bureau Veritas Minerals Pty Ltd assumed control of Ultra Trace during June 2007 and is responsible for assay results after that date.

Sample preparation and analytical procedures for samples that support Mineral Resource estimation have followed similar protocols since 2001. The preparation and analytical procedures are in line with industry-standard methods for platinum, palladium, gold, copper and nickel deposits. Drill programmes included insertion of blank, duplicate, standard reference material (SRM), and certified reference material (CRM) samples. The quality assurance and quality control (QA/QC) program results do not indicate any problems with the analytical protocols that would preclude use of the data in Mineral Resource estimation.

Sample security has been demonstrated by the fact that the samples were always attended or locked in the on-site core facility in Mokopane.

Information on sample preparation, analyses and security will be contained in the Technical Report to be filed on SEDAR at www.sedar.com within 45 days of this news release, and which will be made available on the Ivanhoe Mines website at www.ivanhoemines.com.

About Ivanhoe Mines

Ivanhoe Mines is a Canadian mining company focused on advancing its three principal projects in Southern Africa: the development of major new, mechanized, underground mines at the Kamoa-Kakula copper discoveries in the Democratic Republic of Congo and at the Platreef palladium-rhodium-platinum-nickel-copper-gold discovery in South Africa; and the extensive redevelopment and upgrading of the historic Kipushi zinc-copper-germanium-silver mine, also in the Democratic Republic of Congo.

Kamoa-Kakula began producing copper concentrates in May 2021 and, through phased expansions, is positioned to become one of the world's largest copper producers. Kamoa-Kakula is being powered by clean, renewable hydro-generated electricity and is projected to be among the world's lowest greenhouse gas emitters per unit of metal produced. Ivanhoe Mines has pledged to achieve net-zero operational greenhouse gas emissions (Scope 1 and 2) at the Kamoa-Kakula Copper Mine. Ivanhoe also is exploring for new copper discoveries on its Western Foreland exploration licences in the Democratic Republic of Congo, near the Kamoa-Kakula Project.

Information contacts

Investors: Bill Trenaman +1.604.331.9834 / Media: Matthew Keevil +1.604.558.1034

Cautionary statement on forward-looking information

Certain statements in this news release constitute "forward-looking statements" or "forward-looking information" within the meaning of applicable securities laws. Such statements involve known and unknown risks, uncertainties and other factors, which may cause actual results, performance or achievements of the company, the Platreef Project, or industry results, to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements or information. Such statements can be identified by the use of words such as "may", "would", "could", "will", "intend", "expect", "believe", "plan", "anticipate", "estimate", "scheduled", "forecast", "predict" and other similar terminology, or state that certain actions, events or results "may", "could", "would", "might" or "will" be taken, occur or be achieved. These statements reflect the company's current expectations regarding future events, performance and results, and speak only as of the date of this news release.

The forward-looking statements and forward-looking information in this news release include without limitation, statements that (i) the Phase 1 mine is advancing towards first production in Q3 2024; (ii) Shaft 2 commissioning is accelerated to 2027; (iii) Phase 2 annual forecast production is more than 590,000 ounces of palladium, platinum, rhodium and gold, plus more than 40 million pounds of nickel and copper; (iv) Platreef is to have a cash cost of US$514 per ounce 3PE + AU; (v) changeover of Shaft 1 to a production shaft is expected to be completed in March 2022; (vi) earthworks for the first concentrator is planned to begin in Q2 2022; (vii) civil works and ordering of long lead items is planned for H2 2022; (viii) rock hoisting is to commence in Q2 2022; (ix) two 2.2 Mtpa concentrator modules will be commissioned in 2028 and 2029 once Shaft 2 is complete; (x) steady state production in Phase 2 is 5.2 Mtpa; (xi) the re-commencement of construction of the Masodi Waste Water Treatment is expected to begin in Q3 2022, and construction is expected to take approximately 18 months; (xii) lateral mine development is expected to begin on the 950-metre level in Q2 2022; (xiii) the battery electric mining fleet is expected to arrive at Platreef in March 2022; and (xiv) the senior debt facility of US$120 million is anticipated to be used only after the stream facilities are fully drawn; (xv) Platreef is projected to become one of the world's largest and lowest-cost producers of palladium, platinum, rhodium, nickel, copper and gold.

In addition, all of the results of the Platreef 2022 Feasibility Study constitute forward-looking statements and forward-looking information. The forward-looking statements include metal price assumptions, cash flow forecasts, projected capital and operating costs, metal recoveries, mine life and production rates, and the financial results of the Platreef 2022 Feasibility Study. These include estimates of internal rates of return after-tax of 18.5% at long term consensus metal prices and 29.3% at spot metal prices with payback periods of 7.9 years and 6.6 years respectively; net present values at an 8% discount rate of US$1.7 billion at long term consensus metal prices and US$4.1 billion at spot metal prices; future production forecasts and projects, including average annual production of 590koz 3PE+Au; estimates of net total cash cost, net of copper and nickel by-product credits and including sustaining capital costs of US$514/oz; mine life estimates, including a 28.3 year mine life; initial capital costs of US$448 million and US$1.5 billion for expansion capital costs; Phase 1 average annual production of 113,000 ounces of 3PE + Au; cash flow forecasts; estimates of 3PE+Au recoveries of 86%. Readers are cautioned that actual results may vary from those presented.

All such forward-looking information and statements are based on certain assumptions and analyses made by Ivanhoe Mines' management in light of their experience and perception of historical trends, current conditions and expected future developments, as well as other factors management believe are appropriate in the circumstances. These statements, however, are subject to a variety of risks and uncertainties and other factors that could cause actual events or results to differ materially from those projected in the forward-looking information or statements including, but not limited to, unexpected changes in laws, rules or regulations, or their enforcement by applicable authorities; the failure of parties to contracts to perform as agreed; social or labour unrest; changes in commodity prices; unexpected failure or inadequacy of infrastructure, industrial accidents or machinery failure (including of shaft sinking equipment), or delays in the development of infrastructure, and the failure of exploration programs or other studies to deliver anticipated results or results that would justify and support continued studies, development or operations. Other important factors that could cause actual results to differ from these forward-looking statements also include those described under the heading "Risk Factors" in the company's most recently filed MD&A as well as in the most recent Annual Information Form filed by Ivanhoe Mines. Readers are cautioned not to place undue reliance on forward-looking information or statements. Certain of the factors and assumptions used to develop the forward-looking information and statements, and certain of the risks that could cause the actual results to differ materially are presented in technical reports available on SEDAR at www.sedar.com and on the Ivanhoe Mines website at www.ivanhoemines.com.

This news release also contains references to estimates of Mineral Resources and Mineral Reserves. The estimation of Mineral Resources and Mineral Reserves is inherently uncertain and involves subjective judgments about many relevant factors. Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability. The accuracy of any such estimates is a function of the quantity and quality of available data, and of the assumptions made and judgments used in engineering and geological interpretation, which may prove to be unreliable and depend, to a certain extent, upon the analysis of drilling results and statistical inferences that may ultimately prove to be inaccurate. Mineral Resource or Mineral Reserve estimates may have to be re-estimated based on, among other things: (i) fluctuations in platinum, palladium, gold, rhodium, copper, nickel or other mineral prices; (ii) results of drilling; (iii) results of metallurgical testing and other studies; (iv) changes to proposed mining operations, including dilution; (v) the evaluation of mine plans subsequent to the date of any estimates; and (vi) the possible failure to receive required permits, approvals and licences.

Although the forward-looking statements contained in this news release are based upon what management of the company believes are reasonable assumptions, the company cannot assure investors that actual results will be consistent with these forward-looking statements. These forward-looking statements are made as of the date of this news release and are expressly qualified in their entirety by this cautionary statement. Subject to applicable securities laws, the company does not assume any obligation to update or revise the forward-looking statements contained herein to reflect events or circumstances occurring after the date of this news release.

To view the source version of this press release, please visit https://www.newsfilecorp.com/release/115055