The Conversation (0)

With a strong foothold in the manufacturing and distribution of copper-insulated cables, Australia-based Energy Technologies (ASX:EGY) is poised to capitalize on the growing renewable energy sector through strategic global partnerships presenting a compelling investment opportunity. The company''s wholly owned subsidiary, Bambach Wires and Cables, is the oldest cable manufacturer in Australia, and its extensive history underpins a reputation for reliability and quality.

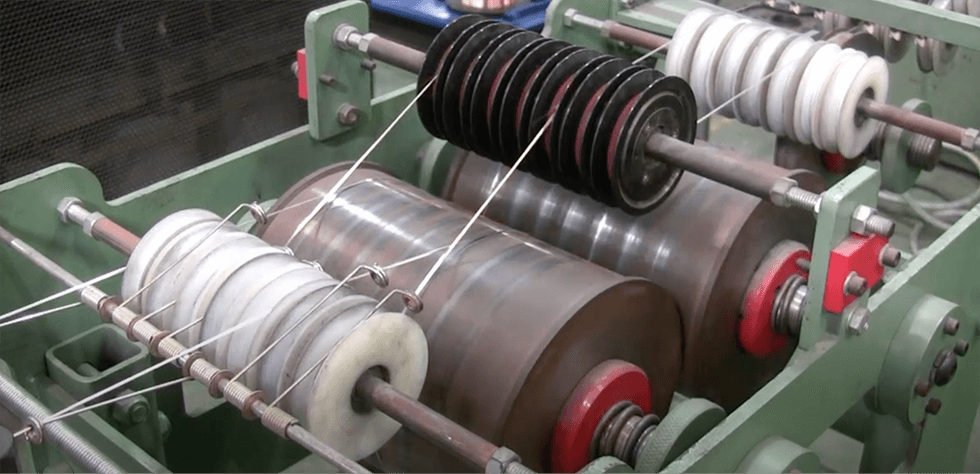

Energy Technologies focuses its factory operations on higher-margin product lines while employing a balanced strategy of manufacturing and purchasing cables for sale. Its Rosedale facility is a significant upgrade in its manufacturing capabilities equipped with a high level of automation that supports production efficiency, processing up to 250 tonnes of copper monthly, with room for additional capacity if demand rises.

Energy Technologies also engages in purchased sales by sourcing lower-margin products from rigorously vetted suppliers throughout the globe. This approach ensures Energy Technologies can meet market demand without overextending its manufacturing resources. Purchased sales for FY25 are projected to contribute an additional AU$6.7 million to the company’s revenue.

This Energy Technologies profile is part of a paid investor education campaign.*

Click here to connect with Energy Technologies (ASX:EGY) to receive an Investor Presentation