The Conversation (0)

HIGHLIGHTS

“It is very exciting to have the Category four (4) exploration approval granted enabling our geology team to immediately commence field works in preparation for drilling. This once again demonstrates the positive operating environment in Kazakhstan and the support the company is enjoying”.

Initial Geological Work Program

The initial geological program will undertake tenement wide mapping and soil sampling focusing on verification of historical shallow high-grade results and identify the extent of the surface outcropping and shallow high-grade uranium across the tenement.

The geology team will be utilising a handheld XRF unit in the field providing real time geological information to the team and valuable geological data that will assist with the Initial drill hole targeting and methodology.

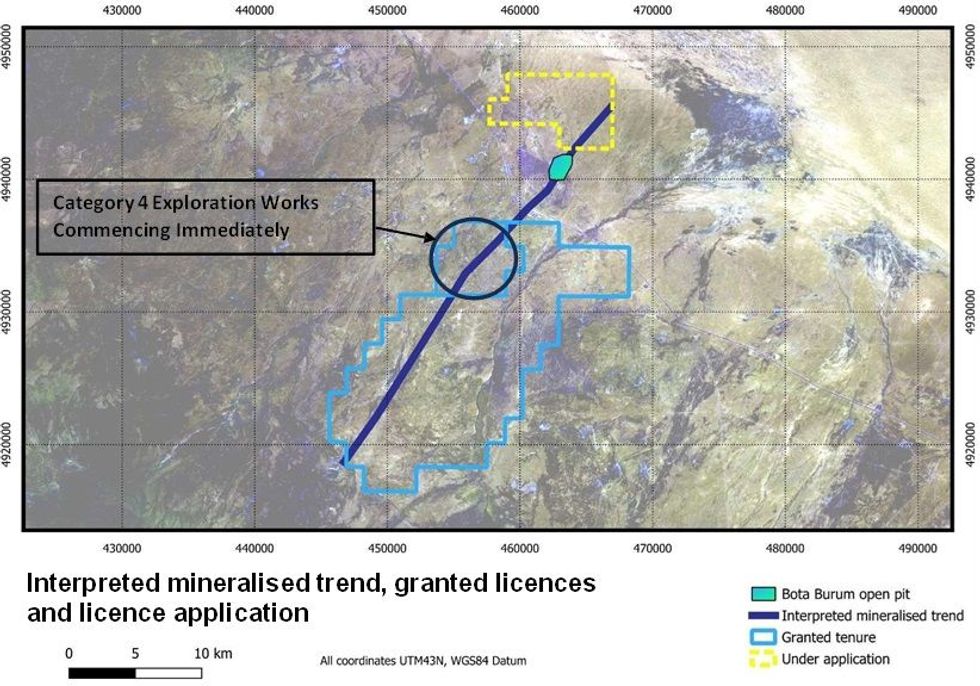

Figure 1 below shows the interpreted mineralised uranium trend1 and location for initial Category 4 exploration works.

Figure 1 – The interpreted mineralised Uranium trend & location for initial Category 4 exploration works.

Figure 1 – The interpreted mineralised Uranium trend & location for initial Category 4 exploration works.

Click here for the full ASX Release

This article includes content from C29 Metals Limited, licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.