The Conversation (0)

In its recent coverage of Metals Australia Limited (ASX:MLS), Australian analyst firm Vested Equities’ has given Metals Australia a valuation of approximately 4.7 cents per share, reflecting a compelling proposition. This valuation, based on a comparative assessment of graphite peers and the intrinsic value of the Lac Rainy resource, does not yet account for the full potential of the company's expansive exploration portfolio, the Vested report indicates. With the anticipation of further exploration unlocking substantial value, Metals Australia presents an attractive investment opportunity with significant upside potential, it adds.

Metals Australia stands out as a formidable player in the battery minerals sector with its robust portfolio of exploration and development projects. Strategically situated in the premier mining jurisdictions of Quebec, Canada and Western Australia, MLS showcases a suite of projects rich in sought-after battery metals such as lithium and graphite. Amidst China's tightening graphite export controls, MLS's assets gain geostrategic importance, offering a non-Chinese source of premium battery-grade graphite crucial for the North American lithium-ion/EV battery market.

“Metals Australia Limited is strategically positioned to experience a re-rating of its share price, driven by a confluence of catalysts,” the report states, citing MLS's strategic positioning, resource base and proactive management team as collectively form a compelling investment narrative.

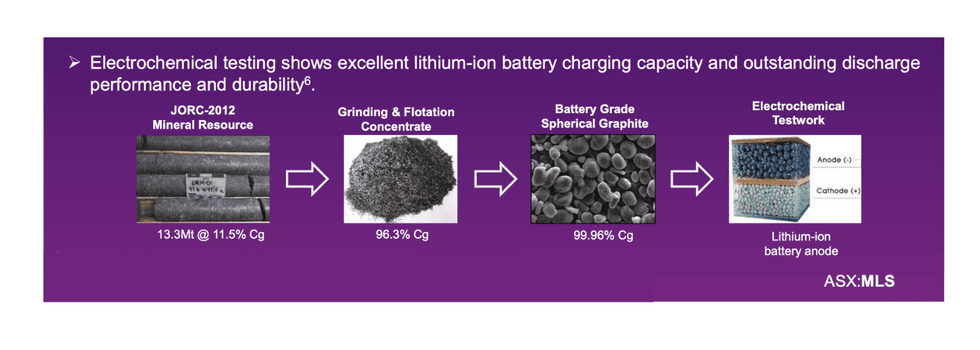

Lac Carheil (formerly Lac Rainy) flake-graphite to battery anode flow sheet.

Lac Carheil (formerly Lac Rainy) flake-graphite to battery anode flow sheet.

Report Highlights:

- The Lac Rainy project, a cornerstone of MLS's portfolio, boasts a JORC 2012 Mineral Resource of 13.3 million tons at 11.5 percent graphitic carbon. This includes a high-grade indicated resource and an inferred resource with significant economic potential confirmed by a completed scoping study. With recent contracts aimed at expanding and enhancing the resource, alongside plans for a flake graphite concentrate plant, the project's potential is yet to be fully tapped, promising substantial upside.

- Aggressive exploration programs for lithium and gold. The discovery of a new LCT pegmatite within the Corvette South Lithium trend in Quebec, parallels the significant findings by Patriot Battery. This, along with the gold prospects in the southeastern tenements and the lithium-bearing pegmatites in the Manindi project, highlight the company's dynamic exploration strategy. Furthermore, the acquisition of copper and gold tenements through Payne Gully Gold adds another layer of prospective value to the company's assets.

- The leadership of MLS, with the recent appointment of CEO Paul Ferguson, is poised to leverage extensive industry experience to accelerate the exploration and development activities. The company's financial health is robust, with cash reserves surpassing its market capitalization, indicating a strong financial position to sustain its ambitious growth plans.

Click here for the full report

This content is intended only for persons who reside or access the website in jurisdictions with securities and other applicable laws which permit the distribution and consumption of this content and whose local law recognizes the scope and effect of this Disclaimer, its limitation of liability, and the legal effect of its exclusive jurisdiction and governing law provisions [link to Governing Law section of the Disclaimer page].

Any investment information contained on this website, including third party research reports, are provided strictly for informational purposes, are general in nature and not tailored for the specific needs of any person, and are not a solicitation or recommendation to purchase or sell a security or intended to provide investment advice. Readers are cautioned to seek the advice of a registered investment advisor regarding the appropriateness of investing in any securities or investment strategies mentioned on this website.

MLS:AU

Alert Options

No alert set