The Conversation (0)

Octava Minerals Limited (ASX:OCT) (“Octava” or the “Company”), a Western Australia focused explorer of the new energy metals antimony, REE’s, Lithium and gold, is pleased to report that detailed geophysics over the 10km antimony corridor at Yallalong is now complete and final data has been processed and interpreted.

Highlights

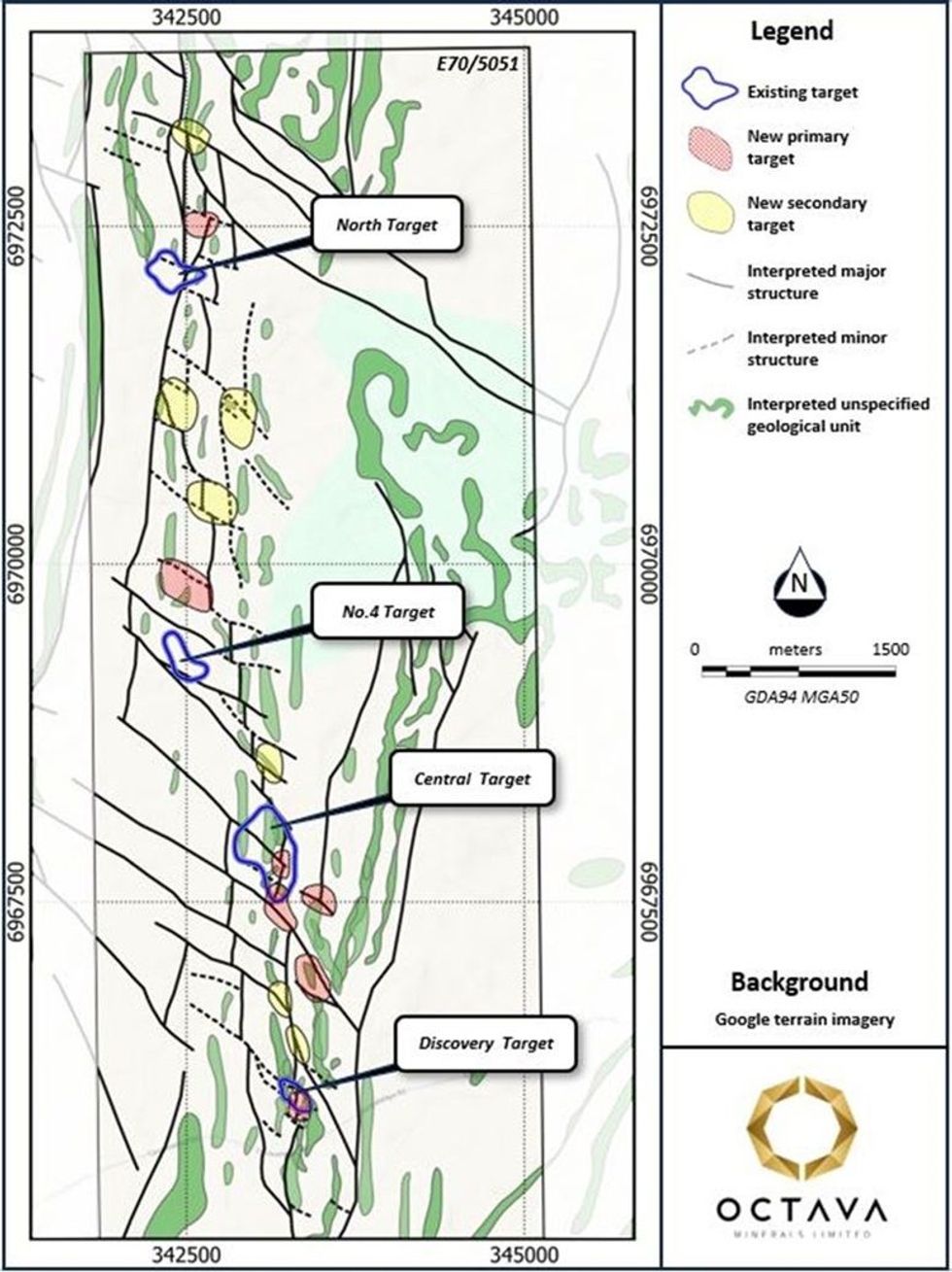

The geophysics has identified 14 new structural antimony targets at Yallalong analogous to the Discovery Target, where historic drilling intercepted high-grade antimony.

Octava’s Managing Director Bevan Wakelam stated, "The new gravity data redefines the exploration model for high grade antimony at Yallalong. It explains the presence of anomalous antimony along the structural corridor and predicts potential hot spots along it. It is exciting to consider the possibility of a continuous system extending under cover for more than 10 kilometers and having a method to pinpoint the most prospective zones. Planning work is already underway for drilling of these new targets "

Antimony

The Yallalong project is located ~ 220km to the northeast of the port town of Geraldton in Western Australia. The antimony (Sb) mineralisation identified at Yallalong appears within a 10km north- south striking mineralised corridor.

Previous exploration identified four principal antimony targets where antimony mineralisation was exposed at surface. Only the Discovery Prospect had previous drilling and recorded high-grade antimony intercepts over a strike length of ~300m, including 7m @ 3.27% Sb.

A detailed geophysical survey was undertaken to identify underlying structures, such as shears and faults, which act as conduits to mineralising fluids. It also outlines key lithological boundaries. These factors are important in the formation of antimony deposits worldwide.

Interpretation of the geophysical data and the historic drilling has re-defined the exploration model for high grade antimony at Yallalong. Fourteen new targets analogous to the Discovery Target have been identified and will be evaluated through planned drilling. See Figure 1.

Figure 1. Summary structural interpretation and with existing and newly identified Sb targets at Yallalong.

Figure 1. Summary structural interpretation and with existing and newly identified Sb targets at Yallalong.

Atlas Geophysics conducted the gravity survey using a 100m x 100m grid pattern, with additional measurements on a 50m x 50m grid over the Discovery Target. NewGen Geo, a geophysical consultancy, carried out the gravity data processing and interpretation.

Click here for the full ASX Release

This article includes content from Octava Minerals Limited, licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.