The Conversation (0)

Metals Australia Ltd (ASX: MLS) continues to make significant progress advancing its flagship Lac Carheil high-grade flake-graphite development project in the Tier 1 global mining province of Quebec, including:

In addition to the advancements being made by the Company, the strategic value of the Lac Carheil high- grade flake-graphite project stands to be significantly enhanced from the outcome of a 30-day consultation period announced by the Canadian Government on August 26th 2024 (September 10 to October 10, 2024) seeking inputs on the potential application of a surtax on a range of Chinese imports related to critical manufacturing sectors, including critical minerals.

This follows the imposition of a 100% surtax on Chinese-made EVs due to come into effect on October 1, 2024, and a 25% surtax on imports of steel and aluminium from China, effective October 15, 2024. Lac Carheil’s strategic significance is also linked directly to, and referenced in, Quebec’s Plan for The Development of Strategic Minerals5 (2020-2025).

Based on its reviews of the projects outlined in the above plan, Metals Australia is unaware of any graphite projects actively progressing in Canada that have both the resource grade and upside potential that Lac Carheil exhibits.

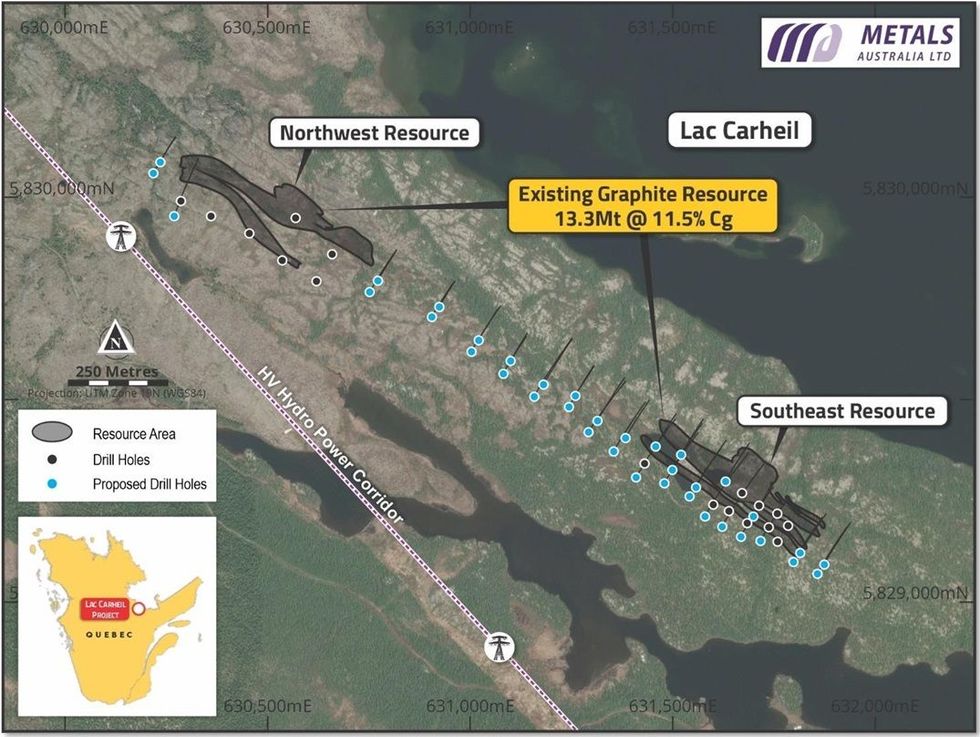

Figure 1 - Lac Carheil Graphite Project – Existing Mineral Resource Locations2 (grey shading / black hole positions) & planned resource extension and infill drilling (blue holes). Location of Quebec Hydro High Voltage Powerline Corridor (dashed line) & general topography.

Figure 1 - Lac Carheil Graphite Project – Existing Mineral Resource Locations2 (grey shading / black hole positions) & planned resource extension and infill drilling (blue holes). Location of Quebec Hydro High Voltage Powerline Corridor (dashed line) & general topography.

Metals Australia CEO Paul Ferguson commented:

“We are delighted to report progress on multiple fronts at Lac Carheil as we continue to advance our flagship high- grade flake-graphite project in Quebec to Pre-Feasibility Study status.

This progress comes as we wrap up our phase one field exploration program at our Corvette River project in Canada, where we expect to receive assay results later this month, and the recent launch of aggressive exploration programs across our three Australian gold and critical minerals projects – Warrambie, Big Bell North and Warrego East.

Over the last couple of weeks, I have had the pleasure of engaging in person with a broad range of stakeholders on country in Ontario and Quebec regarding the development of Lac Carheil. The very clear message from those discussions is that our project is rapidly developing a profile as one of the best graphite projects advancing in North America today.

Earlier this week, the Lac Carheil project received a further potential tailwind when Canada’s Department of Finance launched a 30-day consultation process on a range of potential new surtaxes, including on critical minerals, in response to what it claimed were unfair Chinese trade practices. The Government has already shown its teeth on this issue by imposing a 100% surtax on all Chinese-made EVs, effective October 1, 2024, and a 25% surtax on imports of steel and aluminium, effective October 15, 2024.

Our project can contribute to forecasted shortfalls of graphite required to meet national and homeland security requirements across North America. This future stands in stark contrast to the state of domestic market supply for graphite in North America today. There is extremely limited onshore production of graphite in North America. Nearly all graphite used in the growing North American battery industry is sourced from offshore jurisdictions. This places Lac Carheil as a project of strategic importance for a domestic supply of high-quality graphite. This is essential for securing the supply chain certainty required for the clean energy transition.

The work we committed to completing as part of our planned PFS is rapidly advancing. Comprehensive metallurgical test work for the PFS level flowsheet design of the planned 100,000 tonnes per annum concentrate plant is well progressed – as are the plant designs for the concentrate plant. We are very close to dispatching the bulk concentrate sample to Germany that will launch the downstream design phase of the project, on schedule.

The design work to date has also given rise to a prioritised list of follow-up projects that we intend to further refine and progress as we move from PFS level studies and into the Feasibility Study design. We have held discussions related to grant funding avenues in Canada, including in Quebec, and in the USA, with funding applications made and more to follow. The work we are proposing is innovative and the solutions to be generated match well with the criteria set by governments for grant funding.

While our recent endeavours have focused heavily on the engineering and scientific elements of design, we are cognizant of our need to engage broadly with stakeholders and communities to ensure we understand their concerns, identify solutions as we look to establish enduring partnerships with those communities and stakeholders.

In that regard, a large focus of my recent trip was spent engaging with government at the provincial and local levels and speaking with stakeholders, including existing and prospective service providers, First Nations economic development groups and to seek further meetings with governments and First Nations communities. I was appreciative of the many groups we were able to speak with face to face and to those who have committed to follow up discussions.

As a board and management team, we remain dedicated to collaborating with all stakeholders to develop this strategically significant project for the betterment of all.”

Click here for the full ASX Release

This article includes content from Metals Australia Ltd, licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.