The Conversation (0)

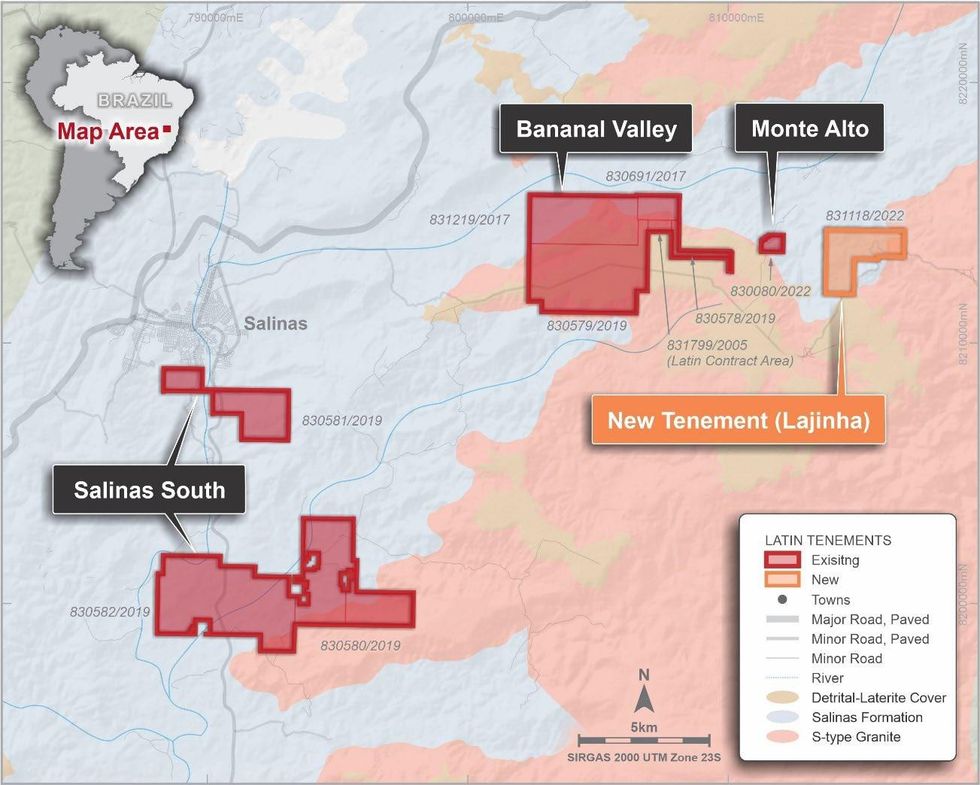

Latin Resources Limited (ASX: LRS) (“Latin” or “the Company”) is pleased to announce it has secured, through its newly created 100% wholly owned subsidiary Belo Lithium Mineracao Ltda. (“Belo”), an additional highly prospective tenement to grow the Company’s Salinas Lithium Project in Brazil (“Salinas” or the “Project”), expanding its footprint at the project to the east (Figure 1) to cover additional strike extensions of the regional prospective host stratigraphy.

HIGHLIGHTS

Latin has secured an exclusive and binding 24-month option agreement (“Option” or “Agreement”), over the new concession in the Bananal Valley (831.118/2008) from Mineracao Salinas Ltda. (the “Vendor”), whereby Latin may acquire a 100% interest in this tenement to the east of the Company’s existing Bananal Valley Project. The Lajinha tenement is highly prospective, with known outcropping spodumene bearing pegmatites, and this addition expands Latin’s strategic land package to over 6,230 hectares in the Salinas lithium corridor.

Latin Resources’ Managing Director, Chris Gale, commented

“We are very pleased to have secured the Lajinha tenement area, we continue to expand our foothold in this developing regional lithium pegmatite field. Our preliminary reconnaissance mapping and outcrop sampling of this area has confirmed the presence of spodumene pegmatites. Our regional mapping team will now complete a more systematic survey to better understand the extent of the known pegmatite system and select initial drill sites.

“With resource definition drilling underway at our main Bananal Valley area, first pass drilling underway at our Monte Alto area, first pass mapping and sampling completed at our Salinas South area; and now the initial systematic work to commence at the new Lajinha tenement - this provides the Company with a full project lithium development pipeline in the Salinas Region. Now the company has made a significant new lithium discovery, this strategic expansion approach to our exploration is critical for long-term success of developing our first maiden JORC Resource.”

Figure 1: Salinas Lithium Project, new Lajinha tenement location - Minas Gerais District, Brazil

Figure 2: Preliminary reconnaissance mapping – (left), weathered spodumene in outcrop (right) at the new

Lajinha tenement - Minas Gerais District, Brazil

Click here for the full ASX Release

This article includes content from [Company Name], licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.