The Conversation (0)

Reach Resources Limited (ASX: RR1 & RR1O) (“Reach” or “the Company”) is pleased to advise that assay results from the latest field program at Wabli Creek have identified a primary source of high grade Nb/REE mineralisation previously only found in surface eluvial samples on site (Figure 2).

HIGHLIGHTS

Most importantly, these latest high-grade assay results (17.65% Nb2O5 and 13.22% Nb2O5) confirm that the hard rock source material holds the same or similar high-grade concentrations as the weathered surface material (eluvial material), previously reported by the Company (32% Nb2O5 and 2.57% TREO - ASX Announcement 21 December 2023). Further, the in-situ samples have been chipped straight off the bedrock (in-situ) approximately 0.5km from the previously reported sample returning 32% Nb2O5.

Figure 1: Large black rock fragments chipped directly from the in-situ granitic pegmatite outcrop, Wabli Creek, Gascoyne, W.A (Sample – 24WRCK046).

Figure 1: Large black rock fragments chipped directly from the in-situ granitic pegmatite outcrop, Wabli Creek, Gascoyne, W.A (Sample – 24WRCK046).

Located in the highly prospective Gascoyne Province of Western Australia, approximately 150km north of Gascoyne Junction, the Wabli Creek project has previously reported high grade niobium and TREO eluvial results up to 32% Nb2O5 and 2.57% TREO (ASX Announcement 21 December 2023).

These latest in-situ results, in addition to the large ovoid intrusive feature (ASX Announcement 28 May 2024), provide a fundamental change in the prospectivity at Wabli Creek.

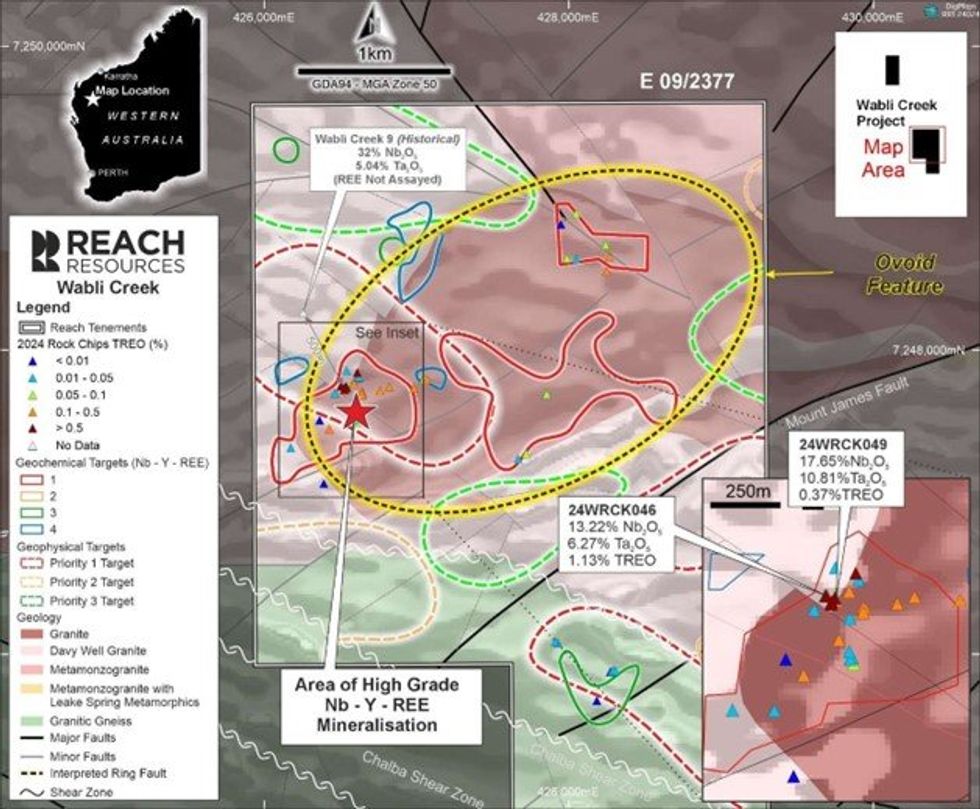

Figure 2: High grade assay results from granitic pegmatite collected at the margins of the late stage, ovoid intrusive feature, Wabli Creek, Gascoyne, W.A (24WRCK046 & 24WRCK049), including historical results approximately 0.5km away reporting 32% Nb2O5 (ASX Announcement 21 December 2023).

Figure 2: High grade assay results from granitic pegmatite collected at the margins of the late stage, ovoid intrusive feature, Wabli Creek, Gascoyne, W.A (24WRCK046 & 24WRCK049), including historical results approximately 0.5km away reporting 32% Nb2O5 (ASX Announcement 21 December 2023).

During the Company’s current program, a total of 49 rock chip samples were taken from Wabli Creek (E09/2377), during May 2024. Sampling was focused on the Priority 1 geochemical targets outlined by Sugden Geoscience (ASX Announcement 21 December 2023).

Click here for the full ASX Release

This article includes content from Reach Resources, licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.