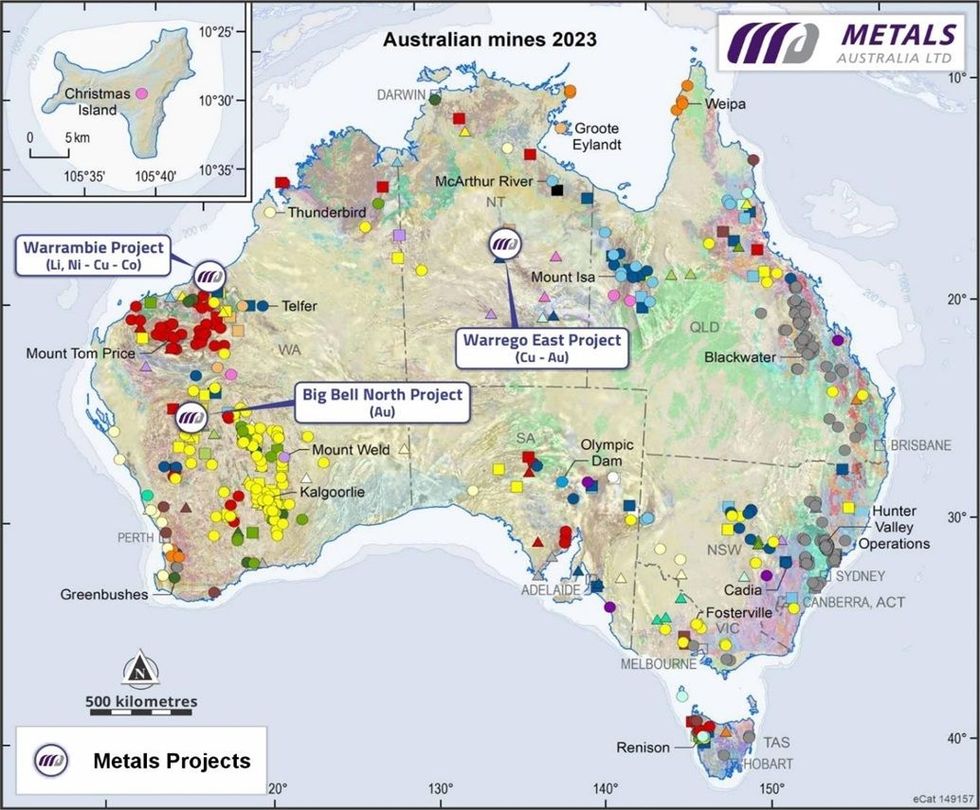

Metals Australia Ltd (ASX: MLS) (“the Company”) is pleased to announce that drilling has commenced testing the first of three key exploration projects in Australia1,8, which are highly prospective for gold and critical minerals. All three projects are located along strike from major mineral deposits in world-class mineral fields (see Figure 1).

- An aircore drilling program of up to 6,000m is underway testing gold, lithium-pegmatite and Ni-Cu- Co targets across the Warrambie Project in WA’s northwest Pilbara1. Warrambie straddles the Scholl Shear Zone, which is analogous to the Mallina Shear – host to the nearby, 10Moz, Hemi gold deposit3. The drilling will also test for major lithium-pegmatites, being located just 10km east of the Andover lithium discovery2,5.

- An up to 120-hole aircore drilling program is permitted to follow an extensive soil sampling and gravity program underway at Big Bell North in WA’s world-class Murchison Gold Province, testing greenstone-splay fault hosted gold targets identified from interpretation of imagery from the recently completed aeromagnetic survey1. Big Bell North is located along strike to the northeast of the 5Moz Big Bell gold deposit4.

- Approvals imminent for a substantial drilling program at the Warrego East copper-gold project within the Tennant Creek Mineral Field, which historically produced a world-class 25Mt @ 6.9g/t Au and 2.8% Cu6. Warrego East is directly east of Warrego mine, which produced 6.75Mt @ 1.9% Cu and 1.8g/t Au6. The drilling will test a series of gravity and magnetics defined ironstone hosted copper-gold targets within a corridor which links the Warrego Mine with the Gecko and Orlando copper-gold deposits6,7.

Metals Australia CEO Paul Ferguson commented:

“2024 is shaping up as the most active and exciting period in Metals Australia’s history - with the three aggressive gold and critical minerals drilling and exploration programs launched at Warrambie, Big Bell North and Warrego East in Australia being advanced in parallel with our two gold and critical minerals programs underway in Canada.

“Critically, our projects are all located in world-class mineralised provinces along strike from major discoveries and historical mines.

We believe all our projects have potential for major new discoveries and we look forward to a period of strong news flow and results throughout the remainder of 2024 and beyond - as we look to unlock their potential and build value for MLS shareholders.”

Figure 1: Metals Australia key Critical Minerals and gold exploration projects in world-class mineral terranes (adapted from Geoscience Australia, Australian Mineral Deposits)

Figure 1: Metals Australia key Critical Minerals and gold exploration projects in world-class mineral terranes (adapted from Geoscience Australia, Australian Mineral Deposits)

Warrambie Lithium-Pegmatite, Gold and Ni-Cu-Co Targets, Northwest Pilbara, WA

An extensive aircore drilling program has commenced testing bedrock lithium-pegmatite targets identified at Warrambie as well as gold and Ni-Cu-Co targets in previously un-explored areas under shallow cover.

Up to 50 aircore holes (up to 6,000m) are being drilled to test targets generated through interpretation of previously acquired detailed aeromagnetics and detailed gravity imagery over the Warrambie project (see Figure 2), including:

- Lithium pegmatite targets associated with northeast-trending fault corridors associated with gravity lows which intersect magnetic mafic intrusive rocks1,8. This is an analogous geological setting to the neighbouring Andover lithium pegmatite discovery (drilling intersections of up to 209m @ 1.42% Li2O2) – which is associated with a 5km wide, northeast-trending structural corridor in mafic intrusive rocks (Figure 2).

- Orogenic gold (and Ni-Cu-Co sulphide) targets associated with magnetic anomalies in the Scholl shear which extend west of the Sabre Resources Ltd (ASX:SBR) Sherlock Bay Project, which hosts a 100,000t Ni-Cu-Co sulphide resource9, where recent drilling produced a significant gold (Ni-Cu-Co) intersection mineralisation (8m @ 1.07 g/t Au, 0.3% Ni, 0.11% Cu in SBDD01010) - see Figure 1. The Scholl Shear is parallel and analogous to the Mallina shear which hosts the world-class, >10Moz, Hemi Gold Deposit (DeGrey Mining, ASX:DEG)3.

Click here for the full ASX Release

This article includes content from Metals Australia Ltd, licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.

Figure 1: Metals Australia key Critical Minerals and gold exploration projects in world-class mineral terranes (adapted from Geoscience Australia, Australian Mineral Deposits)

Figure 1: Metals Australia key Critical Minerals and gold exploration projects in world-class mineral terranes (adapted from Geoscience Australia, Australian Mineral Deposits)