Metals Australia Ltd (“Metals Australia”, or “the Company”) continues to advance its flagship high- grade flake-graphite development project in the Tier 1 mining district of Quebec, Canada.

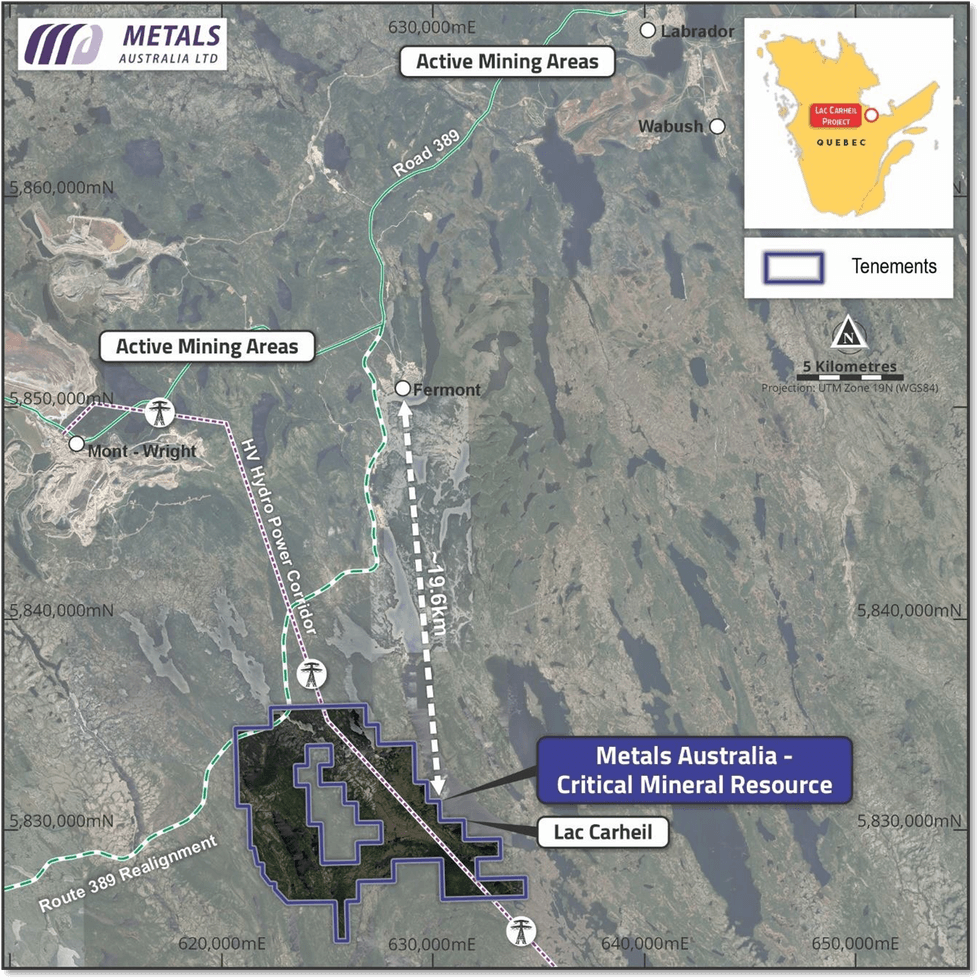

- Project Name change to Lac Carheil Graphite project: Metals Australia is changing the name of its graphite project to Lac Carheil Graphite Project to better align the projects proximity with its closest and most significant geographical feature (Figure 1). The existing project Mineral Resource1 is located on the Carheil Trend, east of Hydro Quebec’s high voltage powerline corridor (315 kV) which bisects the claims owned by the Company. The current resource is a considerable distance from Lac Rainy and much closer to Lac Carheil. The primary objective of the name change is to avoid confusion among all stakeholders (see Figure 2).

- Metals Australia has submitted a new Impact Exploration Assessment (IEA) to the Quebec Ministry of Natural Resources and Forestry (MRNF), following consultation with all stakeholders. The application recognises changes that came into effect from May 6th this year. An application must satisfy the conditions set out in the new regulations and contain questions, requests and comments from local authorities and indigenous communities concerned as well as exploration attributes and delineation of the areas proposed. Metals Australia believes that all Impact concerns raised for a short duration drilling program have been addressed.

- Further contract awards signed. Metals Australia has signed a contract with Lonestar Technical Minerals (LSTM) for the completion of its marketing and pricing strategy as part the overall pre-feasibility (PFS) assessment. This study will investigate the optimum flake-graphite product mix and market opportunities, based on its unique chemical characteristics and flake-size distribution. Graphite is designated as a Critical Mineral in countries such as the USA, Canada, and Australia – given its wide- ranging applications, including as the key anode material in battery energy storage.

- Advancing further detailed proposal reviews for key elements of the project. Significant additional work program scopes are under evaluation, with detailed proposals received and more anticipated. These include Mineral Resource Estimation and Mining Design scopes, which will follow the resource expansion and definition drilling program. Environmental and Social Impact Assessment (ESIA) studies will also be carried out – including baseline environmental studies and ongoing monitoring of the project area. Professional service agreements to support strategic advisory and community engagement programs will also be implemented.

- Progressing previously announced study contracts – Laboratory test work with SGS laboratories is underway, investigating key elements of the design for the Flake Graphite Concentrate Plant, including planned design elements focused on lowering environmental risks associated with long term deposition of tailings. PFS design work with Lycopodium Minerals, Canada is also advancing. Commitments with ANZAPLAN in Germany for downstream design work and location studies are scheduled and will commence when the required sample material has been generated by the SGS test program.

Figure 1: Lac Carheil Graphite Project location, Lac Carheil, Mining Communities, Mining operations, Position of Hydro Quebec 315 KV powerline and proposed new route of main highway (389) to Fermont.

Figure 1: Lac Carheil Graphite Project location, Lac Carheil, Mining Communities, Mining operations, Position of Hydro Quebec 315 KV powerline and proposed new route of main highway (389) to Fermont.

Project Name change to Lac Carheil Graphite project.

Metals Australia has changed the name of the Graphite project to Lac Carheil Graphite Project, as the project’s existing Mineral Resource (13.3 Mt @ 11.5% Graphitic Carbon (Cg) including Indicated of 9.6Mt @ 13.1% Cg & Inferred 3.7Mt @ 7.3% Cg)1 is relatively close to Lac Carheil and a considerable distance from Lac Rainy. Communications have frequently referenced the Carheil trend as the graphite trend on which the current resource exists. The use of Lac Rainy as a project reference has created confusion with stakeholders, given its position to temporarily suspended exploration areas (Figure 2). Figure 2 shows the position of the project resource and lake locations. Also shown are exclusion areas that form part of an Aquatic reserve associated with the Moisie River and its key tributaries, which is approximately 35km south of our current resource. Areas shown in orange have been designated as mining incompatible, while purple areas are under temporary suspension.

Click here for the full ASX Release

This article includes content from Metals Australia Ltd, licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.

Figure 1: Lac Carheil Graphite Project location, Lac Carheil, Mining Communities, Mining operations, Position of Hydro Quebec 315 KV powerline and proposed new route of main highway (389) to Fermont.

Figure 1: Lac Carheil Graphite Project location, Lac Carheil, Mining Communities, Mining operations, Position of Hydro Quebec 315 KV powerline and proposed new route of main highway (389) to Fermont.