The Conversation (0)

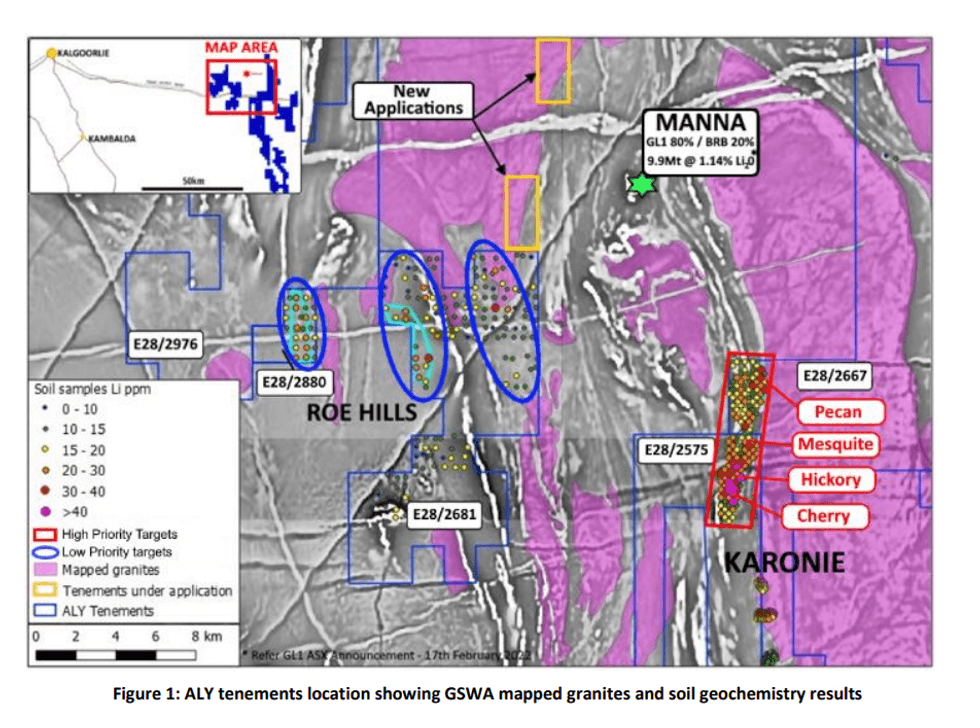

Alchemy Resources Limited (ASX: ALY) (“Alchemy” or “the Company”) is pleased to announce it has identified a new coherent lithium and pathfinder elements anomalous corridor at its 100% owned Karonie Gold Project located east of Kalgoorlie in Western Australia. The tenements sit contiguous and 8km along strike of the Manna Lithium Deposit owned by Global Lithium Resources Limited and Breaker Resources NL (ASX: GL1 80%, ASX:BRB 20%).

Chief Executive Officer Mr James Wilson commented: “The lithium and pathfinder anomalism identified by Alchemy’s soil sampling and recent rock chipping in proximity to Manna are an encouraging start. Mapping by our geologists has shown pegmatites in outcrop along strike of Manna which is made more significant by the fact that there’s been no pegmatites mapped in this region before. The geochemical review reaffirms the prospectivity of our large tenement package at Karonie in what has historically only ever seen gold and base metals exploration. Work is continuing to identify the other intrusive dykes in the vicinity through a program of detailed mapping and sampling.”

NEW LITHIUM PROSPECT IDENTIFICATION – CHERRY, HICKORY, MESQUITE AND PECAN

Alchemy conducted multi-element soil sampling at Pecan/Mesquite/Hickory/Cherry on a 400x400m offset grid (Figure 1, RHS) and formed part of a multi-commodity review. The analysis of lithium and pathfinder elements shows a strong pattern of anomalism over 7km long x 1km wide (Figure 2) with the northern zone having increasing levels of surface cover which could have obscured outcrops. Alchemy’s KZ5 deposit2 located in the southern portion and adjacent to Cherry Prospect is a gold deposit which is believed to be VMS hosted mineralisation with significant drilling being undertaken by Alchemy in 2021. The areas of lithium soil anomalism to the east of the KZ5 gold deposit have never been drill-tested.

The areas sit within the prospective “Goldilocks Zone”, a defined corridor in which LCT pegmatite exist. The zone lies outboard of the granitic terrain and within the greenstone belts.

Alchemy geologists have since conducted initial ground truthing of the anomalies which has revealed outcropping pegmatites at Hickory Prospect and was traced over 1km along strike (Figure 3). A second pegmatite outcrop was mapped at Cherry Prospect (Figure 3). Importantly, GSWA mapping had not mapped the pegmatite outcrops recently identified by Alchemy.

Click here for the full ASX Release

This article includes content from Alchemy Resources Limited, licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.